SmartDCA by TradeAkademi

ลิงก์ TradingView

คำอธิบาย

SmartDCA is a single-direction (Long or Short) step-based DCA strategy with adaptive take-profit and structured risk management.

All core parameters are fully user-configurable. The strategy logic does not enforce a fixed trading style; behavior depends entirely on user-selected settings.

General Structure

The strategy operates in one direction at a time (Long or Short).

All position management logic is applied relative to the selected direction.

The following components are fully controlled by the user:

Trade direction (Long / Short)

Entry model

Entry filters

Take-profit percentage

DCA distance percentage

TP/DCA increment scaling mode

Order size model

Maximum DCA steps

Risk management options

Exit model selection

The strategy plan is visualized either across the entire chart history or within a user-defined custom backtest date range.

Entry Configuration

Users can select the entry model:

Structural breakout

RSI reversal

Trend flip

None (manual disable)

Optional entry filters refine signal selection based on:

Reward space

Entry quality

RSI extremity

Fair value (VWMA)

Trend alignment

DCA & Position Scaling

After initial entry:

Additional DCA orders are triggered when price deviates from the average position price by the defined DCA percentage.

DCA distance and take-profit levels expand step-by-step according to the selected scaling mode.

Order size progression depends on the selected order size model.

Maximum DCA steps define the upper exposure limit.

This ensures the full theoretical risk is bounded and visible.

Exit Models

Users can choose the exit behavior:

Fixed take-profit

Structure-based exit

Adaptive Fast

Adaptive Slow

Protect Profit

Trend Ended

None

All exits are executed using market orders.

Additional Risk Controls

Optional risk features include:

DCA Compression (partial size reduction after recovery)

Defensive Profit Exit

Trend Soft Stop (breakeven protection after trend reversal)

These mechanisms are configurable and do not override the predefined maximum DCA limit.

Visualization & Reporting

The strategy provides:

Active position tracking

DCA step monitoring

Position notional transparency

Trend strength visualization

Historical DCA performance summary

Users may restrict execution to a custom backtest range or allow the strategy to operate across the full visible chart history.

Risk Disclosure

The maximum DCA step defines the full predefined risk envelope.

Strong and sustained one-directional trends may lead to full DCA utilization.

The strategy does not attempt unlimited recovery.

Users are responsible for configuring position sizing and DCA parameters relative to their capital.

This script is for educational and analytical purposes only and does not constitute investment advice.

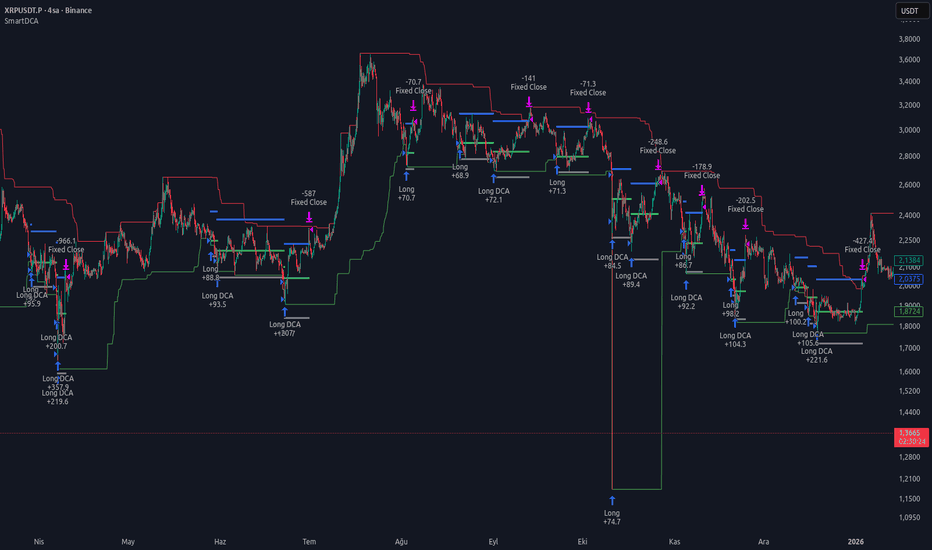

รูป Preview

Pine Script Source

// This Pine Script® code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © trade_akademi

//@version=6

strategy("SmartDCA", overlay=true, fill_orders_on_standard_ohlc = true, initial_capital= 100000, default_qty_type=strategy.percent_of_equity, default_qty_value=0.2, commission_type=strategy.commission.percent, commission_value=0.02, pyramiding = 1000, slippage = 5, backtest_fill_limits_assumption = 5, margin_long = 0, margin_short = 0)

// User Settings

sideInput = input.string("Long", title="Trade Direction", options=["Long", "Short"], group="Entry", tooltip="Defines the trading direction of the strategy.")

mainStrategyInput = input.string("Break Default",title="Primary Entry Model",options=["Break Default","RSI Reversal","Trend Flip","None"],group="Entry",tooltip="Defines the core entry logic of the strategy.\n\n" +"Break Default: Enters on structural high/low breaks.\n" +"RSI Reversal: Enters on RSI extreme reversals (oversold/overbought).\n" +"Trend Flip: Enters when the detected main trend changes direction.\n" +"None: Disables new entries.\n\n" +"Entry Filters can be applied separately to refine signal quality.")

mainPeriodInput = input.int(100, title="Main Entry Period", minval=2, maxval=1000, group="Entry", tooltip="Lookback period used to determine local highs/lows for Break_* entry models. Lower values generate earlier and more aggressive entries. Not used in MA_Based mode.")

entryFilterInput = input.string("None",title="Primary Entry Filter",options=["None", "Reward Space", "Entry Quality", "RSI Extremity", "Fair Value", "Trend Alignment"],group="Entry",tooltip="Applies an additional high-level filter to all entry models. None allows unrestricted entries, Trend Only restricts entries to the main trend direction, Fair Price Zone blocks entries far from structurally active price areas, and Momentum Confirmed requires supportive momentum conditions before allowing entry.")

exitModelInput = input.string("Fixed",title = "Exit Model",options = ["Fixed", "Structure Break", "Adaptive Fast", "Adaptive Slow", "Protect Profit", "Trend Ended", "None"],group = "Exit / DCA / TP",tooltip ="Defines how positions are closed. All exits are executed using market orders for faster execution and simplified management.\n\n" +"Fixed: Closes at predefined take-profit level using market execution. No limit orders are placed.\n\n" +"Structure Break: Closes when price breaks the active structural boundary.\n\n" +"Adaptive Fast: Exits on short-term exhaustion signals for quicker profit capture.\n\n" +"Adaptive Slow: Uses a wider structural reference for extended trend participation.\n\n" +"Protect Profit: Locks in profits based on peak PNL and closes on meaningful giveback.\n\n" +"Trend Ended: Closes when the active trend direction changes. Recommended only when using Trend Flip entry mode.\n\n" +"None: Disables automated exits.")

