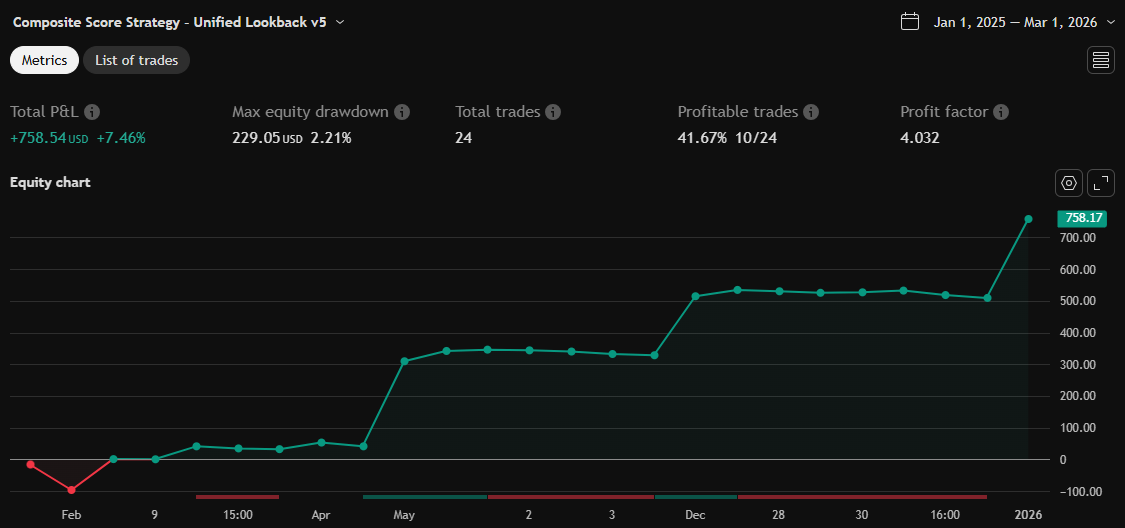

CSS_LFU_v0.1

ลิงก์ TradingView

คำอธิบาย

Overview:

A multi-factor, market-adaptive swing strategy designed for intraday and short-term crypto trading. It synthesizes momentum, volatility, and trend signals into a unified composite score over a configurable lookback window. The strategy leverages a modular, signal-weighted approach to ensure robust entry timing while remaining compatible with human-in-the-loop validation and algorithmic execution.

Core Modules:

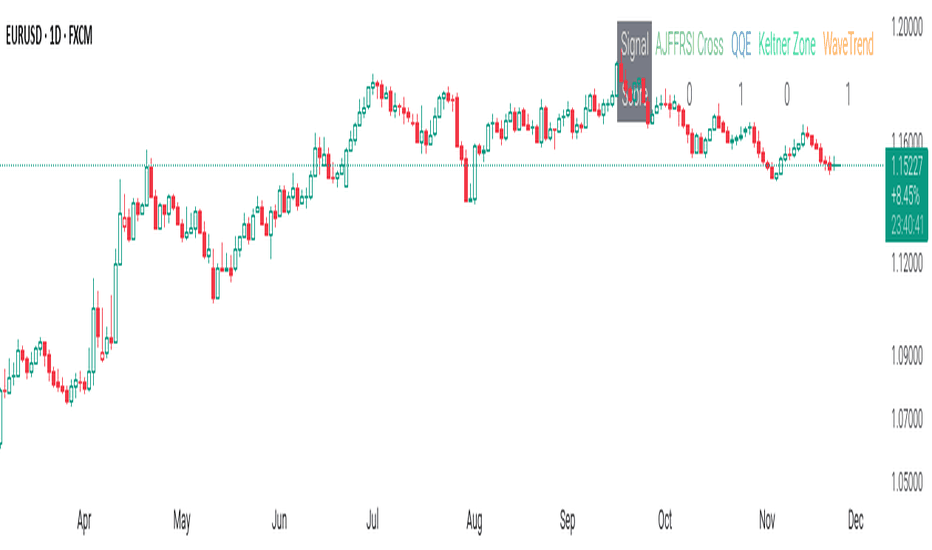

AJFFRSI (RSX-based Momentum): Measures smoothed price momentum with noise-reduction filters to detect crossovers relative to the QQE trailing stop.

QQE (Quantitative Qualitative Easing RSI): A modified RSI with a dynamic trailing stop that adapts to short-term volatility, identifying exhaustion and potential reversal points.

