FlowStateTrader

ลิงก์ TradingView

คำอธิบาย

FlowState Trader - Advanced Time-Filtered Strategy

## Overview

FlowState Trader is a sophisticated algorithmic trading strategy that combines precision entry signals with intelligent time-based filtering and adaptive risk management. Built for traders seeking to achieve their optimal performance state, FlowState identifies high-probability trading opportunities within user-defined time windows while employing dynamic trailing stops and partial position management.

## Core Strategy Philosophy

FlowState Trader operates on the principle that peak trading performance occurs when three elements align: **Focus** (precise entry signals), **Flow** (optimal time windows), and **State** (intelligent position management). This strategy excels at finding reversal opportunities at key support and resistance levels while filtering out suboptimal trading periods to keep traders in their optimal flow state.

## Key Features

### 🎯 Focus Entry System

**Support/Resistance Zone Trading**:

- Dynamic identification of key price levels using configurable lookback periods

- Entry signals triggered when price interacts with these critical zones

- Volume confirmation ensures genuine breakout/reversal momentum

- Trend filter alignment prevents counter-trend disasters

**Entry Conditions**:

- **Long Signals**: Price closes above support buffer, touches support level, with above-average volume

- **Short Signals**: Price closes below resistance buffer, touches resistance level, with above-average volume

- Optional trend filter using EMA or SMA for directional bias confirmation

### ⏰ FlowState Time Filtering System

**Comprehensive Time Controls**:

- **12-Hour Format Trading Windows**: User-friendly AM/PM time selection

- **Multi-Timezone Support**: UTC, EST, PST, CST with automatic conversion

- **Day-of-Week Filtering**: Trade only weekdays, weekends, or both

- **Lunch Hour Avoidance**: Automatically skips low-volume lunch periods (12-1 PM)

- **Visual Time Indicators**: Background coloring shows active/inactive trading periods

**Smart Time Features**:

- Handles overnight trading sessions seamlessly

- Prevents trades during historically poor performance periods

- Customizable trading hours for different market sessions

- Real-time trading window status in dashboard

### 🛡️ Adaptive Risk Management

**Multi-Level Take Profit System**:

- **TP1**: First profit target with optional partial position closure

- **TP2**: Final profit target for remaining position

- **Flexible Scaling**: Choose number of contracts to close at each level

**Dynamic Trailing Stop Technology**:

- **Three Operating Modes**:

- **Conservative**: Earlier activation, tighter trailing (protect profits)

- **Balanced**: Optimal risk/reward balance (recommended)

- **Aggressive**: Later activation, wider trailing (let winners run)

- **ATR-Based Calculations**: Adapts to current market volatility

- **Automatic Activation**: Engages when position reaches profitability threshold

### 📊 Intelligent Position Sizing

**Contract-Based Management**:

- Configurable entry quantity (1-1000 contracts)

- Partial close quantities for profit-taking

- Clear position tracking and P&L monitoring

- Real-time position status updates

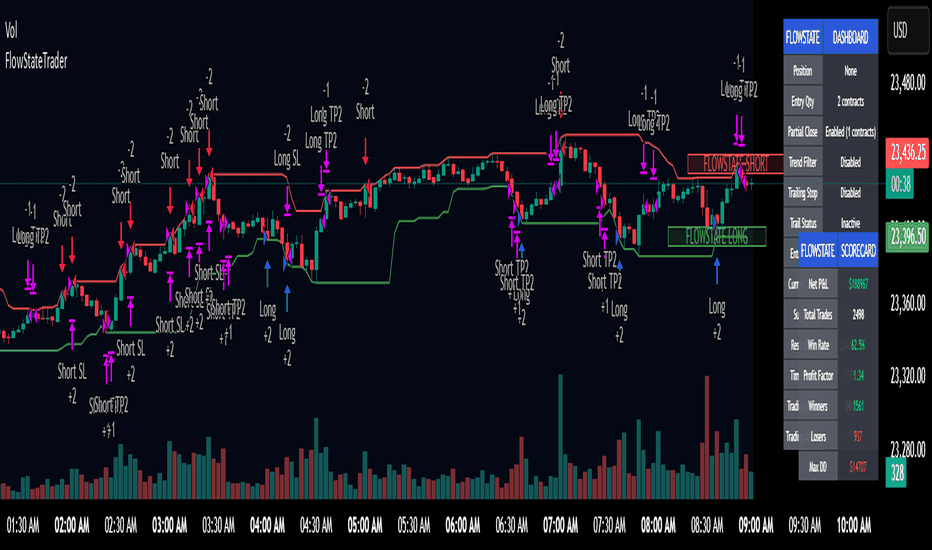

### 🎨 Professional Visualization

**Enhanced Chart Elements**:

- **Entry Zone Highlighting**: Clear visual identification of trading opportunities

