NLR-ADX Divergence Strategy Triple-Confirmed

ลิงก์ TradingView

คำอธิบาย

How it works

Builds a cleaner DMI/ADX

Recomputes classic +DI, −DI, ADX over a user-set length.

Then “non-linear regresses” each series toward a mean (your choice: dynamic EMA of the series or a fixed Static Mid like 50).

The further a value is from the mean, the stronger the pull (controlled by alphaMin/alphaMax and the γ exponent), giving smoother, more stable DI/ADX lines with less whipsaw.

Optional EMA smoothing on top of that.

Lock in values at confirmed pivots

Uses price pivots (left/right bars) to confirm swing lows and highs.

When a pivot confirms, the script captures (“freezes”) the current +DI, −DI, and ADX values at that bar and stores them. This avoids later drift from smoothing/EMAs.

Check for triple divergence

For a bullish setup (potential long):

Price makes a Lower Low vs. a prior pivot low,

+DI is higher than before (bulls quietly stronger),

−DI is lower (bears weakening),

ADX is lower (trend fatigue).

For a bearish setup (potential short)

Price makes a Higher High,

+DI is lower, −DI is higher,

ADX is lower.

Adds a “no-intersection” sanity check: between the two pivots, the live series shouldn’t snake across the straight line connecting endpoints. This filters messy, low-quality structures.

Trade logic

On a valid triple-confirm, places a strategy.entry (Long for bullish, Short for bearish) and optionally labels the bar (BUY or SELL with +DI/−DI/ADX arrows).

Simple flip behavior: if you’re long and a new short signal prints (or vice versa), it closes the open side and flips.

Key inputs you can tweak

Custom DMI Settings

DMI Length — base length for DI/ADX.

Non-Linear Regression Model

Mean Reference — EMA(series) (dynamic) or Static mid (e.g., 50).

Dynamic Mean Length & Deviation Scale Length — govern the mean and scale used for regression.

Min/Max Regression & Non-Linearity Exponent (γ) — how strongly values are pulled toward the mean (stronger when far away).

Divergence Engine

Pivot Left/Right Bars — how strict the swing confirmation is (larger = more confirmation, more delay).

Min Bars Between Pivots — avoids comparing “near-duplicate” swings.

Max Historical Pivots to Store — memory cap.

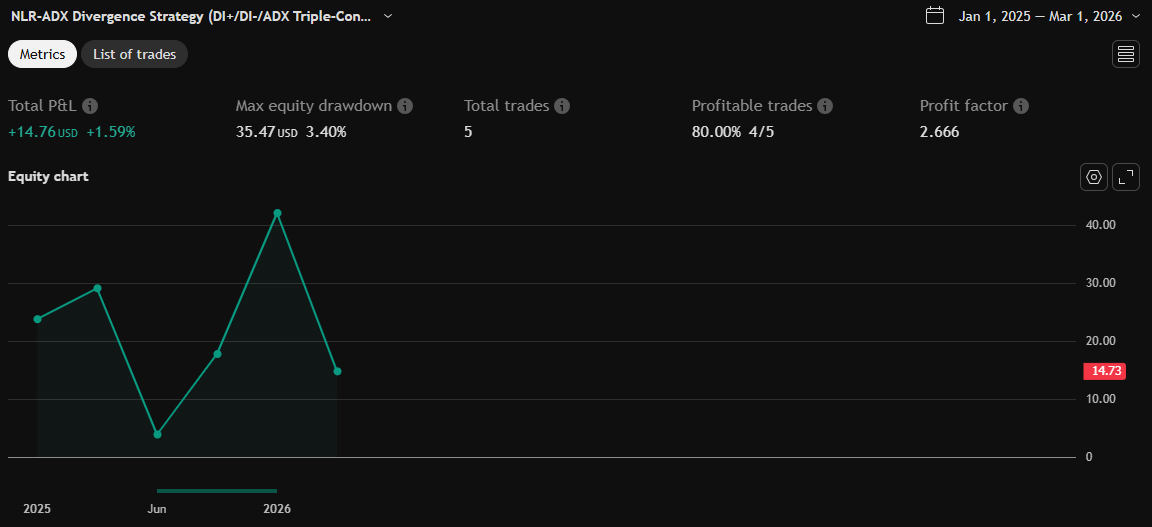

รูป Preview

Pine Script Source

// This Pine Script® code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Cmo22 + assistant update

//@version=5

strategy("NLR-ADX Divergence Strategy (DI+/DI-/ADX Triple-Confirm)", overlay=true, max_lines_count=500, max_labels_count=500, max_bars_back=5000)

