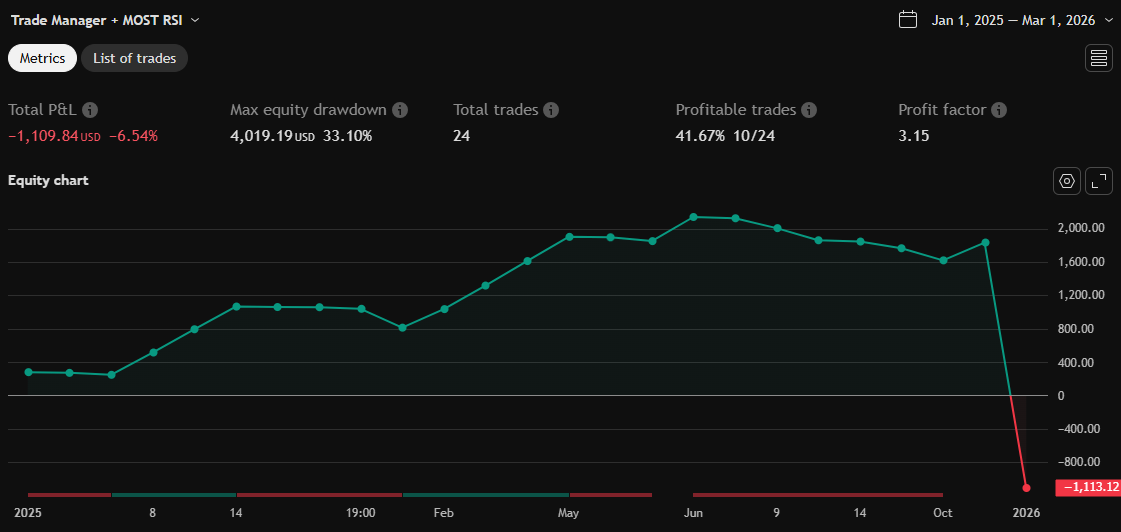

Trade Manager + MOST RSI

ลิงก์ TradingView

คำอธิบาย

📌 Trade Manager + MOST RSI — Adaptive Position Management Strategy

Overview

This strategy combines the MOST‑RSI trend‑reversal model with a fully customizable position management system.

It is designed for traders who want a flexible, visual, and systematic approach to scaling into positions, managing risk, and automating exits.

The script supports both automatic entries (based on MOST‑RSI signals) and manual entries (user‑defined price levels), making it suitable for hybrid discretionary + algorithmic trading.

✨ Key Features

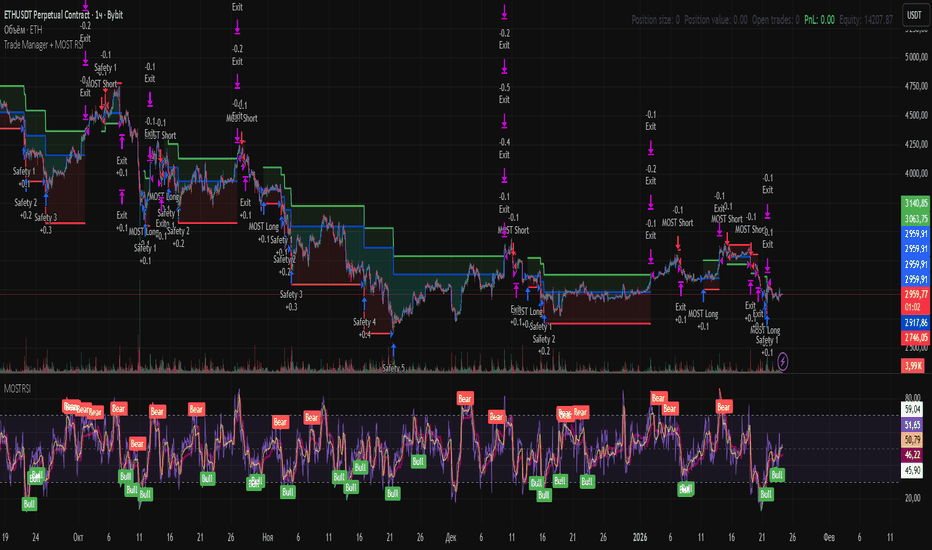

MOST‑RSI Entry Logic

Adaptive RSI‑based trend detection

VAR‑smoothed moving average

Automatic LONG/SHORT signal generation

Configurable sensitivity through MOST Percent, MA Type, and RSI Length

Smart Position Management

Initial order + cascading Safety Orders (SO)

Adjustable deviation, step scaling, and volume scaling

Independent LONG and SHORT deviation settings

Breakeven after N safety orders

Automatic TP placement based on average entry price

Clean Visual Structure

TP lines visible only when a position is open

NEXT SO level with dynamic labeling

Average price line with subtle styling

Transparent background zones for TP, SO, and AVG

Real‑time mini‑table showing position metrics

Manual Entry Mode

Set custom LONG/SHORT entry levels

Automatic line drawing

One‑click reset

Perfect for discretionary setups

📊 Recommended Timeframes

1H — balanced

4H — conservative

MOST‑RSI adapts well across different market conditions.

