BP Strategy Malisa

ลิงก์ TradingView

คำอธิบาย

Get money and get rich for free fkc yeah hdhdhsissohdhrhebdnskskskshdd

Bdhsisjsowjdheiekenndhxuxux

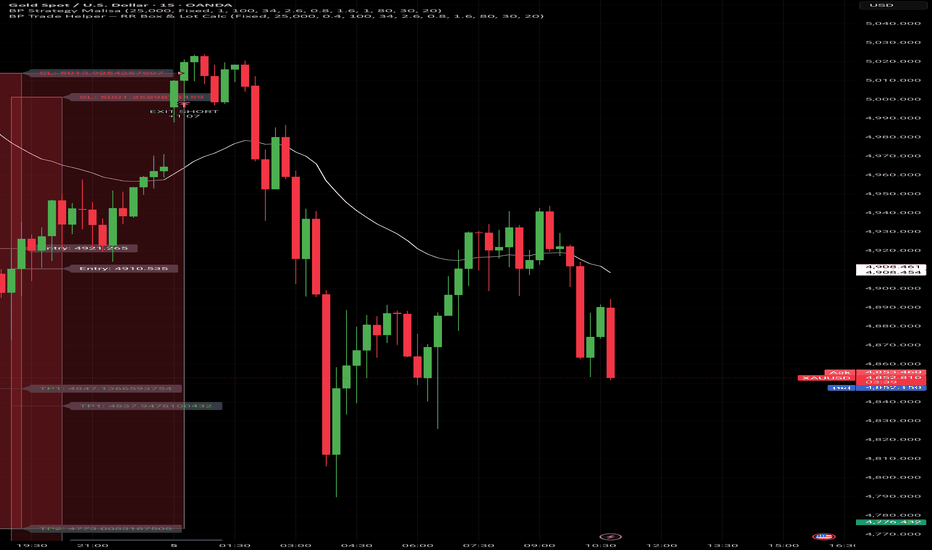

รูป Preview

Pine Script Source

//@version=6

strategy("BP Strategy Malisa", overlay=true, pyramiding=0, calc_on_every_tick=false, default_qty_type=strategy.fixed, default_qty_value=1)

// ===== CAPITAL & RISK INPUTS =====

accountCapital = input.float(10000, "Account Capital (€)", step=100)

riskMode = input.string("Percent", "Risk Mode", options=["Percent", "Fixed"])

riskPercent = input.float(1.0, "Risk % per Trade", step=0.1)

riskFixed = input.float(100, "Fixed € Risk per Trade", step=10)

// ===== STRATEGY INPUTS =====

useSession = input.bool(true, "Enable NY Session")

emaLen = input.int(34, "EMA Length")

slATRmult = input.float(2.6, "SL ATR Mult")

tp1RR = input.float(0.8, "TP1 R:R (BE)")

tpRR = input.float(1.6, "Final TP R:R")

useBreakeven = input.bool(true, "Move SL to BE at TP1")

maxDailyLosses = input.int(2, "Max Losing Trades Per Day")

// ===== FILTERS (KAO NA SLICI) =====

useRSI = input.bool(true, "Use RSI Filter")

rsiOB = input.int(80, "RSI Overbought")

rsiOS = input.int(30, "RSI Oversold")

useADX = input.bool(true, "Use ADX Filter")

adxMin = input.int(37, "ADX Minimum")

// ===== SESSION =====

sessOK = not useSession or not na(time(timeframe.period, "0930-1500", "America/New_York"))

// ===== CORE =====

ema = ta.ema(close, emaLen)

atr = ta.atr(14)

rsi = ta.rsi(close, 14)

[dip, dim, adx] = ta.dmi(14, 14)

bullTrend = close > ema

bearTrend = close < ema

// ===== SIGNALS (S OPCIJAMA) =====

longSignal = sessOK and bullTrend and (not useRSI or rsi < rsiOB) and (not useADX or adx > adxMin)

shortSignal = sessOK and bearTrend and (not useRSI or rsi > rsiOS) and (not useADX or adx > adxMin)

