MAVSS ShLong

ลิงก์ TradingView

คำอธิบาย

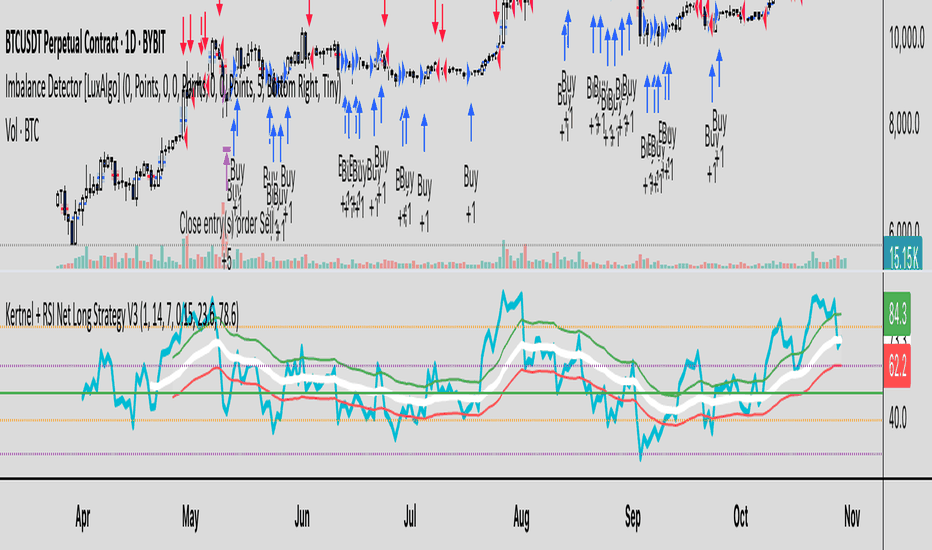

Long bottom of the keltner channel, and short the top with RSI confirmation.

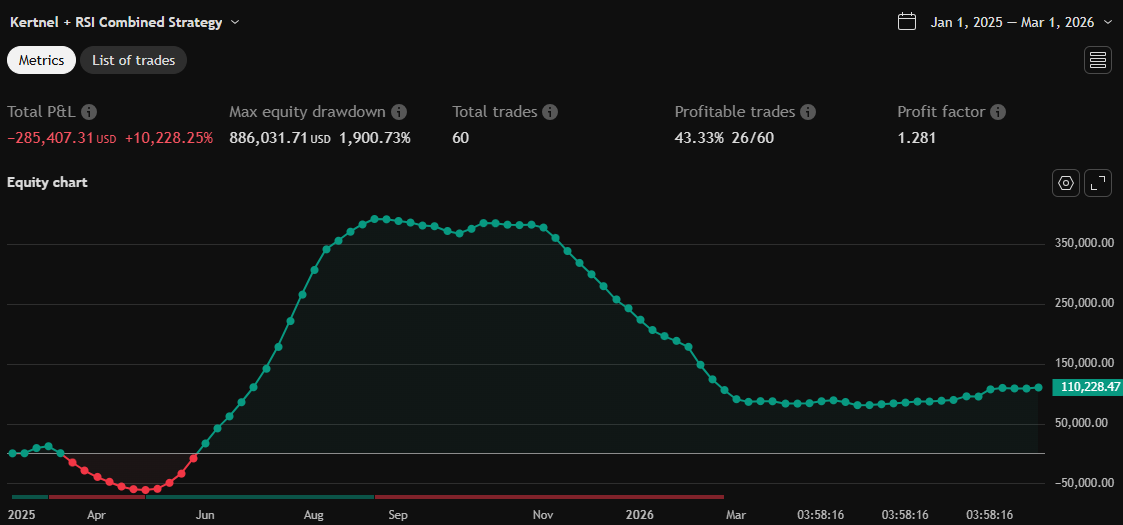

รูป Preview

Pine Script Source

//@version=5

strategy(title="Kertnel + RSI Combined Strategy", overlay=false, pyramiding=10)

// Strategy Inputs

lotSize = input.int(1, title="Lot Size per Order")

lengthMiddle = input.int(14, title="MiddleEMA")

// Adjustment 1: Narrower Channel

channelATR = input.int(7, title="Channel wall ATR")

channelWidth = input.float(0.15, title = "Channel Width")

showBarColor = input.bool(true, title="Highlight Bear/Bull reversals?")

rsiOversoldLevel = input.float(23.6, title="RSI Oversold Level")

rsiOverboughtLevel = input.float(78.6, title="RSI Overbought Level")

// rsi manual

change = ta.change(close)

gain = change >= 0 ? change : 0.0

loss = change < 0 ? (-1) * change : 0.0

avgGain = ta.rma(gain, lengthMiddle)

avgLoss = ta.rma(loss, lengthMiddle)

rs = avgGain / avgLoss

rsi_14 = 100 - (100 / (1 + rs))

// keltner channel calculation

rsi_seven = ta.rsi(close,7)

rsi_keltner = ta.ema(rsi_14,lengthMiddle)

rsi_keltner_previous = ta.rsi(close[1],lengthMiddle)

current_period = ta.rsi(close,lengthMiddle)

abs_current_period_high = math.abs(rsi_keltner - rsi_keltner_previous)

true_range = math.max(current_period, abs_current_period_high)

absolute_true_range = ta.rma(true_range, channelATR)

upperVal = rsi_keltner + channelWidth * absolute_true_range

lowerVal = rsi_keltner - channelWidth * absolute_true_range

// Strategy Logic

// --- BUY/LONG LOGIC ---

// Long at the bottom of the channel on reversal AND in oversold territory

// Adjustment 2 & 3: Reversal from lower channel and RSI filter

longCondition = rsi_seven[1] < lowerVal and rsi_seven > rsi_seven[1] and rsi_seven < rsiOversoldLevel

if longCondition

strategy.order("Buy", strategy.long, qty=lotSize)

// --- SELL/SHORT LOGIC ---

// Short at the top of the channel on reversal AND in overbought territory

// Adjustment 2 & 3: Reversal from upper channel and RSI filter

shortCondition = rsi_seven[1] > upperVal and rsi_seven < rsi_seven[1] and rsi_seven > rsiOverboughtLevel

if shortCondition

strategy.order("Sell", strategy.short, qty=lotSize)

// Close shorts at the bottom of the channel

if ta.crossunder(rsi_seven, lowerVal) and strategy.position_size < 0

strategy.close("Sell", qty=math.abs(strategy.position_size))

// Plotting (optional)

rsi_line = plot(rsi_seven, style=plot.style_line, linewidth=3, color = color.aqua)

middle_line = plot(rsi_keltner, style=plot.style_line, linewidth=3, color=color.white)

upper_line = plot(upperVal, color=color.green)

lower_line = plot(lowerVal, color = color.red)

fill(upper_line, lower_line, color=color.white, transp=90)

band1 = hline(rsiOverboughtLevel, color=color.orange,linestyle=hline.style_dotted)

band0 = hline(rsiOversoldLevel, color=color.purple,linestyle=hline.style_dotted)

hline(61.8, color=color.purple,linestyle=hline.style_dotted)

hline(38.2, color=color.orange,linestyle=hline.style_dotted)

hline(50, color=color.green,linestyle=hline.style_solid)