takeProfitPercentInput = input.float(12, title="Take Profit (%)", step=0.01, minval=0, group="Exit / DCA / TP", tooltip="Defines the base take-profit percentage. When trend-following exit is enabled, this value represents the activation threshold.")

dcaPercentInput = input.float(4, title="DCA Distance (%)", step=0.01, minval=0, group="Exit / DCA / TP", tooltip="Percentage deviation from average price required to trigger an additional DCA order.")

tpDcaIncrementModeInput = input.string("Percent", title="TP/DCA Increment Scaling Mode", options=["Percent", "Fixed"], group="Exit / DCA / TP", tooltip="Percent: TP and DCA thresholds scale multiplicatively (aggressive).\nFixed: Linear increase for deeper and more resilient DCA structures.")

tpIncrementValueInput = input.float(5, title="TP Increment Value", step=0.1, group="Exit / DCA / TP", tooltip="Determines how the take-profit level increases after each DCA step, depending on the selected scaling mode.")

dcaIncrementValueInput = input.float(5, title="DCA Increment Value", step=0.1, group="Exit / DCA / TP", tooltip="Controls how the DCA distance expands after each additional DCA step.")

maxDcaStepsInput = input.int(15,title="Maximum DCA Steps",step=1,minval=1,group="Risk",tooltip="Maximum number of position layers including the initial entry. Higher values increase recovery flexibility but also increase capital exposure and structural risk.")

orderSizeModeInput = input.string("Progressive",title="Order Size Model",options=["Default", "Balanced", "Progressive", "Aggressive"],group="Risk",tooltip="Defines how DCA order sizes grow.\n\nDefault: Equal-sized orders.\nBalanced: Gradual laddered growth.\nProgressive: Linear step-based scaling.\nAggressive: Front-loaded aggressive scaling.")

defensiveProfitExitInput = input.bool(false,title="Defensive Profit Exit",group="Risk",tooltip="Enables early profit protection logic that closes the position before full target extension when short-term reversal risk increases. Designed to reduce giveback during unstable conditions.")

dcaCompressionModeInput = input.bool(false,title="DCA Compression Mode",group="Risk",tooltip="Reduces position size after recovery to release capital and lower structural exposure.\n\n" +"Off: No reduction is applied.\n" +"On: Automatically trims position size once recovery conditions are met.")

trendStopInput = input.bool(false,title="Trend Soft Stop",group="Risk",tooltip="Activates breakeven stop if trend flips against the current position. No immediate exit. Locks downside risk while allowing potential recovery.")

useCustomRangeInput = input.bool(true, title="Use Custom Backtest Range", group="Backtest", tooltip="Limits strategy execution to the specified date range for backtesting purposes.")

startDateInput = input.time(timestamp("2025-01-01 00:00"), title="Backtest Start Date", group="Backtest",confirm=true)

endDateInput = input.time(timestamp("2030-01-01 00:00"), title="Backtest End Date", group="Backtest",confirm=true)

activePositionTableInput = input.bool(true, title="Show Active Position Table", group="Table", tooltip="Displays detailed information about the currently active position.")

tableLeftInput = input.string("Off",title = "Left Panel Table",options = ["Off","Strategy Summary","DCA History","DCA & Order Summary"],group = "Table",tooltip = "Select which table to display on the left panel.\n\n" +"Off: No table displayed.\n" +"Strategy Summary: Shows current strategy configuration and key parameters.\n" +"DCA History: Displays historical DCA step statistics and close performance.\n" +"DCA & Order Summary: Shows order size progression and position scaling structure.")

showHighLowLevelsInput = input.bool(true, title="Show Structure High/Low Levels", group="Visual", tooltip="Visualizes the high/low structure used by Break_* entry models.")

showTrendInput = input.bool(false,title = "Show Trend Structure",group = "Visual",tooltip = "Highlights the detected main market trend on the chart using background coloring. The trend is based on confirmed structural breakouts to avoid false flips during pullbacks.")

showRsiInput = input.bool(false, title="Show RSI Overbought/Oversold Zones", group="Visual", tooltip="Highlights RSI <30 and RSI >70 zones using background shading.")

show4hRsiInput = input.bool(false, title="Show 4H RSI Zones", group="Visual", tooltip="Highlights overbought and oversold zones based on 4-hour RSI.")

showRsiDivergencesInput = input.bool(false, title="Show RSI Divergence Zones", group="Visual", tooltip="Displays visual markers for RSI divergence areas.")

inDateRange = not useCustomRangeInput or (time >= startDateInput and time <= endDateInput)

// Runtime Settings

takeProfitPercentEffective = takeProfitPercentInput

tpIncrementValueEffective = tpIncrementValueInput

dcaPercentEffective = dcaPercentInput

dcaIncrementValueEffective = dcaIncrementValueInput

exitModelEffective = exitModelInput

dcaCompressionEffective = dcaCompressionModeInput

defensiveProfitExitEffective = defensiveProfitExitInput

defensiveProfitExitLimitEffective = 4

defensiveProfitExitProximityEffective = 40

// Static Vars

var mainPeriod = mainPeriodInput

var baseOrderSize = float(na)

var adaptiveTakeProfitPrice = float(na)

var adaptiveDcaPrice = float(na)

var currentDcaStep = int(na)

var lastDcaPrice = float(na)

var lastDcaBar = int(na)

var lastExitBar = int(na)

var lastExitTime = int(na)

var entryBlocked = bool(false)

var dcaBlocked = bool(false)

var orderSize = float(na)

var orderQty = float(na)

var estimatedPnl = float(na)

var currentPnl = float(na)

var maxPnlSeen = float(na)

var minPnlSeen = float(na)

var maxClosePnlSeen = float(na)

var minClosePnlSeen = float(na)

var maxClosePnlSeenAt = float(na)

var minClosePnlSeenAt = float(na)

var protectRatio = float(na)

var protectFloorPnl = float(na)

var protectFloorClosePnl = float(na)

var compressionLock = bool(false)

var compressCount = int(0)

var waitBeforeReCompress = int(0)

var trendStopModeEnabled = bool(false)

var breakevenStopEnabled = bool(false)

var inefficiencyExitEnabled = bool(false)

var exitMode = bool(false)

var protectProfitMode = bool(false)

var totalPositionCount = 0

var totalDcaStepCount = 0

var allTimeMaxDca = int(na)

var allTimeMaxPnl = float(na)

var allTimeMinPnl = float(na)

var allTimeMaxNotional = float(na)

var crossTp = int(na)

var int[] dcaCloseCounts = array.new_int(maxDcaStepsInput + 1, 0)

var float[] dcaClosePnl = array.new_float(maxDcaStepsInput + 1, 0.0)