// ===== DAILY LOSS CONTROL =====

var int lossesToday = 0

newDay = dayofmonth(time) != dayofmonth(time[1])

if newDay

lossesToday := 0

canTradeToday = lossesToday < maxDailyLosses

// ===== TRADE STATE =====

var bool tradeActive = false

var bool tradeLong = false

var bool beActive = false

var float entryPrice = na

var float slPrice = na

var float tp1Price = na

var float tpPrice = na

var line entryLine = na

var line slLine = na

var line tp1Line = na

var line tpLine = na

var box tradeBox = na

// ===== RISK CALC FUNCTION =====

calcPositionSize(entry, stop) =>

riskPerTrade = riskMode == "Percent" ? accountCapital * (riskPercent / 100.0) : riskFixed

riskPerUnit = math.abs(entry - stop)

qty = riskPerUnit > 0 ? riskPerTrade / riskPerUnit : 0

qty

// ===== LONG ENTRY =====

if longSignal and not tradeActive and canTradeToday

tradeActive := true

tradeLong := true

beActive := false

entryPrice := close

risk = atr * slATRmult

slPrice := entryPrice - risk

tp1Price := entryPrice + risk * tp1RR

tpPrice := entryPrice + risk * tpRR

qty = calcPositionSize(entryPrice, slPrice)

strategy.entry("LONG", strategy.long, qty=qty)

strategy.exit("EXIT LONG", "LONG", stop=slPrice, limit=tpPrice)

entryLine = line.new(bar_index, entryPrice, bar_index, entryPrice, color=color.gray, width=2)

slLine = line.new(bar_index, slPrice, bar_index, slPrice, color=color.red, width=2)

tp1Line = line.new(bar_index, tp1Price, bar_index, tp1Price, color=color.green, width=1)

tpLine = line.new(bar_index, tpPrice, bar_index, tpPrice, color=color.green, width=2)

tradeBox := box.new(

left = bar_index,

right = bar_index,

top = tpPrice,

bottom = slPrice,

bgcolor = color.new(color.gray, 85),

border_color = color.gray

)

// ===== SHORT ENTRY =====

if shortSignal and not tradeActive and canTradeToday

tradeActive := true

tradeLong := false

beActive := false

entryPrice := close

risk = atr * slATRmult

slPrice := entryPrice + risk

tp1Price := entryPrice - risk * tp1RR

tpPrice := entryPrice - risk * tpRR

qty = calcPositionSize(entryPrice, slPrice)

strategy.entry("SHORT", strategy.short, qty=qty)

strategy.exit("EXIT SHORT", "SHORT", stop=slPrice, limit=tpPrice)

entryLine = line.new(bar_index, entryPrice, bar_index, entryPrice, color=color.gray, width=2)

slLine = line.new(bar_index, slPrice, bar_index, slPrice, color=color.red, width=2)

tp1Line = line.new(bar_index, tp1Price, bar_index, tp1Price, color=color.green, width=1)

tpLine = line.new(bar_index, tpPrice, bar_index, tpPrice, color=color.green, width=2)

tradeBox := box.new(

left = bar_index,

right = bar_index,

top = slPrice,

bottom = tpPrice,

bgcolor = color.new(color.gray, 85),

border_color = color.gray

)

// ===== UPDATE TRADE =====

if tradeActive

line.set_x2(entryLine, bar_index)

line.set_x2(slLine, bar_index)

line.set_x2(tp1Line, bar_index)

line.set_x2(tpLine, bar_index)

box.set_right(tradeBox, bar_index)

if useBreakeven and not beActive

if tradeLong and high >= tp1Price

slPrice := entryPrice

beActive := true

if not tradeLong and low <= tp1Price

slPrice := entryPrice

beActive := true

if tradeLong and low <= slPrice

box.set_bgcolor(tradeBox, color.new(color.red, 80))

lossesToday += 1

tradeActive := false

if tradeLong and high >= tpPrice

box.set_bgcolor(tradeBox, color.new(color.green, 80))

tradeActive := false

if not tradeLong and high >= slPrice

box.set_bgcolor(tradeBox, color.new(color.red, 80))

lossesToday += 1

tradeActive := false

if not tradeLong and low <= tpPrice

box.set_bgcolor(tradeBox, color.new(color.green, 80))

tradeActive := false

// ===== CONTEXT =====

plot(ema, color=color.white)