- **Dynamic Risk/Reward Lines**: Real-time TP and SL levels with price labels

- **Trailing Stop Visualization**: Live tracking of adaptive stop levels

- **Support/Resistance Lines**: Key level identification

- **Time Window Background**: Visual confirmation of active trading periods

**Dual Dashboard System**:

- **Strategy Dashboard**: Real-time position info, settings status, and current levels

- **Performance Scorecard**: Live P&L tracking, win rates, and trade statistics

- **Customizable Sizing**: Small, Medium, or Large display options

### ⚙️ Comprehensive Customization

**Core Strategy Settings**:

- **Lookback Period**: Support/resistance calculation period (5-100 bars)

- **ATR Configuration**: Period and multipliers for stops/targets

- **Reward-to-Risk Ratios**: Customizable profit target calculations

- **Trend Filter Options**: EMA/SMA selection with adjustable periods

**Time Filter Controls**:

- **Trading Hours**: Start/end times in 12-hour format

- **Timezone Selection**: Four major timezone options

- **Day Restrictions**: Weekend-only, weekday-only, or unrestricted

- **Session Management**: Lunch hour avoidance and custom periods

**Risk Management Options**:

- **Trailing Stop Modes**: Conservative/Balanced/Aggressive presets

- **Partial Close Settings**: Enable/disable with custom quantities

- **Alert System**: Comprehensive notifications for all trade events

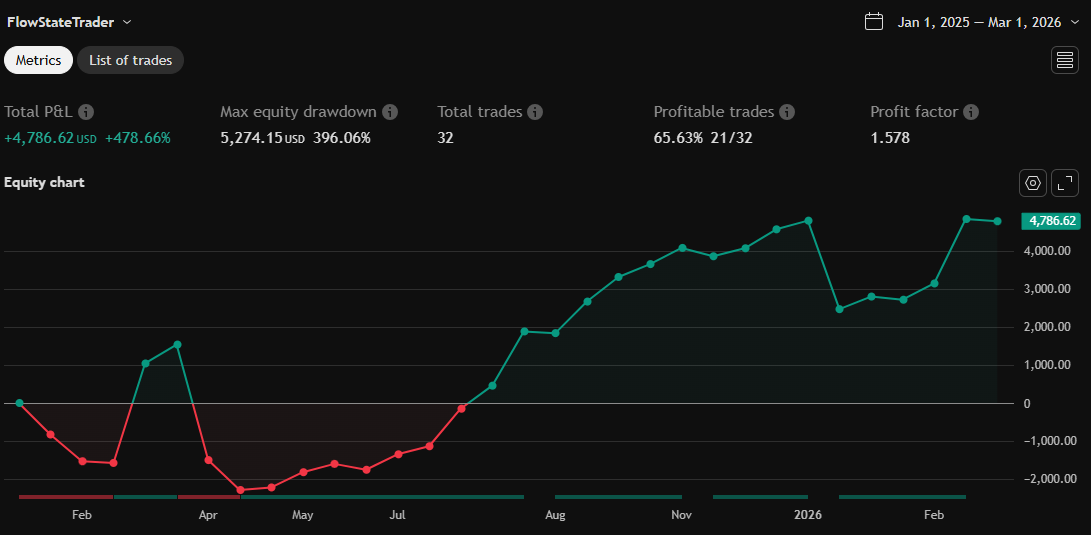

### 📈 Performance Tracking

**Real-Time Metrics**:

- Net profit/loss calculation

- Win rate percentage

- Profit factor analysis

- Maximum drawdown tracking

- Total trade count and breakdown

- Current position P&L

**Trade Analytics**:

- Winner/loser ratio tracking

- Real-time performance scorecard

- Strategy effectiveness monitoring

- Risk-adjusted return metrics

### 🔔 Alert System

**Comprehensive Notifications**:

- Entry signal alerts with price and quantity

- Take profit level hits (TP1 and TP2)

- Stop loss activations

- Trailing stop engagements

- Position closure notifications

## Strategy Logic Deep Dive

### Entry Signal Generation

The strategy identifies high-probability reversal points by combining multiple confirmation factors:

1. **Price Action**: Looks for price interaction with key support/resistance levels

2. **Volume Confirmation**: Ensures sufficient market interest and liquidity

3. **Trend Alignment**: Optional filter prevents counter-trend positions

4. **Time Validation**: Only trades during user-defined optimal periods

5. **Zone Analysis**: Entry occurs within calculated buffer zones around key levels

### Risk Management Philosophy

FlowState Trader employs a three-tier risk management approach:

1. **Initial Protection**: ATR-based stop losses set at strategy entry

2. **Profit Preservation**: Trailing stops activate once position becomes profitable

3. **Scaled Exit**: Partial profit-taking allows for both security and potential

### Time-Based Edge

The time filtering system recognizes that not all trading hours are equal:

