Supertrend 3H Strategy Vinay

ลิงก์ TradingView

คำอธิบาย

Supertrend 3H Strategy Vinay-

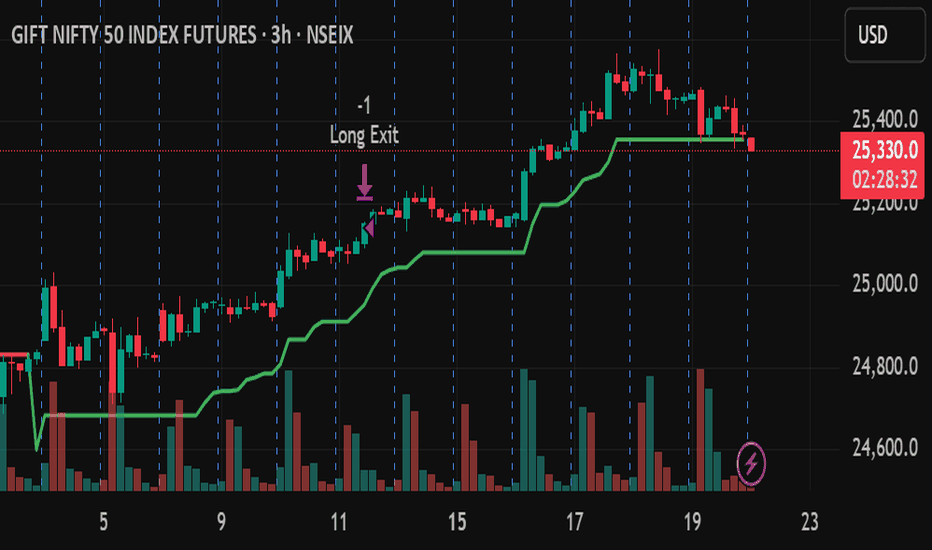

Buy or sell using Supertrend, 200 points SL and 400 points target

รูป Preview

Pine Script Source

//@version=5

strategy("Supertrend 3H Strategy", overlay=true, margin_long=100, margin_short=100, process_orders_on_close=true)

//---------------------------

// Supertrend Inputs

//---------------------------

Periods = input.int(10, title="ATR Period")

Multiplier = input.float(3.0, title="ATR Multiplier", step=0.1)

//---------------------------

// Request 3H Data

//---------------------------

src = request.security(syminfo.tickerid, "180", hl2)

close3 = request.security(syminfo.tickerid, "180", close)

atr3 = request.security(syminfo.tickerid, "180", ta.atr(Periods))

//---------------------------

// Supertrend Calculation (3H)

//---------------------------

up = src - Multiplier * atr3

dn = src + Multiplier * atr3

var float upTrend = na

var float downTrend = na

var int trend = na

up1 = nz(upTrend[1], up)

dn1 = nz(downTrend[1], dn)

upTrend := close3[1] > up1 ? math.max(up, up1) : up

downTrend := close3[1] < dn1 ? math.min(dn, dn1) : dn

trend := na(trend[1]) ? 1 : trend[1]

trend := trend == -1 and close3 > dn1 ? 1 : trend == 1 and close3 < up1 ? -1 : trend

buySignal = trend == 1 and trend[1] == -1

sellSignal = trend == -1 and trend[1] == 1

supertrendLine = trend == 1 ? upTrend : downTrend

plot(supertrendLine, "3H Supertrend", color = trend == 1 ? color.green : color.red, linewidth=2)

//---------------------------

// Strategy Logic

//---------------------------

// Long Entry: Only after buySignal, wait for *next bullish candle* close > supertrend

bullishCondition = buySignal[1] and close > supertrendLine and close > open

// Short Entry: Only after sellSignal, wait for *next bearish candle* close < supertrend

bearishCondition = sellSignal[1] and close < supertrendLine and close < open

//---------------------------

// Orders with Fixed TP/SL

//---------------------------

tpPoints = 400.0

slPoints = 200.0

if (bullishCondition)

strategy.entry("Long", strategy.long)

strategy.exit("Long Exit", "Long", stop = strategy.position_avg_price - slPoints, limit = strategy.position_avg_price + tpPoints)

if (bearishCondition)

strategy.entry("Short", strategy.short)

strategy.exit("Short Exit", "Short", stop = strategy.position_avg_price + slPoints, limit = strategy.position_avg_price - tpPoints)