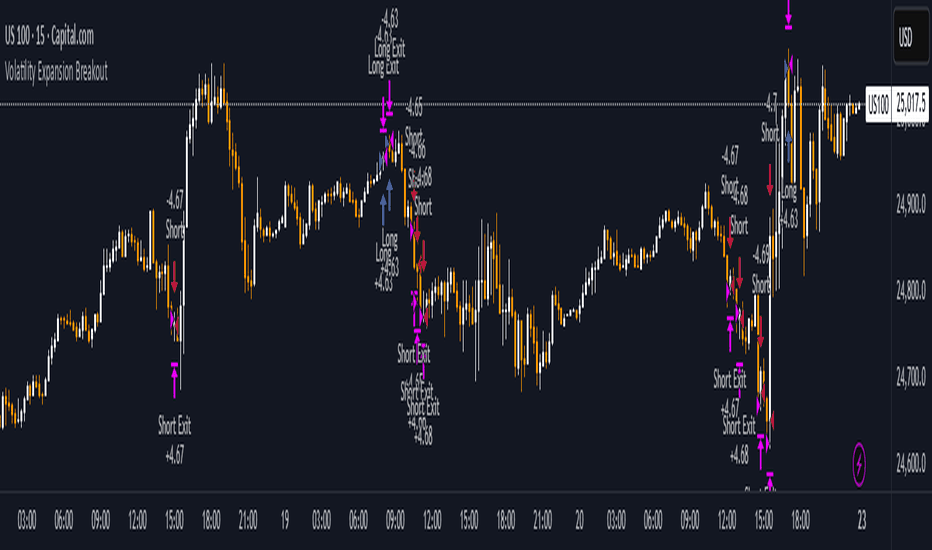

Volatility Expansion Breakout

ลิงก์ TradingView

คำอธิบาย

Short term volatility breakout strategy that works well on indices

รูป Preview

Pine Script Source

//@version=5

strategy("Volatility Expansion Breakout",

overlay=true,

initial_capital=100000,

default_qty_type=strategy.percent_of_equity,

default_qty_value=1)

// === Inputs ===

htf = input.timeframe("60", "Higher Timeframe")

emaLen = input.int(200, "HTF EMA Length")

atrLen = input.int(14, "ATR Length")

atrMult = input.float(2.0, "ATR Trail Multiplier")

rangeLen = input.int(20, "Breakout Range Length")

// === Higher Timeframe Bias ===

htfClose = request.security(syminfo.tickerid, htf, close)

htfEMA = request.security(syminfo.tickerid, htf, ta.ema(close, emaLen))

bullBias = htfClose > htfEMA

bearBias = htfClose < htfEMA

// === Volatility ===

atr = ta.atr(atrLen)

atrRising = atr > atr[1]

// === Breakout Levels ===

rangeHigh = ta.highest(high, rangeLen)

rangeLow = ta.lowest(low, rangeLen)

// === Entries ===

longCondition = bullBias and atrRising and close > rangeHigh[1]

shortCondition = bearBias and atrRising and close < rangeLow[1]

if longCondition

strategy.entry("Long", strategy.long)

if shortCondition

strategy.entry("Short", strategy.short)

// === Trailing Stop ===

longTrail = close - atr * atrMult

shortTrail = close + atr * atrMult

strategy.exit("Long Exit", from_entry="Long", trail_price=longTrail, trail_offset=atr*atrMult)

strategy.exit("Short Exit", from_entry="Short", trail_price=shortTrail, trail_offset=atr*atrMult)