Swing Failure Pattern Strategy Btc Only 5min

ลิงก์ TradingView

คำอธิบาย

🔍 Overview

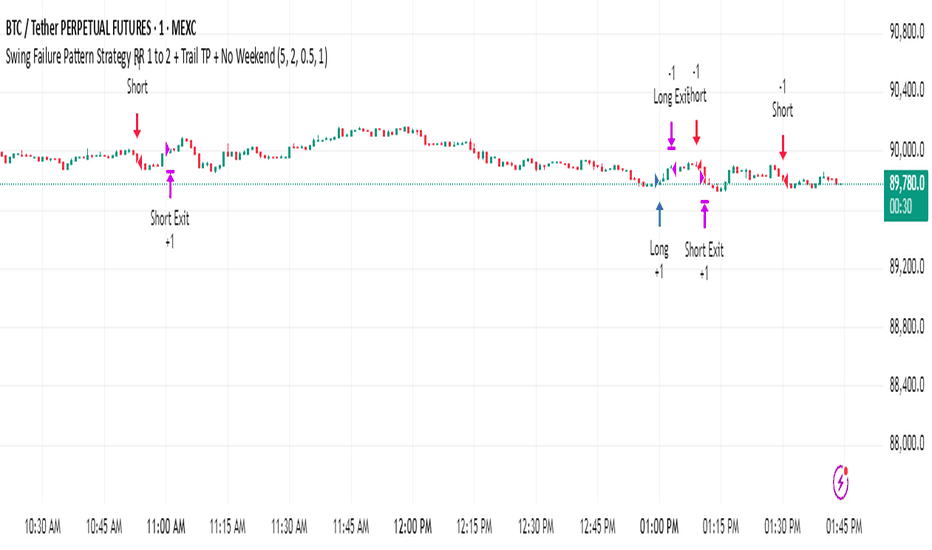

The Swing Failure Pattern (SFP) Strategy is a pure price-action trading system designed to capture liquidity sweeps and market reversals around key swing highs and lows.

It is based on the concept that price often briefly breaks a swing level to trigger stop-losses, then reverses in the opposite direction.

This strategy trades only confirmed SFP setups, ensuring disciplined entries with clearly defined risk.

📈 Bullish SFP (Long Setup)

A Bullish Swing Failure Pattern forms when:

A valid swing low is created

Price wicks below the swing low

The candle closes back above the swing level

Confirmation occurs when price closes above the opposing high

➡️ Action: Enter LONG on the confirmation candle close

📉 Bearish SFP (Short Setup)

A Bearish Swing Failure Pattern forms when:

A valid swing high is created

Price wicks above the swing high

The candle closes back below the swing level

Confirmation occurs when price closes below the opposing low

➡️ Action: Enter SHORT on the confirmation candle close

🛑 Risk Management

Stop Loss

Long → Low of the SFP wick

Short → High of the SFP wick

Take Profit

Fixed Risk : Reward = 1 : 2

All SL and TP levels are fixed at entry (no repainting)

🔁 Trailing Take Profit (Optional)

Trailing TP can be enabled from settings

Trailing starts after 1R profit

Trail distance is R-based and fully adjustable

Works for both long and short trades

⏰ Time Filters

Optional No-Trade on Saturday & Sunday

Prevents new entries during weekends

Active trades continue to manage SL & TP normally

⚙️ Strategy Features

Price-action based (no indicators)

Confirmation-only entries

No repainting logic

Works on all markets and timeframes

Orders executed on candle close

🎯 Best Use Cases

Forex

Indices

Crypto

Futures

Best performance during London & New York sessions

⚠️ Disclaimer

This strategy is intended for educational and backtesting purposes only.

Always test and manage risk appropriately before live trading.

รูป Preview

Pine Script Source

//@version=5

strategy("Swing Failure Pattern Strategy RR 1 to 2 + Trail TP + No Weekend", overlay=true, process_orders_on_close=true)

//==============================

// Inputs

//==============================

len = input.int(5, "Swings", minval=1)

bull = input.bool(true, "Bullish SFP")

bear = input.bool(true, "Bearish SFP")

rr = input.float(2.0, "Risk Reward", minval=0.5)

// Trailing TP

useTrail = input.bool(true, "Enable Trailing TP")

trailRR = input.float(0.5, "Trail Distance (R)", step=0.1)

startRR = input.float(1.0, "Start Trailing After (R)", step=0.1)

// Weekend filter

noWeekend = input.bool(true, "No Trade on Saturday & Sunday")

//==============================

// Time Filter

//==============================

allowTrade = not (noWeekend and (dayofweek == dayofweek.saturday or dayofweek == dayofweek.sunday))

//==============================

// Types

//==============================

type piv

float swing_prc

int swing_bix

float oppos_prc

int oppos_bix

float wick_prc

bool active

bool confirmed

type swing

int bix

float prc

//==============================

// Variables

//==============================

n = bar_index

var swing swingH = swing.new()

var swing swingL = swing.new()

var piv pivH = piv.new()

var piv pivL = piv.new()

//==============================

// Pivot detection

//==============================

ph = ta.pivothigh(len, 1)

pl = ta.pivotlow(len, 1)

//==============================

// BEARISH SFP (SHORT)

//==============================

if bear

if not na(ph)

swingH.bix := n - 1

swingH.prc := ph

sw = swingH.prc

bx = swingH.bix

if allowTrade and high > sw and open < sw and close < sw

opposL = sw

opposB = n

for i = 1 to n - bx - 1

if low[i] < opposL

opposL := low[i]

opposB := n - i

pivH := piv.new(sw, bx, opposL, opposB, high, true, false)

if allowTrade and pivH.active and not pivH.confirmed

if close < pivH.oppos_prc

pivH.confirmed := true

entry = close

stop = pivH.wick_prc

risk = stop - entry

tp = entry - risk * rr

strategy.entry("Short", strategy.short)

if useTrail

strategy.exit("Short Exit", from_entry="Short", stop=stop, limit=tp,

trail_price=entry - risk * startRR, trail_offset=risk * trailRR)

else

strategy.exit("Short Exit", from_entry="Short", stop=stop, limit=tp)

if n - pivH.swing_bix > 500 or close > pivH.swing_prc

pivH.active := false

//==============================

// BULLISH SFP (LONG)

//==============================

if bull

if not na(pl)

swingL.bix := n - 1

swingL.prc := pl

sw = swingL.prc

bx = swingL.bix

if allowTrade and low < sw and open > sw and close > sw

opposH = sw

opposB = n

for i = 1 to n - bx - 1

if high[i] > opposH

opposH := high[i]

opposB := n - i

pivL := piv.new(sw, bx, opposH, opposB, low, true, false)

if allowTrade and pivL.active and not pivL.confirmed

if close > pivL.oppos_prc

pivL.confirmed := true

entry = close

stop = pivL.wick_prc

risk = entry - stop

tp = entry + risk * rr

strategy.entry("Long", strategy.long)

if useTrail

strategy.exit("Long Exit", from_entry="Long", stop=stop, limit=tp,

trail_price=entry + risk * startRR, trail_offset=risk * trailRR)

else

strategy.exit("Long Exit", from_entry="Long", stop=stop, limit=tp)

if n - pivL.swing_bix > 500 or close < pivL.swing_prc

pivL.active := false