Keltner Channel Zones: Determines overextension relative to trend, providing buy/sell zones based on ATR-banded EMA.

WaveTrend Oscillator: Confirms short-term swings and market direction through smoothed oscillator cross signals.

Rolling Composite Score: Aggregates module signals over a unified lookback (e.g., 144 bars) to normalize noise and capture consistent trends.

Signal Logic:

Each module outputs a discrete score (+1 / 0 / -1).

The rolling composite score sums all module scores over the lookback period.

Long positions trigger when the rolling score meets or exceeds the long threshold.

Short positions trigger when the rolling score meets or falls below the short threshold.

Multi-dimensional signal aggregation reduces false positives from single indicators.

Rolling lookback ensures score normalization across different volatility regimes.

Highly modular: easy to adapt modules or weights to different instruments or timeframes.

Fully compatible with automated execution pipelines, including custom exchange screener bots.

Use Case:

Ideal for quant-driven altcoin or multi-asset strategies where high-frequency validation is critical and sequential module weighting enhances trend flip detection.

รูป Preview

Pine Script Source

//@version=6

strategy("Composite Score Strategy – Unified Lookback v5", overlay=true, max_lines_count=500, max_labels_count=500, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// ============================

// USER CONFIG INPUTS

rsi_len = input.int(14, "AJFFRSI Length")

qqe_src = input.source(close, "QQE Source")

qqe_len = input.int(14, "QQE Length")

qqe_factor = input.float(4.236, "QQE Factor")

qqe_smooth = input.int(5, "QQE Smooth")

keltner_src = input.source(close, "Keltner Source")

score_threshold_long = input.float(1, "Composite Score Long Threshold")

score_threshold_short = input.float(-1, "Composite Score Short Threshold")

lookback_bars = input.int(144, "Unified Lookback (bars)")

colorbars = input.bool(true, "Color bars?")

// ============================

// AJFFRSI MODULE

_rsx_rsi(src,len)=>

src_out = 100 * src

mom0 = ta.change(src_out)

moa0 = math.abs(mom0)

Kg = 3 / (len + 2)

Hg = 1 - Kg

f28 = 0.0

f30 = 0.0

f28 := Kg * mom0 + Hg * nz(f28[1])

f30 := Kg * f28 + Hg * nz(f30[1])

mom1 = f28 * 1.5 - f30 * 0.5

f38 = 0.0

f40 = 0.0

f38 := Hg * nz(f38[1]) + Kg * mom1

f40 := Kg * f38 + Hg * nz(f40[1])

mom2 = f38 * 1.5 - f40 * 0.5

f48 = 0.0

f50 = 0.0

f48 := Hg * nz(f48[1]) + Kg * mom2

f50 := Kg * f48 + Hg * nz(f50[1])

mom_out = f48 * 1.5 - f50 * 0.5

f58 = 0.0

f60 = 0.0

f58 := Hg * nz(f58[1]) + Kg * moa0

f60 := Kg * f58 + Hg * nz(f60[1])

moa1 = f58 * 1.5 - f60 * 0.5

f68 = 0.0

f70 = 0.0

f68 := Hg * nz(f68[1]) + Kg * moa1

f70 := Kg * f68 + Hg * nz(f70[1])

moa2 = f68 * 1.5 - f70 * 0.5

f78 = 0.0

f80 = 0.0

f78 := Hg * nz(f78[1]) + Kg * moa2

f80 := Kg * f78 + Hg * nz(f80[1])

moa_out = f78 * 1.5 - f80 * 0.5

math.max(math.min((mom_out / moa_out + 1.0) * 50.0, 100.0), 0.0)

ajf_rsi = _rsx_rsi(close, rsi_len)

plot(ajf_rsi, color=color.white, linewidth=2, title="AJFFRSI")

// ============================

// QQE MODULE

var float ts = na

delta = qqe_src - qqe_src[1]

num = ta.rma(delta, qqe_len)

den = ta.rma(math.abs(delta), qqe_len)

rsi_qqe = 50 * ta.ema(num / den, qqe_smooth) + 50

diff = ta.rma(math.abs(rsi_qqe - rsi_qqe[1]), qqe_len)

crossover_cond = rsi_qqe > nz(ts) and rsi_qqe[1] <= nz(ts[1])

crossunder_cond = rsi_qqe < nz(ts) and rsi_qqe[1] >= nz(ts[1])

ts := na(ts) ? rsi_qqe : crossover_cond ? rsi_qqe - diff * qqe_factor : crossunder_cond ? rsi_qqe + diff * qqe_factor : ts

plot(rsi_qqe, color=color.blue, title="QQE RSI")

plot(ts, color=rsi_qqe>ts ? color.teal : color.red, title="QQE Trailing Stop")