//──────────────────────────────────────────────────────────────────────────────

// Inputs: NLR-DMI core (from your indicator)

//──────────────────────────────────────────────────────────────────────────────

grp_dmi = "Custom DMI Settings"

lenDMI = input.int(14, "DMI Length", minval=2, group=grp_dmi)

grp_reg = "Non-Linear Regression Model"

useDynMean = input.string("EMA(series)", "Mean Reference", options=["EMA(series)", "Static mid"], group=grp_reg)

staticMid = input.float(50.0, "Static Mid (DI reference)", step=0.1, group=grp_reg)

lenMean = input.int(50, "Dynamic Mean Length", minval=5, group=grp_reg)

zLen = input.int(100, "Deviation Scale Length", minval=20, group=grp_reg)

alphaMin = input.float(0.00, "Min Regression (near mean)", step=0.01, group=grp_reg)

alphaMax = input.float(0.85, "Max Regression (far from mean)", step=0.01, group=grp_reg)

nlPower = input.float(2.0, "Non-Linearity Exponent (γ)", step=0.1, minval=0.1, group=grp_reg)

grp_out = "Output & Visualization"

smoothOut = input.bool(true, "EMA Smooth Outputs", group=grp_out)

lenOut = input.int(8, "Output EMA Length", group=grp_out)

showSeriesOnChart = input.bool(false, "Plot DI+/DI-/ADX on price chart", group=grp_out)

showDebugLines = input.bool(true, "Draw divergence lines/labels", group=grp_out)

//──────────────────────────────────────────────────────────────────────────────

// Inputs: Divergence engine

//──────────────────────────────────────────────────────────────────────────────

grp_div = "Divergence Engine"

pivotLeftBars = input.int(8, "Pivot Left Bars", minval=1, group=grp_div)

pivotRightBars = input.int(1, "Pivot Right Bars (Confirmation Delay)", minval=1, group=grp_div)

maxPivotsToStore = input.int(30, "Max Historical Pivots to Store", minval=2, group=grp_div)

minBarsBetweenPivots= input.int(5, "Min Bars Between Pivots (P1 & P2)", minval=1, group=grp_div)

//──────────────────────────────────────────────────────────────────────────────

// Utilities

//──────────────────────────────────────────────────────────────────────────────

f_clamp(x, lo, hi) =>

math.max(lo, math.min(hi, x))

f_nl_regress(x, mu, sigma, aMin, aMax, gamma) =>

s = math.max(sigma, 1e-10)

d = math.abs(x - mu) / s

d01 = d / (1.0 + d)

w = math.pow(d01, gamma)

a = f_clamp(aMin + (aMax - aMin) * w, 0.0, 1.0)

mu + (x - mu) * (1.0 - a)

f_apply_reg(x, useDynStr, meanLen, stdevLen, aMin, aMax, gamma, staticMid) =>

mu = useDynStr == "EMA(series)" ? ta.ema(x, meanLen) : staticMid

sd = ta.stdev(x, stdevLen)

f_nl_regress(x, mu, sd, aMin, aMax, gamma)

// "no-intersection" test between two pivot points for a given series

f_series_no_intersect(series float s, int p1_idx, float v1, int p2_idx, float v2) =>

delta = p2_idx - p1_idx

bool ok = true

if delta > 1

float slope = (v2 - v1) / delta

float prev_dev = 0.0

bool has_cross = false

for j = 1 to delta - 1

int hist_offset = bar_index - (p1_idx + j)

float lin = v1 + slope * j

float val_at = s[hist_offset]

float dev = val_at - lin

if j > 1 and math.sign(dev) != math.sign(prev_dev)

has_cross := true

prev_dev := dev

ok := not has_cross

ok

//──────────────────────────────────────────────────────────────────────────────

// Custom DMI Calculation (unchanged logically)

//──────────────────────────────────────────────────────────────────────────────

upMove = ta.change(high)

downMove = -ta.change(low)

plusDM = upMove > downMove and upMove > 0 ? upMove : 0.0

minusDM = downMove > upMove and downMove > 0 ? downMove : 0.0

tr1 = high - low

tr2 = math.abs(high - nz(close[1]))

tr3 = math.abs(low - nz(close[1]))

trueRange = math.max(math.max(tr1, tr2), tr3)

smPlusDM = ta.rma(plusDM, lenDMI)

smMinusDM = ta.rma(minusDM, lenDMI)

smTR = ta.rma(trueRange, lenDMI)

diPlus_raw = smPlusDM / smTR * 100.0

diMinus_raw = smMinusDM / smTR * 100.0

diPlus_reg = f_apply_reg(diPlus_raw, useDynMean, lenMean, zLen, alphaMin, alphaMax, nlPower, staticMid)