// Strategy

lowest = ta.lowest(low,mainPeriod)

highest = ta.highest(high,mainPeriod)

lowest20 = ta.lowest(close,20)

highest20 = ta.highest(close,20)

lowest50 = ta.lowest(close,50)

highest50 = ta.highest(close,50)

rsi=ta.rsi(close,14)

rsi_4h=request.security(syminfo.tickerid, "240", ta.rsi(close, 14),gaps=barmerge.gaps_off, lookahead=barmerge.lookahead_off)

rsi_divergence_short=close>ta.highest(high,100)[1] and rsi<ta.highest(rsi,100)[1]

rsi_divergence_long=close<ta.lowest(low,100)[1] and rsi>ta.lowest(rsi,100)[1]

no_recent_short = not (rsi_divergence_short[1] or rsi_divergence_short[2] or rsi_divergence_short[3] or rsi_divergence_short[4] or rsi_divergence_short[5])

no_recent_long = not (rsi_divergence_long[1] or rsi_divergence_long[2] or rsi_divergence_long[3] or rsi_divergence_long[4] or rsi_divergence_long[5])

fairValue = ta.vwma(close, 200)

// Trend tespiti

var float baseHigh = na

var float baseLow = na

var int watchDir = 0 // 1 = up watch, -1 = down watch

var int trend = 0 // 1 = up, -1 = down, 0 = neutral

if watchDir == 0

// yukarı aday

if highest > highest[2]

watchDir := 1

baseHigh := highest

// aşağı aday

else if lowest < lowest[2]

watchDir := -1

baseLow := lowest

if watchDir == 1

// ikinci, daha güçlü kırılım

if highest > baseHigh

trend := 1

watchDir := 0

baseHigh := na

// izleme iptali (yapı bozuldu)

else if lowest < lowest[2]

watchDir := 0

baseHigh := na

if watchDir == -1

// ikinci kırılım

if lowest < baseLow

trend := -1

watchDir := 0

baseLow := na

// izleme iptali

else if highest > highest[2]

watchDir := 0

baseLow := na

// final flag

trendOk = (sideInput == "Long" and trend == 1) or (sideInput == "Short" and trend == -1)

isLong = sideInput == "Long"

isShort = sideInput == "Short"

// === TREND STRENGTH ===

var int trendBreakCount = 0

var float lastBreakLevel = na

// Trend yeni başladığında reset

if trend != trend[1]

trendBreakCount := 0

lastBreakLevel := na

// UP trend continuation

if trend == 1

if na(lastBreakLevel)

lastBreakLevel := highest

if highest > lastBreakLevel

trendBreakCount += 1

lastBreakLevel := highest

// DOWN trend continuation

if trend == -1

if na(lastBreakLevel)

lastBreakLevel := lowest

if lowest < lastBreakLevel

trendBreakCount += 1

lastBreakLevel := lowest

// Trend bgcolor

maxStrength = 10

strengthRatio = math.min(trendBreakCount / maxStrength, 1.0)

clampedRatio = math.min(strengthRatio, 1.0)

// yumuşatma (1.0 = linear, 1.5–2.0 güzel akıyor)

smoothRatio = math.pow(clampedRatio, 1.6)

// opacity hesap

opacityRaw = 100 - int(smoothRatio * 50)

// minimum 50'ye sabitle

trendOopacity = math.max(60, math.min(90, opacityRaw))

// Cooldown

twoDaysMs = 2 * 24 * 60 * 60 * 1000

cooldownOk = na(lastExitTime) or (time - lastExitTime > twoDaysMs)

// Functions

// Calculate open profit or loss for the open positions.

tradeOpenPnl() =>

sumProfit = 0.0

for tradeNo = 0 to strategy.opentrades - 1

sumProfit += strategy.opentrades.profit(tradeNo)

result = sumProfit

f_openRealizedPnl() =>

var float openRealized = 0.0

var float lastNetProfit = na

// ilk çağrı

if na(lastNetProfit)

lastNetProfit := strategy.netprofit

// pozisyon kapandıysa reset

if strategy.position_size == 0

openRealized := 0.0

lastNetProfit := strategy.netprofit

// pozisyon açıkken netprofit düşüşünü yakala (realized)

if strategy.position_size != 0

delta = strategy.netprofit - lastNetProfit

// sadece realized kayıplar/kârlar (reduce, partial close)

if delta != 0

openRealized += delta

lastNetProfit := strategy.netprofit

openRealized

f_getOrderSize(baseSize, step, mode) =>

size = baseSize

tmpStep = na(step) ? 0 : step

pair = math.ceil((tmpStep + 1) / 2)

if mode == "Default" // Flat

size := baseSize

else if mode == "Balanced" // Ladder

m = 1.0 + (pair - 1) * 0.5

size := baseSize * m

else if mode == "Progressive" // eski Smart (istersen kaldırabilirsin)

size := baseSize * pair

else if mode == "Aggressive" // Hammer

m = 1.0 + (pair - 1) * 1.5

size := baseSize * m

else

size := baseSize

size

f_getMaxPositionSize(baseSize,maxSteps,mode) =>

total = 0.0

for step = 0 to maxSteps - 1

stepSize = f_getOrderSize(baseSize,step,mode)

total += stepSize

total

f_calcTpDca(baseTp, baseDca, step, mode, tpInc, dcaInc) =>

tp = baseTp

dca = baseDca

if step <= 1

[tp, dca]

else

for i = 2 to step

if mode == "Percent"

tp := tp * (1 + tpInc / 100)

dca := dca * (1 + dcaInc / 100)

else

tp := tp + tpInc

dca := dca + dcaInc

[tp, dca]

f_norm(val, minVal, maxVal)=>

math.min(math.max((val - minVal) / (maxVal - minVal), 0), 1)

trendColor(ma,opacity=50) =>

if (ma>ma[1])

color.new(color.green, opacity)

else

color.new(color.red, opacity)