// ============================

// SIGNALS

bull_cross = ta.crossover(ajf_rsi, ts)

bear_cross = ta.crossunder(ajf_rsi, ts)

// ============================

// KELTNER MODULE

ma = ta.ema(keltner_src, 34)

atr_val = ta.ema(ta.tr(true), 88)

kc_mid = ma

kc_top = kc_mid + atr_val * 1.5

kc_bottom = kc_mid - atr_val * 1.5

kc_buy_zone = close <= kc_bottom

kc_sell_zone = close >= kc_top

kc_cross_up_lower = ta.crossover(close, kc_bottom)

kc_cross_up_upper = ta.crossover(close, kc_top)

// ============================

// WAVETREND MODULE

wt_src = hlc3

wt_movingAverage = ta.ema(wt_src, 10)

wt_movingAverageChannel = ta.ema(math.abs(wt_src - wt_movingAverage), 10)

wt_channelIndex = (wt_src - wt_movingAverage)/(0.015 * wt_movingAverageChannel)

wt_waveTrend1 = ta.ema(wt_channelIndex, 3)

wt_waveTrend2 = ta.sma(wt_waveTrend1, 3)

wt_cross_up = ta.crossover(wt_waveTrend1, wt_waveTrend2)

wt_cross_down = ta.crossunder(wt_waveTrend1, wt_waveTrend2)

// Compute module scores

bull_score = bull_cross ? 1 : 0

bear_score = bear_cross ? -1 : 0

ajf_score = bull_score + bear_score

qqe_score = rsi_qqe > ts ? 1 : rsi_qqe < ts ? -1 : 0

kc_score = kc_buy_zone ? 1 : kc_sell_zone ? -1 : 0

wt_score = wt_cross_up ? 1 : wt_cross_down ? -1 : 0

// Rolling composite score over lookback_bars (used for trade entries)

composite_score_rolling = math.sum(ajf_score + qqe_score + kc_score + wt_score, lookback_bars)

// Cumulative score (for plotting only)

var float composite_score_cum = 0

composite_score_cum := composite_score_cum + ajf_score + qqe_score + kc_score + wt_score

// Entry conditions based on rolling score

if composite_score_rolling >= score_threshold_long

strategy.entry("Long", strategy.long)

if composite_score_rolling <= score_threshold_short

strategy.entry("Short", strategy.short)

// Plot cumulative score for visual reference

plot(composite_score_cum, color=color.orange, title="Composite Score (Cumulative)", linewidth=2)

barcolor(colorbars ? (composite_score_cum > 0 ? color.new(color.green,0) : composite_score_cum < 0 ? color.new(color.red,0) : na) : na)

// ============================

// ALERTS

alertcondition(bull_cross, title="AJFFRSI Bull Cross", message="AJFFRSI crossed above QQE trailing stop – Bullish Signal")

alertcondition(bear_cross, title="AJFFRSI Bear Cross", message="AJFFRSI crossed below QQE trailing stop – Bearish Signal")

alertcondition(kc_buy_zone, title="KC Buy Zone", message="Price touched Keltner support zone")

alertcondition(kc_sell_zone, title="KC Sell Zone", message="Price touched Keltner resistance zone")

alertcondition(wt_cross_up, title="WT Cross Up", message="WaveTrend crossed up")

alertcondition(wt_cross_down, title="WT Cross Down", message="WaveTrend crossed down")

// ============================

// TABLE

var table score_table = table.new(position.top_right, 5, 2, frame_color=color.gray, border_color=color.white)

table.cell(score_table, 0, 0, "Signal", text_color=color.white, bgcolor=color.gray)

table.cell(score_table, 0, 1, "Score", text_color=color.white, bgcolor=color.gray)

table.cell(score_table, 1, 0, "AJFFRSI Cross", text_color=color.green)

table.cell(score_table, 1, 1, str.tostring(ajf_score))

table.cell(score_table, 2, 0, "QQE", text_color=color.blue)

table.cell(score_table, 2, 1, str.tostring(qqe_score))

table.cell(score_table, 3, 0, "Keltner Zone", text_color=color.lime)

table.cell(score_table, 3, 1, str.tostring(kc_score))

table.cell(score_table, 4, 0, "WaveTrend", text_color=color.orange)

table.cell(score_table, 4, 1, str.tostring(wt_score))