ADX Dynamic Zone Inside the SuperTrend with Support / Resistant

ลิงก์ TradingView

คำอธิบาย

I like Simple Strategy and just code one using super trend and ADX

But like All super trend strategy buy and sell signal most of the time are to late

So I am using the super trend like indicator for trend direction and ADX

Dynamic buy or sell zone for pull back and if direction is ok we get in trade but only when we have support for long or resistant for short

Take profit is fix % and stop is Trailing stop

There is A choice if you want to use fixed sum for the trades or increase the size of the trade after # of losing trades

The increase of the size is working like D'Alembert System

Thanks to Trading view and pinecoders.com for the build in indicators and code

If any Questions Let Me Know

Happy Trading

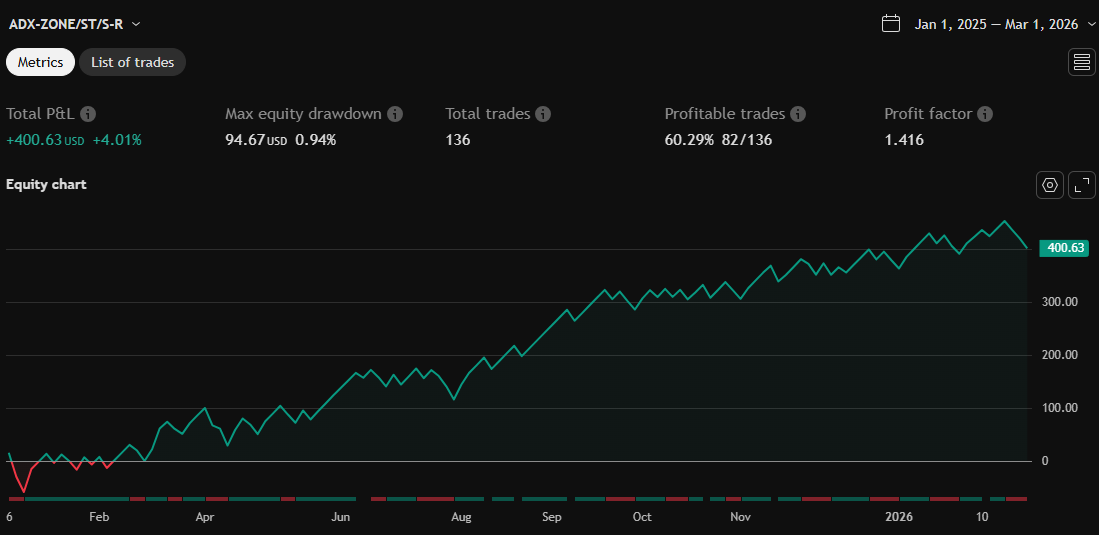

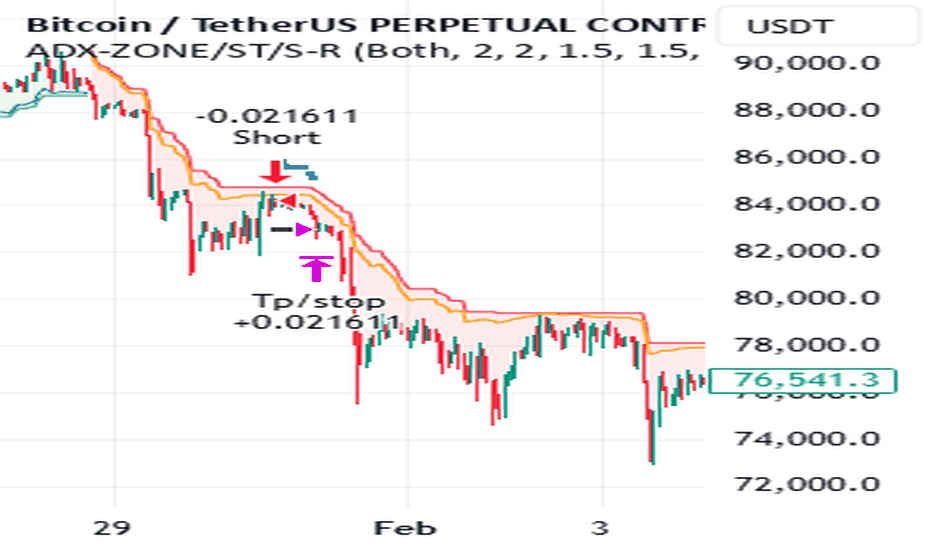

รูป Preview

Pine Script Source

// This Pine Script® code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fullmax

//@version=6

strategy(title = 'ADX-ZONE/ST/S-R', overlay = true, pyramiding = 0)

//

tradedir = input.string('Both', title = 'Trade Direction', options = ['Long', 'Short', 'Both'])

// trail stop inputs

longTrailPerc = input.float(2.0, title = 'Trail Long Loss (%)', minval = 0.0, step = 0.1) * 0.01

shortTrailPerc = input.float(2.0, title = 'Trail Short Loss (%)', minval = 0.0, step = 0.1) * 0.01

///tps

tp_levelL = input.float(title="Take Profit long (%)", defval=1.5, step = 0.1)

tp_levelS = input.float(title="Take Profit short (%)", defval=1.5, step = 0.1)

//// super trend

atrPeriod = input.int(5, 'ATR Length', minval = 1)

factor = input.float(3.02, 'Factor', minval = 0.01, step = 0.01)