// Position

positionSize = strategy.position_size

hasPosition = positionSize != 0

avgPrice = strategy.position_avg_price

openTrades = strategy.opentrades

changeClosedTrades = ta.change(strategy.closedtrades)

positionSide = positionSize>0 ? "Long" : "Short"

baseOrderSize := na(baseOrderSize) ? math.abs(strategy.opentrades.size(0) * strategy.opentrades.entry_price(0)) : baseOrderSize

positionOpenPrice = strategy.opentrades.entry_price(0)

lastEntryPrice = strategy.opentrades.entry_price(strategy.opentrades - 1)

lastOrderSize = strategy.opentrades.size(openTrades-1) * strategy.opentrades.entry_price(openTrades-1)

totalNotional = math.abs(positionSize*avgPrice)

dcaFillRatio = currentDcaStep / maxDcaStepsInput

avgDcaStep = math.round(totalDcaStepCount / totalPositionCount,2)

avgPnl = math.round(strategy.netprofit / totalPositionCount,2)

currentPnl := tradeOpenPnl()

firstOrderPnl = strategy.opentrades.profit(0)

lastOrderPnl = strategy.opentrades.profit(strategy.opentrades - 1)

openRealizedPnl = f_openRealizedPnl()

effectivePnl = openRealizedPnl + currentPnl

orderSize := f_getOrderSize(baseOrderSize,currentDcaStep,orderSizeModeInput)

orderQty := math.abs(orderSize / close)

maxPositionSize = f_getMaxPositionSize(baseOrderSize,maxDcaStepsInput,orderSizeModeInput)

// TP DCA calculations

[adaptiveTakeProfitPercent, adaptiveDcaPercent] = f_calcTpDca(takeProfitPercentEffective,dcaPercentEffective,currentDcaStep,tpDcaIncrementModeInput,tpIncrementValueEffective,dcaIncrementValueEffective)

if na(adaptiveTakeProfitPrice)

adaptiveTakeProfitPrice := positionSide == "Long" ? avgPrice * (1 + (adaptiveTakeProfitPercent / 100)) : avgPrice * (1 - (adaptiveTakeProfitPercent / 100))

tpExtension = (close - adaptiveTakeProfitPrice) / (adaptiveTakeProfitPrice - avgPrice)

tmpAdaptiveDcaPriceLast = positionSide == "Long" ? lastDcaPrice * (1 - adaptiveDcaPercent / 100) : lastDcaPrice * (1 + adaptiveDcaPercent / 100)

tmpAdaptiveDcaPriceAvg = positionSide == "Long" ? avgPrice * (1 - adaptiveDcaPercent / 100) : avgPrice * (1 + adaptiveDcaPercent / 100)

if na(adaptiveDcaPrice)

adaptiveDcaPrice := positionSide == "Long" ? math.min(tmpAdaptiveDcaPriceLast,tmpAdaptiveDcaPriceAvg) : math.max(tmpAdaptiveDcaPriceLast,tmpAdaptiveDcaPriceAvg)

// position calculations

if hasPosition

estimatedPnl:=math.abs(strategy.position_size*strategy.position_avg_price * (1 + adaptiveTakeProfitPercent / 100) - strategy.position_size*strategy.position_avg_price)

maxPnl = sideInput=="Long" ? (high - avgPrice) * math.abs(strategy.position_size) : (avgPrice - low) * math.abs(strategy.position_size)

minPnl = sideInput=="Long" ? (low - avgPrice) * math.abs(strategy.position_size) : (avgPrice - high) * math.abs(strategy.position_size)

maxPnlSeen := na(maxPnlSeen) ? maxPnl : math.max(maxPnlSeen, maxPnl)

minPnlSeen := na(minPnlSeen) ? minPnl : math.min(minPnlSeen, minPnl)

maxClosePnlSeen := na(maxClosePnlSeen) ? currentPnl : math.max(maxClosePnlSeen, currentPnl)

minClosePnlSeen := na(minClosePnlSeen) ? currentPnl : math.min(minClosePnlSeen, currentPnl)

maxClosePnlSeenAt := na(maxClosePnlSeenAt) ? close : math.max(maxClosePnlSeenAt, close)

minClosePnlSeenAt := na(minClosePnlSeenAt) ? close : math.min(minClosePnlSeenAt, close)

if minPnlSeen<allTimeMinPnl or na(allTimeMinPnl)

allTimeMinPnl:=minPnlSeen

if maxPnlSeen<allTimeMaxPnl or na(allTimeMaxPnl)

allTimeMaxPnl:=maxPnlSeen

if currentDcaStep>allTimeMaxDca or na(allTimeMaxDca)

allTimeMaxDca:=currentDcaStep

if totalNotional>allTimeMaxNotional or na(allTimeMaxNotional)

allTimeMaxNotional:=totalNotional

// Cross TP

if close<adaptiveTakeProfitPrice and (high>adaptiveTakeProfitPrice or high[1]>adaptiveTakeProfitPrice)

if na(crossTp)

crossTp := 1

else

crossTp += 1

// Profit Protect

profitStrength = maxClosePnlSeen / math.max(estimatedPnl, 1)

dynamicProtectRatio = profitStrength < 10 ? 0.40 : profitStrength < 20 ? 0.50 : profitStrength < 50 ? 0.60 : profitStrength < 60 ? 0.70 : 0.80

baseProtectRatio = 0.40

pnlStallRatio = currentPnl / math.max(maxClosePnlSeen, 1)

stallBoost = pnlStallRatio < 0.85 ? 0.10 : 0.0

// --- zaman bazlı drift

var int barsSinceMaxPnl = 0

if currentPnl >= maxClosePnlSeen

barsSinceMaxPnl := 0

else

barsSinceMaxPnl += 1

timeStepBars = 20

timeBoostStep = 0.02

maxTimeBoost = 0.15

timeBoost = math.min(math.floor(barsSinceMaxPnl / timeStepBars) * timeBoostStep,maxTimeBoost)

// --- nihai koruma oranı

protectRatio := math.min(math.max(baseProtectRatio,dynamicProtectRatio + stallBoost + timeBoost),0.85)

protectFloorClosePnl := maxClosePnlSeen * protectRatio

// Auto Exit Model

if exitModelInput == "Auto"

exitModelEffective := "Fixed"

if (hasPosition)

strengthOk = trendOk and (strengthRatio == 1 or strengthRatio>strengthRatio[3])

newTrend = isLong ? trendOk and trend[3] == -1 : trendOk and trend[3] == 1

if strengthOk or newTrend

exitModelEffective := "Protect Profit"

else if trendOk

exitModelEffective := "Adaptive Slow"

else if not trendOk

exitModelEffective := "Fixed"

if (currentPnl > estimatedPnl * 50)

exitModelEffective := "Adaptive Fast"

else if (currentPnl > estimatedPnl * 20)

exitModelEffective := "Adaptive Slow"