- Avoids low-volume, high-spread periods

- Focuses on optimal liquidity windows

- Prevents trading during news events (lunch hours)

- Allows customization for different market sessions

## Best Practices and Optimization

### Recommended Settings

**For Scalping (1-5 minute charts)**:

- Lookback Period: 10-20

- ATR Period: 14

- Trailing Stop: Conservative mode

- Time Filter: Major session hours only

**For Day Trading (15-60 minute charts)**:

- Lookback Period: 20-30

- ATR Period: 14-21

- Trailing Stop: Balanced mode

- Time Filter: Extended trading hours

**For Swing Trading (4H+ charts)**:

- Lookback Period: 30-50

- ATR Period: 21+

- Trailing Stop: Aggressive mode

- Time Filter: Disabled or very broad

### Market Compatibility

- **Forex**: Excellent for major pairs during active sessions

- **Stocks**: Ideal for liquid stocks during market hours

- **Futures**: Perfect for index and commodity futures

- **Crypto**: Effective on major cryptocurrencies (24/7 capability)

### Risk Considerations

- **Market Conditions**: Performance varies with volatility regimes

- **Timeframe Selection**: Lower timeframes require tighter risk management

- **Position Sizing**: Never risk more than 1-2% of account per trade

- **Backtesting**: Always test on historical data before live implementation

## Educational Value

FlowState serves as an excellent learning tool for:

- Understanding support/resistance trading

- Learning proper time-based filtering

- Mastering trailing stop techniques

- Developing systematic trading approaches

- Risk management best practices

## Disclaimer

This strategy is for educational and informational purposes only. Past performance does not guarantee future results. Trading involves substantial risk of loss and is not suitable for all investors. Users should thoroughly backtest the strategy and understand all risks before live trading. Always use proper position sizing and never risk more than you can afford to lose.

---

*FlowState Trader represents the evolution of systematic trading - combining classical technical analysis with modern risk management and intelligent time filtering to help traders achieve their optimal performance state through systematic, disciplined execution.*

รูป Preview

Pine Script Source

//@version=5

strategy("FlowStateTrader", overlay=true)

// Input Parameters

lookbackPeriod = input.int(20, "Lookback Period for Key Levels", minval=5, maxval=100)

atrPeriod = input.int(14, "ATR Period", minval=5, maxval=50)

atrMultiplierSL = input.float(1.5, "SL ATR Multiplier", minval=0.5, maxval=5.0, step=0.1)

atrMultiplierTP1 = input.float(1.5, "TP1 ATR Multiplier", minval=0.5, maxval=5.0, step=0.1)

atrMultiplierTP2 = input.float(2.0, "TP2 ATR Multiplier", minval=0.5, maxval=5.0, step=0.1)

rewardToRisk = input.float(2.0, "Reward to Risk Ratio", minval=1.0, maxval=5.0, step=0.1)

// Trend Filter Settings

enableTrendFilter = input.bool(true, "Enable Trend Filter")

trendMAPeriod = input.int(20, "Trend MA Period", minval=5, maxval=200)

trendMAType = input.string("EMA", "Trend MA Type", options=["EMA", "SMA"])

// TIME FILTER SETTINGS

enableTimeFilter = input.bool(false, "Enable Time-Based Filter", tooltip="Filter trades based on specific time windows")

// 12-hour format time inputs

startHour12 = input.int(9, "Start Hour (1-12)", minval=1, maxval=12, tooltip="Trading start hour in 12-hour format")

startAMPM = input.string("AM", "Start AM/PM", options=["AM", "PM"])

endHour12 = input.int(4, "End Hour (1-12)", minval=1, maxval=12, tooltip="Trading end hour in 12-hour format")

endAMPM = input.string("PM", "End AM/PM", options=["AM", "PM"])

// Timezone selection

timeZone = input.string("UTC", "Time Zone", options=["UTC", "EST", "PST", "CST"], tooltip="Time zone for trading hours")

// Additional controls

avoidLunchHour = input.bool(true, "Avoid Lunch Hour (12:00-1:00 PM)", tooltip="Skip trading during typical lunch break")

weekendsOnly = input.bool(false, "Weekends Only", tooltip="Only trade on weekends")

weekdaysOnly = input.bool(false, "Weekdays Only", tooltip="Only trade on weekdays")

// Strategy Settings

entryQty = input.int(1, "Entry Quantity (Contracts)", minval=1, maxval=1000)

enablePartialClose = input.bool(true, "Enable Partial Close at TP1")

partialCloseQty = input.int(1, "Contracts to Close at TP1", minval=1, maxval=100)

enableAlerts = input.bool(true, "Enable Strategy Alerts")

// Dashboard Settings

dashboardSize = input.string("Medium", "Dashboard Size", options=["Small", "Medium", "Large"], tooltip="Control the size of the information dashboard")

enableScorecard = input.bool(true, "Enable Performance Scorecard", tooltip="Show performance metrics in lower right corner")