🔧 Optimization Recommendations

1. Deviation (%)

Trending markets: 4–7%

Ranging markets: 2–3%

Optimize LONG and SHORT separately

2. Safety Order Volume Scale

Typical range: 1.3–1.6

Higher = faster averaging, higher risk

3. Safety Order Step Scale

1.4–1.7 for safer spacing

1.1–1.3 for tighter spacing

4. Take‑Profit

Volatile assets: 2–5%

Stable assets: 1.5–2%

5. Risk Management

Max SO: 5–10 depending on volatility

More SO = safer but more capital required

6. MOST‑RSI Parameters

RSI Length: 14

MA Length: 5

MOST Percent: 7–12%

7. Backtesting

Use at least 1 year of data

Include high‑volatility periods

8. Drawdown Control

If drawdown is too high:

Lower SO volume scale

Reduce max SO

Increase SO step scale

📌 Disclaimer

This script does not guarantee profits and is not financial advice.

Always test strategies on historical data and use proper risk management.

รูป Preview

Pine Script Source

//@version=6

strategy("Trade Manager + MOST RSI", overlay = true, initial_capital = 10000, pyramiding = 9)

lot_precision = input.int(1, "Lot precision", minval = 0, maxval = 8)

show_small_table = input.bool(true, "Show mini-table")

roundQty(q) =>

f = math.pow(10.0, lot_precision)

r = math.ceil(q * f) / f

math.max(1.0 / f, r)

// ================= MANUAL LEVELS =================

use_manual_long = input.bool(false, "Enable manual LONG entries")

use_manual_short = input.bool(false, "Enable manual SHORT entries")

manual_long_price_in = input.float(0.0, "Manual LONG price", step = 0.1)

manual_short_price_in = input.float(0.0, "Manual SHORT price", step = 0.1)

reset_manual_levels = input.bool(false, "Reset manual levels")

var float manual_long_price = na

var float manual_short_price = na

var line long_line = na

var line short_line = na

var bool reset_done = false

if reset_manual_levels and not reset_done

if not na(long_line)

line.delete(long_line)

if not na(short_line)

line.delete(short_line)

manual_long_price := na

manual_short_price := na

long_line := na

short_line := na

reset_done := true

if not reset_manual_levels

reset_done := false

if use_manual_long and manual_long_price_in > 0 and not reset_manual_levels

if na(manual_long_price) or manual_long_price != manual_long_price_in

if not na(long_line)

line.delete(long_line)

manual_long_price := manual_long_price_in

x1 = bar_index > 5000 ? bar_index - 5000 : 0

long_line := line.new(x1, manual_long_price, bar_index, manual_long_price, extend = extend.right, color = color.green)

else

if not na(long_line)

line.delete(long_line)

long_line := na

manual_long_price := na

if use_manual_short and manual_short_price_in > 0 and not reset_manual_levels

if na(manual_short_price) or manual_short_price != manual_short_price_in

if not na(short_line)

line.delete(short_line)

manual_short_price := manual_short_price_in

x1s = bar_index > 5000 ? bar_index - 5000 : 0

short_line := line.new(x1s, manual_short_price, bar_index, manual_short_price, extend = extend.right, color = color.red)

else

if not na(short_line)

line.delete(short_line)

short_line := na

manual_short_price := na

if not na(long_line)

line.set_x2(long_line, bar_index)

if not na(short_line)

line.set_x2(short_line, bar_index)

// ================= MOST RSI =================

Var_Func(source, length) =>

valpha = 2 / (length + 1)

vud1 = source > source[1] ? source - source[1] : 0

vdd1 = source < source[1] ? source[1] - source : 0

vUD = math.sum(vud1, 9)

vDD = math.sum(vdd1, 9)

vCMO = nz((vUD - vDD) / (vUD + vDD))

VAR = 0.0

VAR := nz(valpha * math.abs(vCMO) * source) + (1 - valpha * math.abs(vCMO)) * nz(VAR[1])

VAR

ma(source, length, type) =>

switch type

"SMA" => ta.sma(source, length)

"EMA" => ta.ema(source, length)

"SMMA" => ta.rma(source, length)

"WMA" => ta.wma(source, length)

"VWMA" => ta.vwma(source, length)

