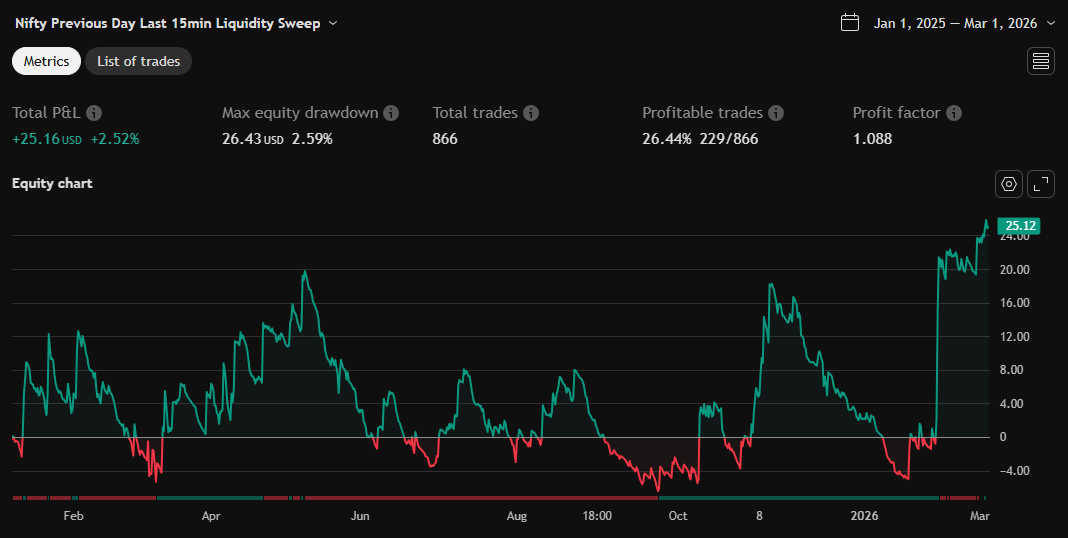

Nifty Previous Day Last 15min Liquidity Sweep

ลิงก์ TradingView

คำอธิบาย

This Nifty strategy targets liquidity sweeps of the previous day's last 15-minute candle (PDH/PDL zone), entering on reversal confirmation for high-probability intraday trades. Use on 15min NIFTY charts during market hours (9:15 AM - 3:30 PM IST).

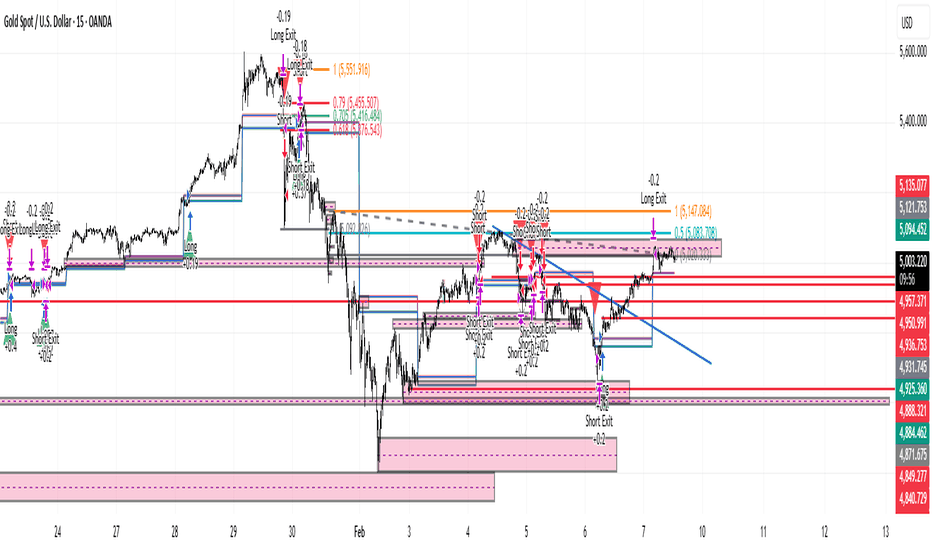

รูป Preview

Pine Script Source

//@version=5

strategy("Nifty Previous Day Last 15min Liquidity Sweep", overlay=true, initial_capital=100000, default_qty_type=strategy.percent_of_equity, default_qty_value=1)

// Inputs

risk_pct = input.float(1.0, "Risk % per Trade")

rr_ratio = input.float(2.0, "Risk:Reward Ratio")

// Detect previous day (India time, NSE 9:15-15:30 IST)

is_new_day = ta.change(time("D"))

var float prev_day_zone_high = na

var float prev_day_zone_low = na

if is_new_day

prev_day_zone_high := high[1] // Last 15min high of prev day (on 15min chart)

prev_day_zone_low := low[1] // Last 15min low

// Plot zone

plot(prev_day_zone_high, "Prev Day High (Entry Zone)", color.red, 2)

plot(prev_day_zone_low, "Prev Day Low (Entry Zone)", color.green, 2)

fill(plot(prev_day_zone_high), plot(prev_day_zone_low), color.new(color.blue, 95), "Entry Zone")

// Liquidity Sweep: Price breaks beyond zone then reverses (close back inside with momentum)

bull_sweep = not na(prev_day_zone_high) and low < prev_day_zone_low and close > prev_day_zone_low // Sweep low, reverse up

bear_sweep = not na(prev_day_zone_high) and high > prev_day_zone_high and close < prev_day_zone_high // Sweep high, reverse down

// Entry on sweep confirmation (next candle close confirms reversal)

long_condition = bull_sweep[1] and close > open // Bullish candle after sweep

short_condition = bear_sweep[1] and close < open // Bearish candle after sweep

// Entries

if long_condition

strategy.entry("Long", strategy.long)

if short_condition

strategy.entry("Short", strategy.short)

// Risk Management

long_sl = prev_day_zone_low

long_tp = close + (rr_ratio * (close - long_sl))

short_sl = prev_day_zone_high

short_tp = close - (rr_ratio * (short_sl - close))

if strategy.position_size > 0

strategy.exit("Long Exit", "Long", stop=long_sl, limit=long_tp)

if strategy.position_size < 0

strategy.exit("Short Exit", "Short", stop=short_sl, limit=short_tp)

// Visuals

plotshape(long_condition, "Long Entry", shape.triangleup, location.belowbar, color.green, size=size.normal)

plotshape(short_condition, "Short Entry", shape.triangledown, location.abovebar, color.red, size=size.normal)

plotshape(bull_sweep, "Bull Sweep", shape.arrowdown, location.belowbar, color.orange)

plotshape(bear_sweep, "Bear Sweep", shape.arrowup, location.abovebar, color.orange)