// Stop

if inDateRange and hasPosition

if trendStopInput and ((isLong and trend == -1) or (isShort and trend == 1)) and strengthRatio == 1 and currentDcaStep>1 and currentPnl < 0

breakevenStopEnabled := true

if breakevenStopEnabled and effectivePnl > 0

if sideInput == "Long"

strategy.close("Long", comment="Breakeven Stop")

else if sideInput=="Short"

strategy.close("Short", comment="Breakeven Stop")

entryBlocked := true

lastExitBar := bar_index

lastExitTime := time

if inefficiencyExitEnabled and math.abs(openRealizedPnl)>estimatedPnl and effectivePnl>math.abs(openRealizedPnl) * 0.1

strategy.close(isLong ? "Long" : "Short", comment="Inefficiency Exit")

entryBlocked := true

lastExitBar := bar_index

lastExitTime := time

// Defensive Profit Exit

if inDateRange and hasPosition and defensiveProfitExitEffective and currentDcaStep >= defensiveProfitExitLimitEffective and effectivePnl > 0

defensiveProfitExitProximity = defensiveProfitExitProximityEffective / 100.0

if sideInput == "Long" and (close - avgPrice) / (adaptiveTakeProfitPrice - avgPrice) >= defensiveProfitExitProximity

strategy.close("Long", comment="Defensive Profit Exit")

entryBlocked := true

lastExitBar := bar_index

lastExitTime := time

else if sideInput=="Short" and (avgPrice - close) / (avgPrice - adaptiveTakeProfitPrice) >= defensiveProfitExitProximity

strategy.close("Short", comment="Defensive Profit Exit")

entryBlocked := true

lastExitBar := bar_index

lastExitTime := time

// Range dışına çıkış anı

exitedDateRange = useCustomRangeInput and not inDateRange and inDateRange[1]

if exitedDateRange and strategy.position_size != 0

strategy.close_all(comment="Backtest Range End")

// Open Position

if inDateRange and not hasPosition and cooldownOk and not entryBlocked

entrySignal = false

entryFilter = true

openPosition = false

// ENTRY SIGNALS

if mainStrategyInput == "Break Default"

entrySignal := isLong ? ((low < lowest[1] and close < high[1]) or close < lowest[1]) : ((high > highest[1] and close > low[1]) or close > highest[1])

else if mainStrategyInput=="RSI Reversal"

entrySignal := isLong ? rsi <= 30 : rsi >= 70

else if mainStrategyInput=="Trend Flip"

entrySignal := isLong ? trend == 1 and trend[1] != 1 : trend == -1 and trend[1] != -1

// ENTRY FILTERS

if entryFilterInput == "Reward Space"

entryFilter := isLong ? highest[1] > close * (1 + adaptiveTakeProfitPercent / 100) : lowest[1] < close * (1 - adaptiveTakeProfitPercent / 100)

else if entryFilterInput == "Entry Quality"

entryFilter := isLong ? highest[1] > close * (1 + adaptiveTakeProfitPercent / 100) and (close - low) / (high - low) < 0.4 : lowest[1] < close * (1 - adaptiveTakeProfitPercent / 100) and (high - close) / (high - low) < 0.4

else if entryFilterInput == "RSI Extremity"

entryFilter := isLong ? rsi <= 30 : rsi >= 70

else if entryFilterInput == "Fair Value"

entryFilter := isLong ? close <= fairValue : close >= fairValue

else if entryFilterInput == "Trend Alignment"

entryFilter := isLong ? trend == 1 : trend == -1

openPosition := entrySignal and entryFilter

if openPosition

strategy.entry(isLong ? "Long" : "Short", isLong ? strategy.long : strategy.short, comment = isLong ? "Long" : "Short", qty = orderQty)

lastDcaPrice := close

currentDcaStep := 1

totalPositionCount += 1

adaptiveTakeProfitPrice := na

adaptiveDcaPrice := na

// Add Position

if inDateRange and hasPosition and not entryBlocked and not dcaBlocked

canDca = false

if sideInput=="Long"

canDca:=(close<lastDcaPrice * (1 - (adaptiveDcaPercent / 100)) and close<avgPrice * (1 - (adaptiveDcaPercent / 100)))

else

canDca:=(close>lastDcaPrice * (1 + (adaptiveDcaPercent / 100)) and close>avgPrice * (1 + (adaptiveDcaPercent / 100)))

if canDca and currentDcaStep<maxDcaStepsInput

strategy.entry(sideInput == "Long" ? "Long" : "Short", sideInput=="Long" ? strategy.long : strategy.short, qty=orderQty, comment = sideInput == "Long" ? "Long DCA" : "Short DCA")

lastDcaPrice:=close

lastDcaBar := bar_index

currentDcaStep += 1

adaptiveTakeProfitPrice := na

adaptiveDcaPrice := na

waitBeforeReCompress -= 1

if waitBeforeReCompress == 0

compressionLock := false

// Take Profit

if inDateRange and hasPosition

var exitSignal = bool(false)

// Fixed Exit (mevcut davranış)

if exitModelEffective=="Fixed"

exitSignal := effectivePnl>0 and ((sideInput == "Long" and close>adaptiveTakeProfitPrice) or (sideInput == "Short" and close<adaptiveTakeProfitPrice))

if exitSignal

if sideInput == "Long"

strategy.close("Long", comment="Fixed Close")

else

strategy.close("Short", comment="Fixed Close")

else if exitModelEffective=="Adaptive Fast"

exitSignal := effectivePnl>0 and (sideInput == "Long" and close < lowest20[1] and close>avgPrice * 1.01) or (sideInput == "Short" and close>highest20[1] and close < avgPrice * 0.99)

if exitSignal

if sideInput == "Long"

strategy.close("Long", comment="Adaptive Fast Exit")

else

strategy.close("Short", comment="Adaptive Fast Exit")

else if exitModelEffective=="Adaptive Slow"

exitSignal := effectivePnl>0 and (sideInput == "Long" and close < lowest50[1] and close>avgPrice * 1.01) or (sideInput == "Short" and close>highest50[1] and close < avgPrice * 0.99)

if exitSignal

if sideInput == "Long"

strategy.close("Long", comment="Adaptive Slow Exit")

else

strategy.close("Short", comment="Adaptive Slow Exit")

else if exitModelEffective=="Structure Break"

exitSignal := effectivePnl>0 and (sideInput == "Long" and high > highest[1] and close>avgPrice * 1.01) or (sideInput == "Short" and low<lowest[1] and close < avgPrice * 0.99)

if exitSignal

if sideInput == "Long"

strategy.close("Long", comment="Structure Break Exit")

else

strategy.close("Short", comment="Structure Break Exit")

else if exitModelEffective=="Protect Profit"

