Long-Term Strategy: 1-Year Breakout + 6-Month Exit

ลิงก์ TradingView

คำอธิบาย

Descripción (Description): (Copia y pega todo lo que está dentro del recuadro de abajo)

Description

This is a long-term trend-following strategy designed to capture major market moves while filtering out short-term noise. It is based on the classic principle of "buying strength" (Breakouts) and allowing profits to run, while cutting losses when the medium-term trend reverses.

How it Works (Logic)

1. Entry Condition (Long Only): The strategy looks for a significant display of strength. It enters a Long position only when two conditions are met simultaneously:

Price Breakout: The closing price exceeds the highest high of the last 252 trading days (approximately 1 year). This ensures we are entering during a strong momentum phase.

Trend Filter: The SuperTrend indicator (Settings: ATR 10, Factor 3.0) must be bullish. This acts as a confirmation filter to avoid false breakouts in choppy markets.

2. Exit Condition: The strategy uses a trailing stop based on price action, not a fixed percentage.

It closes the position when the price closes below the lowest low of the last 126 trading days (approximately 6 months).

This wide exit allows the trade to "breathe" during normal market corrections without exiting the position prematurely.

Settings & Risk Management

Capital Usage: The script is configured to use 10% of equity per trade to reflect realistic risk management (compounding).

Commissions: Included at 0.1% to simulate real trading costs.

Slippage: Included (3 ticks) to account for market execution variability.

Best Use: This strategy is intended for higher timeframes (Daily or Weekly) on trending assets like Indices, Crypto, or Commodities.

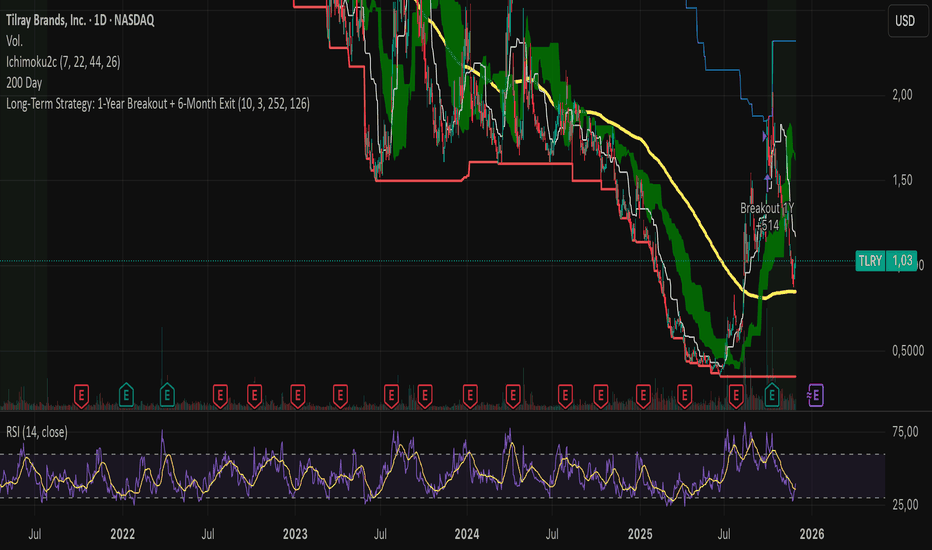

รูป Preview

Pine Script Source

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © TuUsuario

//@version=5

strategy("Long-Term Strategy: 1-Year Breakout + 6-Month Exit",

overlay=true,

initial_capital=10000,

default_qty_type=strategy.percent_of_equity,

default_qty_value=10, // RIESGO: 10% del capital (Norma: Realista)

commission_type=strategy.commission.percent,

commission_value=0.1, // COMISIÓN: 0.1% (Norma: Realista)

slippage=3) // SLIPPAGE: 3 ticks (Norma: Realista)

// --- 1. SETTINGS (Configuration) ---

// SuperTrend Settings (Entry Filter)

atrPeriod = input.int(10, "ATR Period (SuperTrend)", group="Entry Settings")

factor = input.float(3.0, "Factor (SuperTrend)", group="Entry Settings")

// Entry Filter (12 Months / 1 Year)

// 252 trading days approx 1 year

diasEntrada = input.int(252, "Entry High Lookback (Days)", group="Entry Settings")

// Exit Settings (6 Months)

// 126 trading days approx 6 months

diasSalida = input.int(126, "Exit Low Lookback (Days)", group="Exit Settings")

// --- 2. CALCULATIONS ---

[supertrend, direction] = ta.supertrend(factor, atrPeriod)

// 1-Year High (For Entry)

maximoAnual = ta.highest(high, diasEntrada)[1]

// 6-Month Low (For Exit)

minimoSemestral = ta.lowest(low, diasSalida)[1]

// --- 3. TRADING LOGIC ---

// ENTRY CONDITION (LONG):

// 1. SuperTrend is Bullish (direction < 0)

// 2. Price closes above the 1-Year High

longCondition = (direction < 0) and (close >= maximoAnual)

// EXIT CONDITION (CLOSE):

// Price CLOSES below the 6-Month Low.

exitCondition = close < minimoSemestral

// --- 4. EXECUTION ---

if (longCondition)

strategy.entry("Long", strategy.long, comment="Breakout 1Y")

if (exitCondition)

strategy.close("Long", comment="Exit 6M Low")

// --- 5. VISUALIZATION ---

// Entry Level (Blue Line)

plot(maximoAnual, color=color.new(color.blue, 0), title="1-Year High (Entry)")

// Exit Level (Red Line) - Dynamic Stop Loss

plot(minimoSemestral, color=color.new(color.red, 0), linewidth=2, title="6-Month Low (Exit)")

// Background color if position is open

bgcolor(strategy.position_size > 0 ? color.new(color.green, 95) : na)