// Trailing Stop Settings

enableTrailingStop = input.bool(true, "Enable Trailing Stop")

trailMode = input.string("Balanced", "Trailing Stop Mode", options=["Conservative", "Balanced", "Aggressive"], tooltip="Conservative: Protect more profit | Balanced: Good middle ground | Aggressive: Let winners run longer")

// Set trailing parameters based on mode

trailActivationMultiplier = trailMode == "Conservative" ? 0.8 : trailMode == "Balanced" ? 1.0 : 1.2

trailDistanceMultiplier = trailMode == "Conservative" ? 0.6 : trailMode == "Balanced" ? 0.8 : 1.0

// TIME FILTER FUNCTIONS

// Convert 12-hour format to 24-hour format

convertTo24Hour(hour12, ampm) =>

var int hour24 = na

if ampm == "AM"

hour24 := hour12 == 12 ? 0 : hour12

else // PM

hour24 := hour12 == 12 ? 12 : hour12 + 12

hour24

// Convert timezone to UTC offset

getUTCOffset(tz) =>

var int offset = na

if tz == "UTC"

offset := 0

else if tz == "EST"

offset := -5 // EST is UTC-5

else if tz == "CST"

offset := -6 // CST is UTC-6

else if tz == "PST"

offset := -8 // PST is UTC-8

offset

getCurrentHour() =>

hour(time, "UTC")

getCurrentDayOfWeek() =>

dayofweek(time)

isWeekend() =>

currentDay = getCurrentDayOfWeek()

currentDay == dayofweek.saturday or currentDay == dayofweek.sunday

isWeekday() =>

not isWeekend()

isInTradingWindow() =>

if not enableTimeFilter

true

else

// Convert 12-hour inputs to 24-hour UTC

startHour24 = convertTo24Hour(startHour12, startAMPM)

endHour24 = convertTo24Hour(endHour12, endAMPM)

utcOffset = getUTCOffset(timeZone)

// Convert local time to UTC

startHourUTC = (startHour24 - utcOffset + 24) % 24

endHourUTC = (endHour24 - utcOffset + 24) % 24

currentHour = getCurrentHour()

// Handle trading window logic

var bool inWindow = false

// Handle same-day window vs overnight window

if startHourUTC <= endHourUTC

// Same day window (e.g., 9 AM to 4 PM)

inWindow := currentHour >= startHourUTC and currentHour <= endHourUTC

else

// Overnight window (e.g., 10 PM to 6 AM)

inWindow := currentHour >= startHourUTC or currentHour <= endHourUTC

// Apply day-of-week filters

if weekendsOnly and not isWeekend()

inWindow := false

if weekdaysOnly and not isWeekday()

inWindow := false

// Apply lunch hour filter (12:00-1:00 PM in selected timezone)

if avoidLunchHour and inWindow

lunchStart24 = 12 // 12 PM

lunchEnd24 = 13 // 1 PM

lunchStartUTC = (lunchStart24 - utcOffset + 24) % 24

lunchEndUTC = (lunchEnd24 - utcOffset + 24) % 24

// Check if current hour falls in lunch period

if lunchStartUTC <= lunchEndUTC

// Normal case: lunch doesn't cross midnight

if currentHour >= lunchStartUTC and currentHour < lunchEndUTC

inWindow := false

else

// Edge case: lunch period crosses midnight (shouldn't happen but safety check)

if currentHour >= lunchStartUTC or currentHour < lunchEndUTC

inWindow := false

inWindow

// Combined time filter

isGoodTradingTime() =>

isInTradingWindow()

// ATR and Volume Calculation

atr = ta.atr(atrPeriod)

volumeSMA = ta.sma(volume, atrPeriod)

// Trend Filter

trendMA = enableTrendFilter ? (trendMAType == "EMA" ? ta.ema(close, trendMAPeriod) : ta.sma(close, trendMAPeriod)) : na

isBullishTrend = enableTrendFilter ? close > trendMA : true

isBearishTrend = enableTrendFilter ? close < trendMA : true

// Key Levels Identification (Support & Resistance Zones)

support = ta.lowest(low, lookbackPeriod)

resistance = ta.highest(high, lookbackPeriod)

supportBuffer = support - atr * 0.5

resistanceBuffer = resistance + atr * 0.5

// Define Entry Conditions (with time filter)

isBullishEntry = (close > supportBuffer) and (low <= support) and (volume > volumeSMA) and isBullishTrend and isGoodTradingTime()

isBearishEntry = (close < resistanceBuffer) and (high >= resistance) and (volume > volumeSMA) and isBearishTrend and isGoodTradingTime()