if effectivePnl>0 and (sideInput == "Long" and close < lowest50[1] and close>avgPrice * 1.01) or (sideInput == "Short" and close>highest50[1] and close < avgPrice * 0.99)

protectProfitMode := true

if protectProfitMode

exitSignal := effectivePnl > estimatedPnl and effectivePnl <= protectFloorClosePnl and maxClosePnlSeen > 0

if exitSignal

if sideInput == "Long"

strategy.close("Long", comment="Protect Profit Exit")

else

strategy.close("Short", comment="Protect Profit Exit")

protectProfitMode := false

if close<avgPrice

protectProfitMode := false

else if exitModelEffective=="Trend Ended"

exitSignal := (sideInput == "Long" and trend[1] == 1 and trend == -1) or (sideInput == "Short" and trend[1] == -1 and trend == 1)

if exitSignal

strategy.close(sideInput == "Long" ? "Long" : "Short", comment="Trend Exit")

if exitSignal

entryBlocked := true

lastExitBar := bar_index

// Dca Compression

if hasPosition and dcaCompressionEffective

canCompress = (currentDcaStep >= 3 and dcaFillRatio<1 and not compressionLock and

((sideInput == "Long" and ((dcaFillRatio>0.80 and currentPnl>minClosePnlSeen * 0.10) or (high>avgPrice and close>high[1]))) or

(sideInput == "Short" and ((dcaFillRatio>0.80 and currentPnl>minClosePnlSeen * 0.10) or (low<avgPrice and close<low[1]))))

)

if canCompress

stepReduction = dcaFillRatio <= 0.40 ? 1 : dcaFillRatio <= 0.60 ? 2 : dcaFillRatio <= 0.90 ? 3 : 4

compressStep = math.max(currentDcaStep - stepReduction, 1)

compressionComment = "Dca Compression (-" + str.tostring(stepReduction) + " DCA)"

reduceNotional = 0.0

for i = 0 to stepReduction - 1

stepIndex = (currentDcaStep - 1) - i

if stepIndex >= 0

reduceNotional += f_getOrderSize(baseOrderSize,stepIndex,orderSizeModeInput)

reduceQty = reduceNotional / close

if sideInput == "Long"

strategy.close("Long", qty = reduceQty, comment = compressionComment)

else

strategy.close("Short", qty = reduceQty, comment = compressionComment)

currentDcaStep := compressStep

lastDcaPrice := (close + lastDcaPrice) / 2

adaptiveDcaPrice := na

compressionLock := true

compressCount += 1

waitBeforeReCompress := compressStep

// Reset

if strategy.position_size == 0 and strategy.position_size[1] != 0

dcaIndex = math.min(currentDcaStep, maxDcaStepsInput)

array.set(dcaCloseCounts,dcaIndex,array.get(dcaCloseCounts, dcaIndex) + 1)

array.set(dcaClosePnl,dcaIndex,array.get(dcaClosePnl, dcaIndex) + strategy.netprofit - strategy.netprofit[1])

totalDcaStepCount := totalDcaStepCount + currentDcaStep

takeProfitPercentEffective := takeProfitPercentInput

dcaPercentEffective := dcaPercentInput

dcaBlocked := false

currentDcaStep := na

positionSize := na

lastDcaPrice := na

lastDcaBar := na

compressionLock := false

compressCount := 0

waitBeforeReCompress := 0

trendStopModeEnabled := false

breakevenStopEnabled := false

inefficiencyExitEnabled := false

exitMode := false

protectProfitMode := false

maxPnlSeen := na

minPnlSeen := na

maxClosePnlSeen := na

minClosePnlSeen := na

maxClosePnlSeenAt := na

minClosePnlSeenAt := na

crossTp := na

newPositionOpened = barstate.isconfirmed and strategy.position_size != 0 and strategy.position_size[1] == 0

if newPositionOpened

lastDcaPrice := na(lastDcaPrice) ? close : lastDcaPrice

currentDcaStep := 1

if entryBlocked and bar_index > lastExitBar

entryBlocked := false

// Shape

trendStopActivated = hasPosition and trendStopModeEnabled and not trendStopModeEnabled[1]

plotchar(trendStopActivated,char="S",location=location.abovebar,color=color.orange,size = size.tiny,display = display.pane)

// Bg color

bgcolor(useCustomRangeInput ? (inDateRange ? na : color.new(color.gray, 90)) : na, title="Outside Backtest Range")

bgcolor(inDateRange and showTrendInput ? trend == 1 ? color.new(color.green, trendOopacity) : trend == -1 ? color.new(color.red, trendOopacity) : na : na)

bgcolor(inDateRange and rsi<=30 ? color.new(color.green, showRsiInput ? 90 : 100) : na)

bgcolor(inDateRange and rsi>=70 ? color.new(color.red, showRsiInput ? 90 : 100) : na)

bgcolor(inDateRange and rsi_4h<=30 ? color.new(color.green, show4hRsiInput ? 90 : 100) : na)

bgcolor(inDateRange and rsi_4h>=70 ? color.new(color.red, show4hRsiInput ? 90 : 100) : na)

bgcolor(inDateRange and rsi_4h<=30 and rsi<=30 ? color.new(color.green, show4hRsiInput ? 80 : 100) : na)

bgcolor(inDateRange and rsi_4h>=70 and rsi>=70 ? color.new(color.red, show4hRsiInput ? 80 : 100) : na)

bgcolor(inDateRange and rsi_divergence_short and no_recent_short ? color.new(color.orange, showRsiDivergencesInput ? 90 : 100) : na)

bgcolor(inDateRange and rsi_divergence_long and no_recent_long ? color.new(color.lime, showRsiDivergencesInput ? 90 : 100) : na)

plot(lowest[1],color = color.new(color.green, 0),title = "Lowest",display = showHighLowLevelsInput ? display.pane : display.none)

plot(highest[1],color = color.new(color.red, 0),title = "Highest",display = showHighLowLevelsInput ? display.pane : display.none)

plot(hasPosition ? lastDcaPrice : na,title="Last Entry Price",display = display.status_line)

plot(strategy.position_avg_price,title="Position AVG Price (Strategy)",color=positionSide == "Long" ? color.green : color.red,linewidth = 1,style=plot.style_circles)

plot(hasPosition ? adaptiveTakeProfitPrice : na,title="TP Price",color=color.blue,linewidth = 1,style=plot.style_circles)

plot(hasPosition ? adaptiveDcaPrice : na,title="DCA Price",color=color.gray,linewidth = 1,style=plot.style_circles, display = display.pane)

plot(hasPosition ? adaptiveTakeProfitPercent : na,title="TP %", color=color.green, linewidth=1, display=display.status_line)