[supertrend, direction] = ta.supertrend(factor, atrPeriod)

supertrend := barstate.isfirst ? na : supertrend

upd = direction < 0 ? supertrend : na

dnd = direction < 0 ? na : supertrend

supertrend := barstate.isfirst ? na : supertrend

upTrend = plot(direction < 0 ? supertrend : na, "Up Trend", color = color.green, style = plot.style_linebr)

downTrend = plot(direction < 0 ? na : supertrend, "Down Trend", color = color.red, style = plot.style_linebr)

bodyMiddle = plot(barstate.isfirst ? na : (open + close) / 2, "Body Middle",display = display.none)

fill(bodyMiddle, upTrend, title = "Uptrend background", color = color.new(color.green, 90), fillgaps = false)

fill(bodyMiddle, downTrend, title = "Downtrend background", color = color.new(color.red, 90), fillgaps = false)

///// pivot S/R

S_R = input.bool(true, title="Support-Res")

sup = input.int(33, title="Lookback (Sup)", minval=1)

res = input.int(17, title="Lookback (Res)", minval=1)

support = ta.lowest(low[1], sup)

resistan = ta.highest(high[1], res)

entrysup = low >= support

entryres = high <= resistan

///// ADX cal

adxlen = input(1, title = "ADX Smoothing")

dilen = input(20, title = "DI Length")

dirmov(len) =>

up = ta.change(high)

down = -ta.change(low)

plusDM = na(up) ? na : (up > down and up > 0 ? up : 0)

minusDM = na(down) ? na : (down > up and down > 0 ? down : 0)

truerange = ta.rma(ta.tr, len)

plus = fixnan(100 * ta.rma(plusDM, len) / truerange)

minus = fixnan(100 * ta.rma(minusDM, len) / truerange)

[plus, minus]

adx(dilen, adxlen) =>

[plus, minus] = dirmov(dilen)

sum = plus + minus

adx = 100 * ta.rma(math.abs(plus - minus) / (sum == 0 ? 1 : sum), adxlen)

sig = adx(dilen, adxlen)

////bay and sell zone from the trend

buyzone = upd * (1 + sig / 10000)

sellzone = dnd * (1 - sig / 10000)

plot(buyzone, "Buy zone", color = color.blue, style = plot.style_linebr)

plot(sellzone, "Sell Zone", color = color.orange, style = plot.style_linebr)

/// bay and sell signal

buy = low < buyzone and entrysup

sell = high > sellzone and entryres

// Calculate the take-profit prices

tp_price_long = strategy.position_avg_price * (1 + tp_levelL / 100)

tp_price_short = strategy.position_avg_price * (1 - tp_levelS / 100)

// Determine trail stop

longStopPrice = 0.0

shortStopPrice = 0.0

longStopPrice := if strategy.position_size > 0

stopValue = close * (1 - longTrailPerc)

math.max(stopValue, longStopPrice[1])

else

0

shortStopPrice := if strategy.position_size < 0

stopValue = close * (1 + shortTrailPerc)

math.min(stopValue, shortStopPrice[1])

else

999999

// Plot stop price and TPs

plot(strategy.position_size > 0 ? longStopPrice : na, color = color.blue, style = plot.style_circles, linewidth = 1, title = 'Long Trail Stop')

plot(strategy.position_size < 0 ? shortStopPrice : na, color = color.blue, style = plot.style_circles, linewidth = 1, title = 'Short Trail Stop')

plot(strategy.position_size > 0 ? tp_price_long : na, color = color.rgb(69, 54, 67), style = plot.style_circles, linewidth = 1, title = 'Long Trail Stop')

plot(strategy.position_size < 0 ? tp_price_short : na, color = color.rgb(69, 54, 67), style = plot.style_circles, linewidth = 1, title = 'Long Trail Stop')

//// size of the trade

SZZ = input(1000, title = 'Size of the trade in USD')

//increase trade cal

increaseT = input.bool(true,title = " Increase size of the trade after # of losing trades ")

nl = input.float(1,minval=1,title = "# of losing trades in the row")

osc = SZZ / close

// Check if there's a new losing trade that increased the streak

loss = (strategy.losstrades > strategy.losstrades[1]) and (strategy.wintrades == strategy.wintrades[1]) and (strategy.eventrades == strategy.eventrades[1])

win = strategy.wintrades > strategy.wintrades[1] and strategy.losstrades == strategy.losstrades[1] and strategy.eventrades == strategy.eventrades[1]

// Determine current losing streak length

streaklen = 0

streaklen := if loss

nz(streaklen[1]) + 1

else

if strategy.wintrades > strategy.wintrades[1] or

strategy.eventrades > strategy.eventrades[1]

0

else

nz(streaklen[1])

/// size increase like D'Alembert

var size_arr = array.from(osc/2, osc, osc, osc/2)

array.size(size_arr)

if win and array.size(size_arr) >= 4

array.shift(size_arr)

array.pop(size_arr)

else if win

size_arr := array.from(osc/2, osc/2, osc/2,osc/2)

if streaklen > nl and loss

array.push(size_arr, value= array.get(size_arr, 1) + array.last(size_arr))

first_elem = array.get(size_arr, 0)

last_elem = array.last(size_arr)

fl = first_elem + last_elem

// strategy orders

if buy and (tradedir == "Long" or tradedir == "Both") and strategy.opentrades == 0

strategy.entry('Long', strategy.long, qty = increaseT == true ? fl : osc)

if sell and (tradedir == "Short" or tradedir == "Both") and strategy.opentrades == 0

strategy.entry('Short', strategy.short,qty = increaseT == true ? fl : osc )

// exit

if strategy.position_size > 0

strategy.exit('Long', stop = longStopPrice, limit=tp_price_long)

if strategy.position_size < 0

strategy.exit('Tp/stop', stop = shortStopPrice,limit=tp_price_short)

////