// Calculate Stop Loss and Take Profit Levels

bullishSL = support - atr * atrMultiplierSL

bullishTP1 = support + atr * rewardToRisk * atrMultiplierTP1

bullishTP2 = support + atr * rewardToRisk * atrMultiplierTP2

bearishSL = resistance + atr * atrMultiplierSL

bearishTP1 = resistance - atr * rewardToRisk * atrMultiplierTP1

bearishTP2 = resistance - atr * rewardToRisk * atrMultiplierTP2

// Strategy Position Management

var float longEntryPrice = na

var float shortEntryPrice = na

var bool tp1HitLong = false

var bool tp1HitShort = false

// Trailing Stop Variables

var float longTrailStop = na

var float shortTrailStop = na

var bool longTrailActive = false

var bool shortTrailActive = false

// Calculate position sizing

finalQty = entryQty

// Long Entry

if isBullishEntry and strategy.position_size == 0

strategy.entry("Long", strategy.long, qty=finalQty)

longEntryPrice := close

tp1HitLong := false

// Reset trailing stop variables

longTrailStop := na

longTrailActive := false

if enableAlerts

alert("Long Entry Signal at " + str.tostring(close) + " - Qty: " + str.tostring(finalQty), alert.freq_once_per_bar)

// Short Entry

if isBearishEntry and strategy.position_size == 0

strategy.entry("Short", strategy.short, qty=finalQty)

shortEntryPrice := close

tp1HitShort := false

// Reset trailing stop variables

shortTrailStop := na

shortTrailActive := false

if enableAlerts

alert("Short Entry Signal at " + str.tostring(close) + " - Qty: " + str.tostring(finalQty), alert.freq_once_per_bar)

// Long Position Management

if strategy.position_size > 0

// Calculate current profit

currentProfit = close - strategy.position_avg_price

profitInATR = currentProfit / atr

// Trailing Stop Logic

if enableTrailingStop and profitInATR >= trailActivationMultiplier

// Activate trailing stop

if not longTrailActive

longTrailActive := true

longTrailStop := close - atr * trailDistanceMultiplier

else

// Update trailing stop (only move up, never down)

newTrailStop = close - atr * trailDistanceMultiplier

longTrailStop := math.max(longTrailStop, newTrailStop)

// Determine which stop loss to use

effectiveStopLoss = enableTrailingStop and longTrailActive ? longTrailStop : bullishSL

// Stop Loss (either original or trailing)

strategy.exit("Long SL", "Long", stop=effectiveStopLoss)

// Take Profit 1 (Partial Close by Contracts)

if enablePartialClose and not tp1HitLong and high >= bullishTP1 and strategy.position_size >= partialCloseQty

strategy.close("Long", qty=partialCloseQty, comment="Long TP1", immediately=true)

tp1HitLong := true

// Take Profit 2 (Close Remaining Position) or Full Close if Partial is Disabled

if (enablePartialClose and tp1HitLong and high >= bullishTP2) or (not enablePartialClose and high >= bullishTP1)

strategy.close("Long", comment=enablePartialClose ? "Long TP2" : "Long TP1", immediately=true)

// Short Position Management

if strategy.position_size < 0

// Calculate current profit (for shorts, profit when price goes down)

currentProfit = strategy.position_avg_price - close

profitInATR = currentProfit / atr

// Trailing Stop Logic

if enableTrailingStop and profitInATR >= trailActivationMultiplier

// Activate trailing stop

if not shortTrailActive

shortTrailActive := true

shortTrailStop := close + atr * trailDistanceMultiplier

else

// Update trailing stop (only move down, never up)

newTrailStop = close + atr * trailDistanceMultiplier

shortTrailStop := math.min(shortTrailStop, newTrailStop)

// Determine which stop loss to use

effectiveStopLoss = enableTrailingStop and shortTrailActive ? shortTrailStop : bearishSL

// Stop Loss (either original or trailing)

strategy.exit("Short SL", "Short", stop=effectiveStopLoss)

// Take Profit 1 (Partial Close by Contracts)

if enablePartialClose and not tp1HitShort and low <= bearishTP1 and math.abs(strategy.position_size) >= partialCloseQty

strategy.close("Short", qty=partialCloseQty, comment="Short TP1", immediately=true)

tp1HitShort := true

// Take Profit 2 (Close Remaining Position) or Full Close if Partial is Disabled

if (enablePartialClose and tp1HitShort and low <= bearishTP2) or (not enablePartialClose and low <= bearishTP1)

strategy.close("Short", comment=enablePartialClose ? "Short TP2" : "Short TP1", immediately=true)

