MES 15m High Win Rate Mean Reversion

ลิงก์ TradingView

คำอธิบาย

Core Idea

It assumes:

Most 15-minute moves in normal conditions revert back toward fair value.

Fair value = VWAP + 20-period mean

It is not a trend strategy.

It bets against short-term overextension.

Market Environment It Wants

This system performs best when:

Market is rotational

Volatility is moderate

No major macro catalyst

Institutions are rebalancing inventory

It avoids:

Strong breakout days

Expansion after news

Persistent trend sessions

Step-By-Step Logic

1️⃣ Volatility Compression Filter

It checks:

ATR (14)

Compared to its 30-bar average

If ATR is too high → no trade.

This attempts to skip news days and expansion regimes.

2️⃣ Extreme Detection

On the 15-minute chart:

It calculates:

20-period mean

2 standard deviation Bollinger Bands

VWAP

A trade triggers only when:

For Long:

Price touches lower 2σ band

Price is below VWAP

For Short:

Price touches upper 2σ band

Price is above VWAP

This defines “statistical stretch.”

3️⃣ Position Structure

6 MES contracts

5 point stop (~$150 risk)

6–6.5 point target (~$180–$195 reward)

Max 2 trades per day

One trade per direction

Why It Has Higher Win Rate

Because:

It trades exhaustion, not continuation.

It enters after price is statistically stretched.

Target is smaller than stop multiple systems.

It avoids high volatility regimes.

Mean reversion strategies win often because markets rotate more than they trend.

What It Is Not

It is not:

A breakout system

A momentum system

A trend following model

A high daily payout generator

It is a:

Low-frequency, moderate-edge, capital-preservation framework.

Risk Characteristics

From your backtest:

Win rate ≈ 60%

Profit factor ≈ 1.7

Max drawdown ≈ $435

Low trade count

That is healthy.

But understand:

When trend days hit, it will lose.

If volatility regime changes structurally, edge degrades.

Strengths

Smooth equity curve

Compatible with prop trailing drawdown

Emotionally manageable

Predictable trade frequency

Weaknesses

Underperforms in trending months

Can have clusters of 3–4 losses

Needs volatility filter to stay safe

Won’t consistently produce $350 every day

Psychological Fit

This system fits traders who:

Prefer frequent small wins

Can accept occasional flat weeks

Care more about survival than speed

Avoid revenge trading

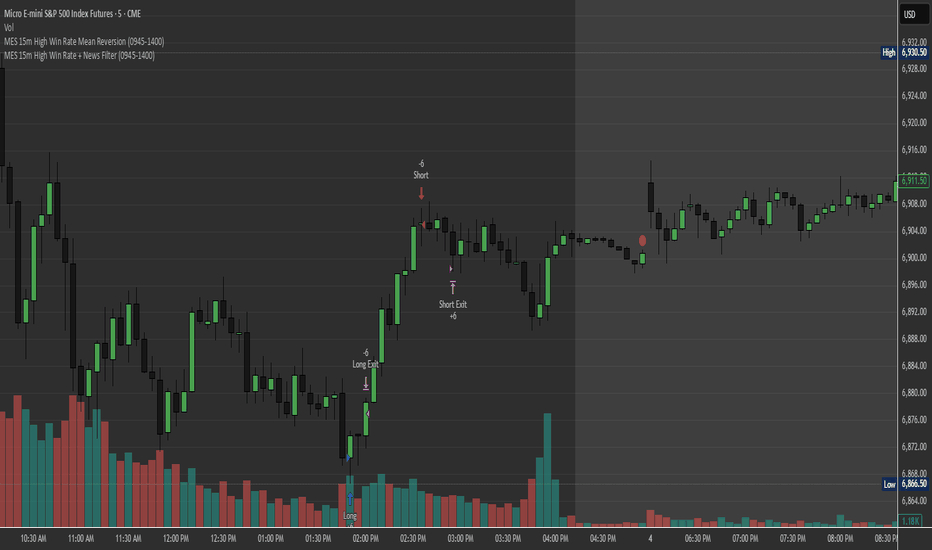

รูป Preview

Pine Script Source

//@version=6

strategy("MES 15m High Win Rate Mean Reversion",

overlay=true,

pyramiding=0,

default_qty_type=strategy.fixed,

default_qty_value=6)

// === SETTINGS ===

stopPoints = 5.0

targetPoints = 6.0

dailyMaxLoss = 450.0

dailyMaxProfit = 700.0

maxTradesPerDay = 2

sessionInput = input.session("0945-1400", "NY Session")

// === SESSION FILTER ===

inSession = not na(time(timeframe.period, sessionInput))

// === DAILY RESET ===

var float dayStartEquity = na

var int tradeCount = 0

var bool longTaken = false

var bool shortTaken = false

newDay = dayofmonth != dayofmonth[1]

if newDay

dayStartEquity := strategy.equity

tradeCount := 0

longTaken := false

shortTaken := false

dailyPnL = strategy.equity - dayStartEquity

tradingAllowed =

dailyPnL > -dailyMaxLoss and

dailyPnL < dailyMaxProfit and

tradeCount < maxTradesPerDay

// === VOLATILITY COMPRESSION FILTER ===

atr = ta.atr(14)

atrCompression = atr < ta.sma(atr, 30)

// === VWAP + BOLLINGER EXTREMES ===

vwapValue = ta.vwap(close)

basis = ta.sma(close, 20)

dev = ta.stdev(close, 20)

upperBand = basis + 2 * dev

lowerBand = basis - 2 * dev

longCondition =

close < lowerBand and

close < vwapValue and

atrCompression and

not longTaken

shortCondition =

close > upperBand and

close > vwapValue and

atrCompression and

not shortTaken

// === ENTRY ===

if (longCondition and inSession and tradingAllowed)

strategy.entry("Long", strategy.long)

tradeCount += 1

longTaken := true

if (shortCondition and inSession and tradingAllowed)

strategy.entry("Short", strategy.short)

tradeCount += 1

shortTaken := true

// === EXIT ===

if (strategy.position_size > 0)

strategy.exit("Long Exit", from_entry="Long",

stop=strategy.position_avg_price - stopPoints,

limit=strategy.position_avg_price + targetPoints)

if (strategy.position_size < 0)

strategy.exit("Short Exit", from_entry="Short",

stop=strategy.position_avg_price + stopPoints,

limit=strategy.position_avg_price - targetPoints)