diMinus_reg = f_apply_reg(diMinus_raw, useDynMean, lenMean, zLen, alphaMin, alphaMax, nlPower, staticMid)

diPlus = smoothOut ? ta.ema(diPlus_reg, lenOut) : diPlus_reg

diMinus = smoothOut ? ta.ema(diMinus_reg, lenOut) : diMinus_reg

dx = math.abs(diPlus - diMinus) / math.max(diPlus + diMinus, 1e-10) * 100.0

adx_raw = ta.rma(dx, lenDMI)

adx = smoothOut ? ta.ema(adx_raw, lenOut) : adx_raw

// Optional plots on price pane (off by default)

plot(showSeriesOnChart ? diPlus : na, title="+DI (Regressed)", color=color.new(color.teal, 0), linewidth=2)

plot(showSeriesOnChart ? diMinus : na, title="-DI (Regressed)", color=color.new(color.red, 0), linewidth=2)

plot(showSeriesOnChart ? adx : na, title="ADX (Regressed)", color=color.new(color.yellow,0), linewidth=3)

//──────────────────────────────────────────────────────────────────────────────

// Divergence storage (store *frozen* values at each pivot to avoid EMA drift)

//──────────────────────────────────────────────────────────────────────────────

var int[] pivotLow_bars = array.new_int()

var float[] pivotLow_price = array.new_float()

var float[] pivotLow_diP = array.new_float()

var float[] pivotLow_diM = array.new_float()

var float[] pivotLow_adx = array.new_float()

var int[] pivotHigh_bars = array.new_int()

var float[] pivotHigh_price = array.new_float()

var float[] pivotHigh_diP = array.new_float()

var float[] pivotHigh_diM = array.new_float()

var float[] pivotHigh_adx = array.new_float()

// Detect confirmed price pivots

pl_price_confirmed = ta.pivotlow(low, pivotLeftBars, pivotRightBars)

ph_price_confirmed = ta.pivothigh(high, pivotLeftBars, pivotRightBars)

//──────────────────────────────────────────────────────────────────────────────

// BUY side: price LL + (+DI HL) + (-DI lower) + (ADX lower)

//──────────────────────────────────────────────────────────────────────────────

var bool newBuySignal = false

var bool newSellSignal = false

newBuySignal := false

newSellSignal := false

if not na(pl_price_confirmed)

int P2_bar_idx = bar_index - pivotRightBars

float P2_price = low[pivotRightBars]

// *** CAPTURE FROZEN INDICATOR VALUES AT THE PIVOT BAR ***

float diP2_cap = diPlus[pivotRightBars]

float diM2_cap = diMinus[pivotRightBars]

float adx2_cap = adx[pivotRightBars]

// Compare vs all stored prior low pivots (using stored P1 values)

if array.size(pivotLow_bars) > 0

for i = 0 to array.size(pivotLow_bars) - 1

int P1_bar_idx = array.get(pivotLow_bars, i)

float P1_price = array.get(pivotLow_price, i)

float diP1_cap = array.get(pivotLow_diP, i)

float diM1_cap = array.get(pivotLow_diM, i)

float adx1_cap = array.get(pivotLow_adx, i)

if P2_bar_idx <= P1_bar_idx

continue

if (P2_bar_idx - P1_bar_idx) < minBarsBetweenPivots

continue

// Price must make a Lower Low

bool priceLL = P2_price < P1_price

// Triple divergence at the same pair of price lows (using *captured* values)

bool plus_bull = diP2_cap > diP1_cap // +DI higher on new LL

bool minus_bear_equiv = diM2_cap < diM1_cap // -DI lower (bears weakening)

bool adx_bear = adx2_cap < adx1_cap // ADX lower (weaker trend)

// No-intersection checks using stored endpoints and live series in-between

bool price_no_x = f_series_no_intersect(low, P1_bar_idx, P1_price, P2_bar_idx, P2_price)

bool diplus_no_x = f_series_no_intersect(diPlus, P1_bar_idx, diP1_cap, P2_bar_idx, diP2_cap)

bool diminus_no_x = f_series_no_intersect(diMinus,P1_bar_idx, diM1_cap, P2_bar_idx, diM2_cap)

bool adx_no_x = f_series_no_intersect(adx, P1_bar_idx, adx1_cap, P2_bar_idx, adx2_cap)

if priceLL and plus_bull and minus_bear_equiv and adx_bear and price_no_x and diplus_no_x and diminus_no_x and adx_no_x