// Reset flags when position closes

if strategy.position_size == 0

tp1HitLong := false

tp1HitShort := false

// Reset trailing stop variables

longTrailStop := na

shortTrailStop := na

longTrailActive := false

shortTrailActive := false

// Visualization - Entry Zones

var box bullishBox = na

var box bearishBox = na

var label bullishZoneLabel = na

var label bearishZoneLabel = na

// Bullish Entry Zone

if isBullishEntry

if na(bullishBox)

bullishBox := box.new(left=bar_index - 10, top=support + atr * 0.5, right=bar_index + 10, bottom=support - atr * 0.5, border_color=color.green, bgcolor=color.new(color.green, 85))

bullishZoneLabel := label.new(bar_index, support, "FLOWSTATE LONG", color=color.new(color.white, 100), textcolor=color.green, style=label.style_label_center, size=size.normal)

else

box.set_left(bullishBox, bar_index - 10)

box.set_right(bullishBox, bar_index + 10)

box.set_top(bullishBox, support + atr * 0.5)

box.set_bottom(bullishBox, support - atr * 0.5)

label.set_xy(bullishZoneLabel, bar_index, support)

// Bearish Entry Zone

if isBearishEntry

if na(bearishBox)

bearishBox := box.new(left=bar_index - 10, top=resistance + atr * 0.5, right=bar_index + 10, bottom=resistance - atr * 0.5, border_color=color.red, bgcolor=color.new(color.red, 85))

bearishZoneLabel := label.new(bar_index, resistance, "FLOWSTATE SHORT", color=color.new(color.white, 100), textcolor=color.red, style=label.style_label_center, size=size.normal)

else

box.set_left(bearishBox, bar_index - 10)

box.set_right(bearishBox, bar_index + 10)

box.set_top(bearishBox, resistance + atr * 0.5)

box.set_bottom(bearishBox, resistance - atr * 0.5)

label.set_xy(bearishZoneLabel, bar_index, resistance)

// Visualization - Risk/Reward Lines for Active Positions

var line longTP1Line = na

var line longTP2Line = na

var line longSLLine = na

var line shortTP1Line = na

var line shortTP2Line = na

var line shortSLLine = na

// Labels for TP/SL Values

var label longTP1Label = na

var label longTP2Label = na

var label longSLLabel = na

var label shortTP1Label = na

var label shortTP2Label = na

var label shortSLLabel = na

// Long Position Lines and Labels

if strategy.position_size > 0

if na(longTP1Line)

longTP1Line := line.new(bar_index, bullishTP1, bar_index + 10, bullishTP1, color=color.green, width=2)

longTP2Line := line.new(bar_index, bullishTP2, bar_index + 10, bullishTP2, color=color.green, width=2)

longSLLine := line.new(bar_index, bullishSL, bar_index + 10, bullishSL, color=color.red, width=2)

// Create labels with values

longTP1Label := label.new(bar_index + 10, bullishTP1, "TP1: " + str.tostring(bullishTP1, "#.####"), color=color.green, textcolor=color.white, style=label.style_label_left, size=size.small)

longTP2Label := label.new(bar_index + 10, bullishTP2, "TP2: " + str.tostring(bullishTP2, "#.####"), color=color.green, textcolor=color.white, style=label.style_label_left, size=size.small)

longSLLabel := label.new(bar_index + 10, bullishSL, "SL: " + str.tostring(bullishSL, "#.####"), color=color.red, textcolor=color.white, style=label.style_label_left, size=size.small)

else

line.set_xy1(longTP1Line, bar_index, bullishTP1)

line.set_xy2(longTP1Line, bar_index + 10, bullishTP1)

line.set_xy1(longTP2Line, bar_index, bullishTP2)

line.set_xy2(longTP2Line, bar_index + 10, bullishTP2)

line.set_xy1(longSLLine, bar_index, bullishSL)

line.set_xy2(longSLLine, bar_index + 10, bullishSL)

// Update labels

label.set_xy(longTP1Label, bar_index + 10, bullishTP1)

label.set_text(longTP1Label, "TP1: " + str.tostring(bullishTP1, "#.####"))

label.set_xy(longTP2Label, bar_index + 10, bullishTP2)

label.set_text(longTP2Label, "TP2: " + str.tostring(bullishTP2, "#.####"))

label.set_xy(longSLLabel, bar_index + 10, bullishSL)

label.set_text(longSLLabel, "SL: " + str.tostring(bullishSL, "#.####"))

else

if not na(longTP1Line)

line.delete(longTP1Line)

line.delete(longTP2Line)

line.delete(longSLLine)

label.delete(longTP1Label)

label.delete(longTP2Label)

label.delete(longSLLabel)

longTP1Line := na

longTP2Line := na

longSLLine := na

longTP1Label := na

longTP2Label := na

longSLLabel := na

// Short Position Lines and Labels

if strategy.position_size < 0

if na(shortTP1Line)

shortTP1Line := line.new(bar_index, bearishTP1, bar_index + 10, bearishTP1, color=color.red, width=2)

shortTP2Line := line.new(bar_index, bearishTP2, bar_index + 10, bearishTP2, color=color.red, width=2)

shortSLLine := line.new(bar_index, bearishSL, bar_index + 10, bearishSL, color=color.green, width=2)