plot(hasPosition ? adaptiveDcaPercent : na,title="DCA %", color=color.orange, linewidth=1, display=display.status_line)

plot(hasPosition ? currentDcaStep : na,title="Current DCA Step",color=color.white,linewidth = 1,display=display.status_line)

plot(hasPosition ? lastOrderSize : na,title="Step Order Size",color=color.orange,linewidth = 1,display=display.status_line)

plot(hasPosition ? totalNotional : na,title="Position Notional Size",color=color.fuchsia,linewidth = 1,display=display.status_line)

plot(hasPosition ? currentPnl : na,title="Active PNL",color=currentPnl>0 ? color.green : color.red,linewidth = 1,display=display.status_line)

plot(hasPosition ? openRealizedPnl : na,title="Realized PNL",color=openRealizedPnl>0 ? color.green : color.red,linewidth = 1,display=display.status_line)

plot(hasPosition ? estimatedPnl : na,title="Target PNL",color=color.blue,linewidth = 1,display=display.status_line)

//plot(strengthRatio, title="Trend Strength", display = display.status_line)

plot(strategy.netprofit,title="Total Strategy PNL",color=strategy.netprofit>0 ? color.green : color.red,linewidth = 1,display=display.status_line)

// Visual Tables

clrHeaderBg = color.rgb(45, 45, 45)

clrLabelBg = color.rgb(60, 60, 60)

clrValueBg = color.rgb(20, 20, 20)

clrHeaderTxt = color.white

clrLabelTxt = color.silver

clrValueTxt = color.white

clrPos = color.rgb(46, 204, 113) // yeşil

clrNeg = color.rgb(231, 76, 60) // kırmızı

clrWarn = color.rgb(241, 196, 15) // sarı

clrCountBase = color.green

clrRatioBase = color.green

f_header(_table, _text, _row) =>

table.cell(_table,0,_row,_text,text_color=clrHeaderTxt,bgcolor=clrHeaderBg,text_halign=text.align_center,text_size = size.small)

table.merge_cells(_table,0,_row,1,_row)

f_row(_table,_row,_label,_value,_bgLabel,_bgValue,_txtValue) =>

table.cell(_table,0,_row," " + _label,text_color=clrLabelTxt,bgcolor=_bgLabel,text_halign=text.align_left,text_size = size.small)

table.cell(_table,1,_row,str.tostring(_value) + " ",text_color=_txtValue,bgcolor=_bgValue,text_halign=text.align_right,text_size = size.small)

f_header3(_table, _text, _row) =>

table.cell(_table,0,_row,_text,text_color=clrHeaderTxt,bgcolor=clrHeaderBg,text_halign=text.align_center,text_size = size.small)

table.merge_cells(_table,0,_row,2,_row)

f_row3(_table, _row, _label, _value1, _value2, _bgLabel, _bgValue1, _bgValue2, _txtValue) =>

table.cell(_table,0,_row," " + _label,text_color = clrLabelTxt,bgcolor = _bgLabel,text_halign = text.align_left,text_size = size.small)

table.cell(_table,1,_row,str.tostring(_value1) + " ",text_color = _txtValue,bgcolor = _bgValue1,text_halign = text.align_right,text_size = size.small)

table.cell(_table,2,_row,str.tostring(_value2) + " ",text_color = _txtValue,bgcolor = _bgValue2,text_halign = text.align_right,text_size = size.small)

f_header4(_table, _text, _row) =>

table.cell(_table,0,_row,_text,text_color=clrHeaderTxt,bgcolor=clrHeaderBg,text_halign=text.align_center,text_size = size.small)

table.merge_cells(_table,0,_row,3,_row)

f_row4(_table, _row, _label, _v1, _v2, _v3, _bgLabel, _bgV1, _bgV2, _bgV3, _txtValue) =>

table.cell(_table, 0, _row, " " + _label, text_color=clrLabelTxt, bgcolor=_bgLabel, text_halign=text.align_left,text_size = size.small)

table.cell(_table, 1, _row, str.tostring(_v1) + " ", text_color=_txtValue, bgcolor=_bgV1, text_halign=text.align_right,text_size = size.small)

table.cell(_table, 2, _row, str.tostring(_v2) + " ", text_color=_txtValue, bgcolor=_bgV2, text_halign=text.align_right,text_size = size.small)

table.cell(_table, 3, _row, str.tostring(_v3) + " ", text_color=_txtValue, bgcolor=_bgV3, text_halign=text.align_right,text_size = size.small)

f_dimColor(_clr, _isDim) =>

_isDim ? color.new(_clr, 80) : _clr

f_gradient(_value, _max, _baseClr) =>

_max > 0 ? color.new(_baseClr, 80 - int(60 * math.min(math.abs(_value) / _max, 1))) : color.new(_baseClr, 80)

if tableLeftInput == "Strategy Summary"

var table planTable = table.new(position = position.bottom_left,columns=2,rows=50,border_width = 1,border_color = color.gray)

f_header(planTable, "🔎 Strategy Overview", 0)

f_row(planTable,1, "Direction", sideInput,clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,2, "Entry Model", mainStrategyInput,clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,3, "Entry Filter", entryFilterInput,clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,4, "Entry Lookback Period", mainPeriodInput,clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,5, "Exit Model", exitModelEffective,clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,6, "Order Size Model", orderSizeModeInput,clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,7, "Max DCA Steps", maxDcaStepsInput,clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,8, "Base Order Size", baseOrderSize,clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,9, "Estimated Max Notional ~", math.ceil(maxPositionSize),clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,10, "Take Profit (%)", takeProfitPercentInput,clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,11, "DCA Distance (%)", dcaPercentInput,clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,12, "TP / DCA Scaling Mode", tpDcaIncrementModeInput,clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,13, "TP Increment (%)", tpIncrementValueInput,clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,14, "DCA Increment (%)", dcaIncrementValueInput,clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,15, "Total Position Count", totalPositionCount,color.blue, color.blue, clrValueTxt)

f_row(planTable,16, "Total DCA Step Count", totalDcaStepCount,clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,17, "Average DCA Steps", avgDcaStep,clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,18, "All-Time Max DCA Steps", allTimeMaxDca,clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,19, "All-Time Max Notional", math.round(allTimeMaxNotional),clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,20, "All-Time Realized PNL", math.round(strategy.netprofit,2),clrLabelBg, strategy.netprofit>0 ? clrPos : clrNeg, clrValueTxt)

f_row(planTable,21, "All-Time Avg Pnl", avgPnl,clrLabelBg, clrValueBg, clrValueTxt)