"VAR" => Var_Func(source, length)

=> ta.sma(source, length)

rsiLength = input.int(14, "RSI Length")

rsiSource = input.source(close, "RSI Source")

maType = input.string("VAR", "MA Type", options = ["SMA","EMA","SMMA","WMA","VWMA","VAR"])

maLength = input.int(5, "MA Length")

percent = input.float(9.0, "MOST Percent", step = 0.1)

up = ta.rma(math.max(ta.change(rsiSource), 0), rsiLength)

down = ta.rma(-math.min(ta.change(rsiSource), 0), rsiLength)

rsi = down == 0 ? 100 : up == 0 ? 0 : 100 - (100 / (1 + up / down))

rsiMA = ma(rsi, maLength, maType)

exMov = rsiMA

fark = exMov * percent * 0.01

longStop = exMov - fark

longStopPrev = nz(longStop[1], longStop)

longStop := exMov > longStopPrev ? math.max(longStop, longStopPrev) : longStop

shortStop = exMov + fark

shortStopPrev = nz(shortStop[1], shortStop)

shortStop := exMov < shortStopPrev ? math.min(shortStop, shortStopPrev) : shortStop

dir = 1

dir := nz(dir[1], dir)

dir := dir == -1 and exMov > shortStopPrev ? 1 :

dir == 1 and exMov < longStopPrev ? -1 : dir

MOST = dir == 1 ? longStop : shortStop

cro = ta.crossover(exMov, MOST)

cru = ta.crossunder(exMov, MOST)

// ================= RISK SETTINGS =================

enable_long_trades = input.bool(true, "Enable LONG trades")

enable_short_trades = input.bool(true, "Enable SHORT trades")

enable_breakeven = input.bool(false, "Enable breakeven")

breakeven_trades = input.int(1, "Breakeven after N SO")

price_deviation_short = input.float(3.1, "SHORT deviation (%)") / -100

price_deviation_long = input.float(3.1, "LONG deviation (%)") / 100

take_profit_short = input.float(3.0, "SHORT take profit (%)") / 100

take_profit_long = input.float(3.0, "LONG take profit (%)") / 100

first_order = roundQty(input.float(100.0, "Initial order ($)") / close)

safe_order = roundQty(input.float(200.0, "Safety order ($)") / close)

safe_order_volume_scale = input.float(1.49, "SO volume scale")

safe_order_step_scale = input.float(1.37, "SO step scale")

max_safe_order = input.int(8, "Max safety orders")

fee = input.float(0.1, "Exchange fee (%)") / 100

var float initial_order = 0.0

take_profit_level_short = strategy.position_avg_price * (1 - take_profit_short)

take_profit_level_long = strategy.position_avg_price * (1 + take_profit_long)

// ================= ENTRY LOGIC =================

price_deviation = strategy.position_size <= 0 ? price_deviation_short : price_deviation_long

existing_position = strategy.position_size != 0

can_new_entry = strategy.opentrades == 0 and not existing_position

long_signal = cro and enable_long_trades

short_signal = cru and enable_short_trades

long_level_entry = use_manual_long and enable_long_trades and not na(manual_long_price) and close <= manual_long_price

short_level_entry = use_manual_short and enable_short_trades and not na(manual_short_price) and close >= manual_short_price

if can_new_entry

if long_signal

strategy.entry("MOST Long", strategy.long, qty = first_order)

initial_order := close

else if short_signal

strategy.entry("MOST Short", strategy.short, qty = first_order)

initial_order := close

else if long_level_entry

strategy.entry("Manual Long", strategy.long, qty = first_order)

initial_order := close

manual_long_price := na

if not na(long_line)

line.delete(long_line)

long_line := na

else if short_level_entry

strategy.entry("Manual Short", strategy.short, qty = first_order)

initial_order := close

manual_short_price := na

if not na(short_line)

line.delete(short_line)

short_line := na

// ================= SAFETY ORDERS =================

saveorder = 0.0

if safe_order_step_scale == 1.0

saveorder := initial_order - initial_order * price_deviation * safe_order_step_scale * strategy.opentrades

else

saveorder := initial_order - initial_order * (

(price_deviation * math.pow(safe_order_step_scale, strategy.opentrades) - price_deviation)

/ (safe_order_step_scale - 1)

)

ns = str.tostring(strategy.opentrades)

if strategy.opentrades > 0 and strategy.opentrades < max_safe_order and strategy.position_size < 0

so_qty = roundQty(safe_order * math.pow(safe_order_volume_scale, strategy.opentrades - 1))

strategy.entry("Safety " + ns, strategy.short, qty = so_qty, limit = saveorder)

if strategy.opentrades > 0 and strategy.opentrades < max_safe_order and strategy.position_size > 0

so_qty = roundQty(safe_order * math.pow(safe_order_volume_scale, strategy.opentrades - 1))

strategy.entry("Safety " + ns, strategy.long, qty = so_qty, limit = saveorder)