// Create labels with values

shortTP1Label := label.new(bar_index + 10, bearishTP1, "TP1: " + str.tostring(bearishTP1, "#.####"), color=color.red, textcolor=color.white, style=label.style_label_left, size=size.small)

shortTP2Label := label.new(bar_index + 10, bearishTP2, "TP2: " + str.tostring(bearishTP2, "#.####"), color=color.red, textcolor=color.white, style=label.style_label_left, size=size.small)

shortSLLabel := label.new(bar_index + 10, bearishSL, "SL: " + str.tostring(bearishSL, "#.####"), color=color.green, textcolor=color.white, style=label.style_label_left, size=size.small)

else

line.set_xy1(shortTP1Line, bar_index, bearishTP1)

line.set_xy2(shortTP1Line, bar_index + 10, bearishTP1)

line.set_xy1(shortTP2Line, bar_index, bearishTP2)

line.set_xy2(shortTP2Line, bar_index + 10, bearishTP2)

line.set_xy1(shortSLLine, bar_index, bearishSL)

line.set_xy2(shortSLLine, bar_index + 10, bearishSL)

// Update labels

label.set_xy(shortTP1Label, bar_index + 10, bearishTP1)

label.set_text(shortTP1Label, "TP1: " + str.tostring(bearishTP1, "#.####"))

label.set_xy(shortTP2Label, bar_index + 10, bearishTP2)

label.set_text(shortTP2Label, "TP2: " + str.tostring(bearishTP2, "#.####"))

label.set_xy(shortSLLabel, bar_index + 10, bearishSL)

label.set_text(shortSLLabel, "SL: " + str.tostring(bearishSL, "#.####"))

else

if not na(shortTP1Line)

line.delete(shortTP1Line)

line.delete(shortTP2Line)

line.delete(shortSLLine)

label.delete(shortTP1Label)

label.delete(shortTP2Label)

label.delete(shortSLLabel)

shortTP1Line := na

shortTP2Line := na

shortSLLine := na

shortTP1Label := na

shortTP2Label := na

shortSLLabel := na

// Support and Resistance Lines

plot(support, "Support", color=color.green, linewidth=1, style=plot.style_line)

plot(resistance, "Resistance", color=color.red, linewidth=1, style=plot.style_line)

// Plot Trend MA if enabled

plot(enableTrendFilter ? trendMA : na, "Trend MA", color=color.blue, linewidth=2)

// Plot Trailing Stops if active

plot(strategy.position_size > 0 and longTrailActive ? longTrailStop : na, "Long Trail Stop", color=color.orange, linewidth=2, style=plot.style_stepline)

plot(strategy.position_size < 0 and shortTrailActive ? shortTrailStop : na, "Short Trail Stop", color=color.orange, linewidth=2, style=plot.style_stepline)

// ENHANCED DASHBOARD WITH TIME INFO

// Background color for trading windows

tradingWindowBg = enableTimeFilter and isInTradingWindow() ? color.new(color.blue, 95) : na

offHoursBg = enableTimeFilter and not isInTradingWindow() ? color.new(color.red, 98) : na

bgcolor(tradingWindowBg, title="Active Trading Window")

bgcolor(offHoursBg, title="Off Trading Hours")

// Table for Current Strategy Info

dashboardTextSize = dashboardSize == "Small" ? size.tiny : dashboardSize == "Medium" ? size.small : size.normal

var table infoTable = table.new(position.top_right, 2, 14, bgcolor=color.new(color.black, 10), border_width=1)

if barstate.islast

// Header row

table.cell(infoTable, 0, 0, "FLOWSTATE", text_color=color.white, bgcolor=color.new(color.blue, 20), text_size=size.small)

table.cell(infoTable, 1, 0, "DASHBOARD", text_color=color.white, bgcolor=color.new(color.blue, 20), text_size=size.small)

table.cell(infoTable, 0, 1, "Position", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(infoTable, 1, 1, strategy.position_size > 0 ? "Long (" + str.tostring(math.abs(strategy.position_size)) + ")" : strategy.position_size < 0 ? "Short (" + str.tostring(math.abs(strategy.position_size)) + ")" : "None", text_color=color.white, text_size=size.tiny)

table.cell(infoTable, 0, 2, "Entry Qty", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(infoTable, 1, 2, str.tostring(entryQty) + " contracts", text_color=color.white, text_size=size.tiny)

table.cell(infoTable, 0, 3, "Partial Close", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(infoTable, 1, 3, enablePartialClose ? "Enabled (" + str.tostring(partialCloseQty) + " contracts)" : "Disabled", text_color=color.white, text_size=size.tiny)

table.cell(infoTable, 0, 4, "Trend Filter", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(infoTable, 1, 4, enableTrendFilter ? trendMAType + "(" + str.tostring(trendMAPeriod) + ")" : "Disabled", text_color=color.white, text_size=size.tiny)