if showDebugLines

label.new(P2_bar_idx, P2_price, "BUY\n+DI↑ -DI↓ ADX↓", yloc=yloc.belowbar,

style=label.style_label_up, color=color.new(color.green,70), textcolor=color.white, size=size.tiny)

strategy.entry("Long", strategy.long, comment="DI/ADX Triple Bull Div")

newBuySignal := true

break

// Save THIS pivot-L with captured indicator values (freeze at detection time)

array.unshift(pivotLow_bars, P2_bar_idx)

array.unshift(pivotLow_price, P2_price)

array.unshift(pivotLow_diP, diP2_cap)

array.unshift(pivotLow_diM, diM2_cap)

array.unshift(pivotLow_adx, adx2_cap)

// Trim

while array.size(pivotLow_bars) > maxPivotsToStore

array.pop(pivotLow_bars)

array.pop(pivotLow_price)

array.pop(pivotLow_diP)

array.pop(pivotLow_diM)

array.pop(pivotLow_adx)

//──────────────────────────────────────────────────────────────────────────────

// SELL side: price HH + (+DI LH) + (-DI higher) + (ADX lower)

//──────────────────────────────────────────────────────────────────────────────

if not na(ph_price_confirmed)

int P2_bar_idx = bar_index - pivotRightBars

float P2_price = high[pivotRightBars]

// *** CAPTURE FROZEN INDICATOR VALUES AT THE PIVOT BAR ***

float diP2_cap = diPlus[pivotRightBars]

float diM2_cap = diMinus[pivotRightBars]

float adx2_cap = adx[pivotRightBars]

if array.size(pivotHigh_bars) > 0

for i = 0 to array.size(pivotHigh_bars) - 1

int P1_bar_idx = array.get(pivotHigh_bars, i)

float P1_price = array.get(pivotHigh_price, i)

float diP1_cap = array.get(pivotHigh_diP, i)

float diM1_cap = array.get(pivotHigh_diM, i)

float adx1_cap = array.get(pivotHigh_adx, i)

if P2_bar_idx <= P1_bar_idx

continue

if (P2_bar_idx - P1_bar_idx) < minBarsBetweenPivots

continue

// Price must make a Higher High

bool priceHH = P2_price > P1_price

// Triple divergence at the same pair of price highs (using *captured* values)

bool plus_bear = diP2_cap < diP1_cap // +DI lower on new HH

bool minus_bull = diM2_cap > diM1_cap // -DI higher (bears strengthening)

bool adx_bear = adx2_cap < adx1_cap // ADX lower (weaker trend)

// No-intersection checks using stored endpoints and live series in-between

bool price_no_x = f_series_no_intersect(high, P1_bar_idx, P1_price, P2_bar_idx, P2_price)

bool diplus_no_x = f_series_no_intersect(diPlus, P1_bar_idx, diP1_cap, P2_bar_idx, diP2_cap)

bool diminus_no_x = f_series_no_intersect(diMinus,P1_bar_idx, diM1_cap, P2_bar_idx, diM2_cap)

bool adx_no_x = f_series_no_intersect(adx, P1_bar_idx, adx1_cap, P2_bar_idx, adx2_cap)

if priceHH and plus_bear and minus_bull and adx_bear and price_no_x and diplus_no_x and diminus_no_x and adx_no_x

if showDebugLines

label.new(P2_bar_idx, P2_price, "SELL\n+DI↓ -DI↑ ADX↓", yloc=yloc.abovebar,

style=label.style_label_down, color=color.new(color.red,70), textcolor=color.white, size=size.tiny)

strategy.entry("Short", strategy.short, comment="DI/ADX Triple Bear Div")

newSellSignal := true

break

// Save THIS pivot-H with captured indicator values (freeze at detection time)

array.unshift(pivotHigh_bars, P2_bar_idx)

array.unshift(pivotHigh_price, P2_price)

array.unshift(pivotHigh_diP, diP2_cap)

array.unshift(pivotHigh_diM, diM2_cap)

array.unshift(pivotHigh_adx, adx2_cap)

// Trim

while array.size(pivotHigh_bars) > maxPivotsToStore

array.pop(pivotHigh_bars)

array.pop(pivotHigh_price)

array.pop(pivotHigh_diP)

array.pop(pivotHigh_diM)

array.pop(pivotHigh_adx)

// Optional: simple flip on opposite signal (exit current side on new entry the other way)

if strategy.position_size > 0 and newSellSignal

strategy.close("Long", comment="FlipToShort")

if strategy.position_size < 0 and newBuySignal

strategy.close("Short", comment="FlipToLong")