// ================= VISUALIZATION OF NEXT SO =================

next_so_level = strategy.position_size != 0 and strategy.opentrades < max_safe_order ? saveorder : na

so_plot = plot(

next_so_level,

title = "Next Safety Order",

style = plot.style_linebr,

linewidth= 2,

color = color.red

)

// ================= EXITS (TP ORDERS) =================

if strategy.position_size < 0

strategy.exit("Exit", limit = take_profit_level_short)

if strategy.position_size > 0

strategy.exit("Exit", limit = take_profit_level_long)

// ================= TP VISUAL =================

tp_long = plot(

strategy.position_size > 0 ? take_profit_level_long : na,

style = plot.style_linebr,

linewidth= 2,

color = color.green,

title = "TP Long"

)

tp_short = plot(

strategy.position_size < 0 ? take_profit_level_short : na,

style = plot.style_linebr,

linewidth= 2,

color = color.green,

title = "TP Short"

)

// ================= AVG PRICE =================

avg_price_plot = plot(

strategy.position_avg_price,

style = plot.style_linebr,

linewidth= 2,

color = color.new(#004ad4, 10)

)

// ================= BACKGROUND =================

fill(tp_long, plot(close), strategy.position_size > 0 ? color.new(color.green, 90) : color.new(color.green, 100))

fill(tp_short, plot(close), strategy.position_size < 0 ? color.new(color.green, 90) : color.new(color.green, 100))

fill(so_plot, plot(close), color.new(color.red, 90))

fill(avg_price_plot, plot(close), color.new(color.aqua, 90))

// ================= LABELS =================

var label avg_label = na

var label tp_long_label = na

var label tp_short_label = na

var label so_label = na

if barstate.islast

if not na(avg_label)

label.delete(avg_label)

avg_label := label.new(

bar_index, strategy.position_avg_price,

"AVG",

color = color.new(color.aqua, 0),

textcolor = color.white,

style = label.style_label_left,

size = size.tiny

)

if strategy.position_size > 0

if not na(tp_long_label)

label.delete(tp_long_label)

tp_long_label := label.new(

bar_index, take_profit_level_long,

"TP LONG",

color = color.new(color.green, 0),

textcolor = color.white,

style = label.style_label_left,

size = size.tiny

)

else

if not na(tp_long_label)

label.delete(tp_long_label)

tp_long_label := na

if strategy.position_size < 0

if not na(tp_short_label)

label.delete(tp_short_label)

tp_short_label := label.new(

bar_index, take_profit_level_short,

"TP SHORT",

color = color.new(color.green, 0),

textcolor = color.white,

style = label.style_label_left,

size = size.tiny

)

else

if not na(tp_short_label)

label.delete(tp_short_label)

tp_short_label := na

if not na(next_so_level)

if not na(so_label)

label.delete(so_label)

so_label := label.new(

bar_index, next_so_level,

"NEXT SO",

color = color.new(color.red, 0),

textcolor = color.white,

style = label.style_label_left,

size = size.tiny

)

else

if not na(so_label)

label.delete(so_label)

so_label := na

// ================= BREAKEVEN =================

short_order_fee = strategy.position_avg_price * (1 - fee)

long_order_fee = strategy.position_avg_price * (1 + fee)

if strategy.position_size < 0 and strategy.opentrades > breakeven_trades and close < short_order_fee and enable_breakeven

strategy.close_all("Breakeven Short")

if strategy.position_size > 0 and strategy.opentrades > breakeven_trades and close > long_order_fee and enable_breakeven

strategy.close_all("Breakeven Long")

if ta.crossunder(strategy.opentrades, 0.5)

strategy.close_all()

strategy.cancel_all()

// ================= MINI TABLE =================

if show_small_table

sum_qty = strategy.position_size

sum_usd = sum_qty * close

open_trades = strategy.opentrades

open_pnl = strategy.openprofit

eq = strategy.equity

var table mini = table.new(position.top_right, 5, 1)

table.cell(mini, 0, 0, "Position size: " + str.tostring(sum_qty))

table.cell(mini, 1, 0, "Position value: " + str.tostring(sum_usd, format.mintick))

table.cell(mini, 2, 0, "Open trades: " + str.tostring(open_trades))

table.cell(mini, 3, 0, "PnL: " + str.tostring(open_pnl, format.mintick), text_color = open_pnl >= 0 ? color.green : color.red)

table.cell(mini, 4, 0, "Equity: " + str.tostring(eq, format.mintick))