table.cell(infoTable, 0, 5, "Trailing Stop", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(infoTable, 1, 5, enableTrailingStop ? trailMode + " Mode" : "Disabled", text_color=color.white, text_size=size.tiny)

table.cell(infoTable, 0, 6, "Trail Status", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(infoTable, 1, 6, strategy.position_size > 0 and longTrailActive ? "Long Trailing" : strategy.position_size < 0 and shortTrailActive ? "Short Trailing" : "Inactive", text_color=color.white, text_size=size.tiny)

table.cell(infoTable, 0, 7, "Entry Price", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(infoTable, 1, 7, strategy.position_size != 0 ? str.tostring(strategy.position_avg_price, "#.####") : "N/A", text_color=color.white, text_size=size.tiny)

table.cell(infoTable, 0, 8, "Current P&L", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(infoTable, 1, 8, strategy.position_size != 0 ? str.tostring(strategy.openprofit, "#.##") : "N/A", text_color=strategy.openprofit >= 0 ? color.lime : color.red, text_size=size.tiny)

table.cell(infoTable, 0, 9, "Support", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(infoTable, 1, 9, str.tostring(support, "#.####"), text_color=color.lime, text_size=size.tiny)

table.cell(infoTable, 0, 10, "Resistance", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(infoTable, 1, 10, str.tostring(resistance, "#.####"), text_color=color.red, text_size=size.tiny)

// TIME-BASED DASHBOARD ROWS

table.cell(infoTable, 0, 11, "Time Filter", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(infoTable, 1, 11, enableTimeFilter ? "ON" : "OFF", text_color=enableTimeFilter ? color.lime : color.red, text_size=size.tiny)

table.cell(infoTable, 0, 12, "Trading Hours", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(infoTable, 1, 12, enableTimeFilter ? str.tostring(startHour12) + startAMPM + "-" + str.tostring(endHour12) + endAMPM + " " + timeZone : "24/7", text_color=color.white, text_size=size.tiny)

table.cell(infoTable, 0, 13, "Trading Active", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(infoTable, 0, 13, "Trading Active", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(infoTable, 1, 13, isGoodTradingTime() ? "YES" : "NO", text_color=isGoodTradingTime() ? color.lime : color.red, text_size=size.tiny)

// Performance Scorecard Table

if enableScorecard

var table scorecardTable = table.new(position.bottom_right, 2, 8, bgcolor=color.new(color.black, 10), border_width=1)

if barstate.islast

// Calculate performance metrics

totalTrades = strategy.closedtrades

winningTrades = strategy.wintrades

losingTrades = strategy.losstrades

winRate = totalTrades > 0 ? (winningTrades / totalTrades) * 100 : 0

profitFactor = strategy.grossprofit / math.abs(strategy.grossloss)

netProfit = strategy.netprofit

maxDrawdown = strategy.max_drawdown

// Header

table.cell(scorecardTable, 0, 0, "FLOWSTATE", text_color=color.white, bgcolor=color.new(color.blue, 20), text_size=size.small)

table.cell(scorecardTable, 1, 0, "SCORECARD", text_color=color.white, bgcolor=color.new(color.blue, 20), text_size=size.small)

// Performance metrics

table.cell(scorecardTable, 0, 1, "Net P&L", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(scorecardTable, 1, 1, "$" + str.tostring(netProfit, "#"), text_color=netProfit >= 0 ? color.lime : color.red, text_size=size.tiny)

table.cell(scorecardTable, 0, 2, "Total Trades", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(scorecardTable, 1, 2, str.tostring(totalTrades), text_color=color.white, text_size=size.tiny)

table.cell(scorecardTable, 0, 3, "Win Rate", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(scorecardTable, 1, 3, str.tostring(winRate, "#.#") + "%", text_color=winRate >= 50 ? color.lime : color.red, text_size=size.tiny)

table.cell(scorecardTable, 0, 4, "Profit Factor", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(scorecardTable, 1, 4, str.tostring(profitFactor, "#.##"), text_color=profitFactor >= 1.0 ? color.lime : color.red, text_size=size.tiny)

table.cell(scorecardTable, 0, 5, "Winners", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(scorecardTable, 1, 5, str.tostring(winningTrades), text_color=color.lime, text_size=size.tiny)

table.cell(scorecardTable, 0, 6, "Losers", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(scorecardTable, 1, 6, str.tostring(losingTrades), text_color=color.red, text_size=size.tiny)

table.cell(scorecardTable, 0, 7, "Max DD", text_color=color.white, bgcolor=color.new(color.gray, 50), text_size=size.tiny)

table.cell(scorecardTable, 1, 7, "$" + str.tostring(math.abs(maxDrawdown), "#"), text_color=color.orange, text_size=size.tiny)