f_row(planTable,22, "All-Time Max Drawdown", math.round(allTimeMinPnl,2),clrLabelBg, clrValueBg, clrNeg)

else if tableLeftInput == "DCA History"

maxCount = array.max(dcaCloseCounts)

maxPnl = math.max(math.abs(array.max(dcaClosePnl)),math.abs(array.min(dcaClosePnl)))

var table dcaSummaryTable = table.new(position = position.bottom_left,columns = 4,rows = maxDcaStepsInput + 2,border_width = 1,border_color = color.gray)

f_header4(dcaSummaryTable, "📜 DCA History", 0)

for i = 1 to maxDcaStepsInput

count = array.get(dcaCloseCounts, i)

pnl = array.get(dcaClosePnl, i)

ratio = totalPositionCount > 0? (count / totalPositionCount) * 100: 0.0

isEmpty = count == 0

countBg = f_dimColor(f_gradient(count, maxCount, clrCountBase),isEmpty)

ratioBg = f_dimColor(f_gradient(ratio, 100, clrRatioBase),isEmpty)

pnlBaseClr = pnl > 0 ? clrPos : pnl < 0 ? clrNeg : clrValueBg

pnlBg = f_dimColor(f_gradient(pnl, maxPnl, pnlBaseClr),isEmpty)

f_row4(dcaSummaryTable,i,str.tostring(i) + " DCA",count,str.tostring(math.round(ratio, 2)) + "%",math.round(pnl, 2),f_dimColor(clrLabelBg, isEmpty),countBg,ratioBg,pnlBg,clrValueTxt)

else if tableLeftInput == "DCA & Order Summary"

// --- maksimum teorik pozisyon

maxPositionSizeTable = f_getMaxPositionSize(baseOrderSize,maxDcaStepsInput,orderSizeModeInput)

// --- max değerler (renk skalası için)

var float maxOrderSize = 0.0

var float maxTotalSize = 0.0

var float totalPosSize = 0.0

totalPosSize := 0

for i = 0 to maxDcaStepsInput - 1

orderSizeStep = f_getOrderSize(baseOrderSize, i, orderSizeModeInput)

totalPosSize += orderSizeStep

maxOrderSize := math.max(maxOrderSize, orderSizeStep)

maxTotalSize := math.max(maxTotalSize, totalPosSize)

// --- tablo

var table dcaOrderTable = table.new(position = position.bottom_left,columns = 4,rows = maxDcaStepsInput + 2,border_width = 1,border_color = color.gray)

f_header4(dcaOrderTable, "📦 DCA Order & Notional Summary", 0)

// --- satırlar

totalPosSize := 0

for i = 0 to maxDcaStepsInput - 1

step = i + 1

orderSizeStep = f_getOrderSize(baseOrderSize, i, orderSizeModeInput)

totalPosSize += orderSizeStep

shareRatio = maxPositionSizeTable > 0 ? (orderSizeStep / maxPositionSizeTable) * 100 : 0.0

orderBg = f_gradient(orderSizeStep, maxOrderSize, clrCountBase)

totalBg = f_gradient(totalPosSize, maxTotalSize, clrRatioBase)

f_row4(dcaOrderTable,step,"DCA " + str.tostring(step),math.round(orderSizeStep, 2),math.round(totalPosSize, 2),str.tostring(math.round(shareRatio, 2)) + "%",clrLabelBg,orderBg,totalBg,clrValueBg,clrValueTxt)

if activePositionTableInput

var table posTable = na

if not hasPosition and not na(posTable)

table.delete(posTable)

posTable := na

if hasPosition and na(posTable)

posTable := table.new(position = position.top_right,columns = 2,rows = 15,border_width = 1,border_color = color.gray)

if hasPosition and not na(posTable)

f_header(posTable, "🟢 Active Position", 0)

f_row(posTable, 2, "DCA Step", str.format("{0}/{1}", currentDcaStep, maxDcaStepsInput),clrLabelBg, clrValueBg, currentDcaStep >= maxDcaStepsInput * 0.7 ? clrNeg : currentDcaStep >= maxDcaStepsInput * 0.5 ? clrWarn : clrPos)

f_row(posTable, 3, "Max Notional ~", math.round(maxPositionSize),clrLabelBg, clrValueBg, clrValueTxt)

f_row(posTable, 4, "Take Profit (%)", math.round(adaptiveTakeProfitPercent,2),clrLabelBg, clrValueBg, clrValueTxt)

f_row(posTable, 5, "DCA (%)", math.round(adaptiveDcaPercent,2),clrLabelBg, clrValueBg, clrValueTxt)

f_row(posTable, 6, "Current Notional", math.round(totalNotional),clrLabelBg, clrValueBg, clrValueTxt)

f_row(posTable, 7, "Next Order Size ➡", math.round(orderSize),clrLabelBg, color.gray, clrValueTxt)

f_row(posTable, 8, "Target PNL ~", math.round(estimatedPnl, 2),clrLabelBg, clrValueBg, color.blue)

f_row(posTable, 9, "Unrealized PNL", math.round(currentPnl, 2),clrLabelBg, currentPnl > 0 ? clrPos : clrNeg, clrValueTxt)

f_row(posTable, 10, "Realized PNL", math.round(openRealizedPnl, 2),clrLabelBg, clrValueBg, openRealizedPnl > 0 ? color.green : color.red)

f_row(posTable, 11, "Max PNL", math.round(maxClosePnlSeen, 2),clrLabelBg, clrValueBg, maxClosePnlSeen > 0 ? color.green : color.red)

f_row(posTable, 12, "Min PNL", math.round(minClosePnlSeen, 2),clrLabelBg, clrValueBg, minClosePnlSeen > 0 ? color.green : color.red)

if not hasPosition and na(posTable)

nextPosTable = table.new(position = position.top_right,columns = 2,rows = 15,border_width = 1,border_color = color.gray)

f_header(nextPosTable, "⌛ Next Position", 0)

f_row(nextPosTable, 2, "Direction", sideInput,clrLabelBg, clrValueBg, clrValueTxt)

f_row(nextPosTable, 3, "Entry Model", mainStrategyInput,clrLabelBg, clrValueBg, clrValueTxt)

f_row(nextPosTable, 4, "Max DCA Steps", maxDcaStepsInput,clrLabelBg, clrValueBg, clrValueTxt)

f_row(nextPosTable, 5, "Max Notional ~", math.round(maxPositionSize),clrLabelBg, clrValueBg, clrValueTxt)

f_row(nextPosTable, 6, "Initial Order Size", math.round(baseOrderSize),clrLabelBg, color.blue, clrValueTxt)