Anhnga4.0 - Filter Toggle

ลิงก์ TradingView

คำอธิบาย

INPUTS:

1.5 0.8 (OR 1.6 0.5/0.6)

BE=0.45

1

MAs: 35 135

7

This Pine Script code defines a trading strategy named **"Anhnga4.0 - Filter Toggle"**. It is a trend-following strategy that uses momentum oscillators and moving averages to identify entries, while featuring a specific "Overextension Filter" to avoid buying at the top or selling at the bottom.

Here is a breakdown of how the script works:

---

## 1. Core Trading Logic (The Entry)

The strategy looks for a "perfect storm" of three factors before entering a trade:

* **Momentum (WaveTrend):** It uses the WaveTrend oscillator (`wt1` and `wt2`).

* **Long:** A bullish crossover happens while the oscillator is below the zero line (oversold).

* **Short:** A bearish crossunder happens while the oscillator is above the zero line (overbought).

* **Trend Confirmation:** The price must be on the "correct" side of three different lines: the 20-period Moving Average (BB Basis), the 50-period SMA, and the 200-period SMA.

* **The Window:** You don't have to enter exactly on the cross. The `Signal Window` allows the trade to trigger up to 4 bars after the momentum cross, provided the trend filters align.

## 2. The "Overextension" Filter

This is a unique feature of this script. It calculates the distance between the current price and the **50-period Moving Average**.

* If the price is too far away from the MA (defined by the **ATR Limit**), the script assumes the move is "exhausted."

* If `Enable Overextension Filter?` is on, the strategy will skip these trades to avoid "chasing the pump."

* **Visual Cue:** The chart background turns **purple** when the price is considered overextended.

---

## 3. Risk Management & Exit Strategy

The script manages trades dynamically using Bollinger Bands and Risk:Reward ratios:

| Feature | Description |

| --- | --- |

| **Stop Loss (SL)** | Set at the **Lower Bollinger Band** for Longs and **Upper Band** for Shorts. |

| **Take Profit (TP)** | Calculated based on your **RR Ratio** (default is 2.0). If your risk is $10, it sets the target at $20 profit. |

| **Breakeven** | A "protection" feature. Once the price moves in your favor by a certain amount (the `Breakeven Trigger`), the script moves the Stop Loss to your entry price to ensure a "risk-free" trade. |

---

## 4. Visual Elements on the Chart

* **Green Lines:** Your target price (TP).

* **Red Lines:** Your initial Stop Loss.

* **Yellow Lines:** Indicates the Stop Loss has been moved to **Breakeven**.

* **Purple Background:** High alert—price is overextended; trades are likely being filtered out.

---

## Summary of Settings

* **BB Multiplier:** Controls how wide your initial stop loss is.

* **ATR Limit:** Controls how sensitive the "Overextension" filter is (higher = more trades allowed; lower = stricter filtering).

* **Breakeven Trigger:** Set to 1.0 by default, meaning once you are "1R" (profit equals initial risk) in profit, the stop moves to entry.

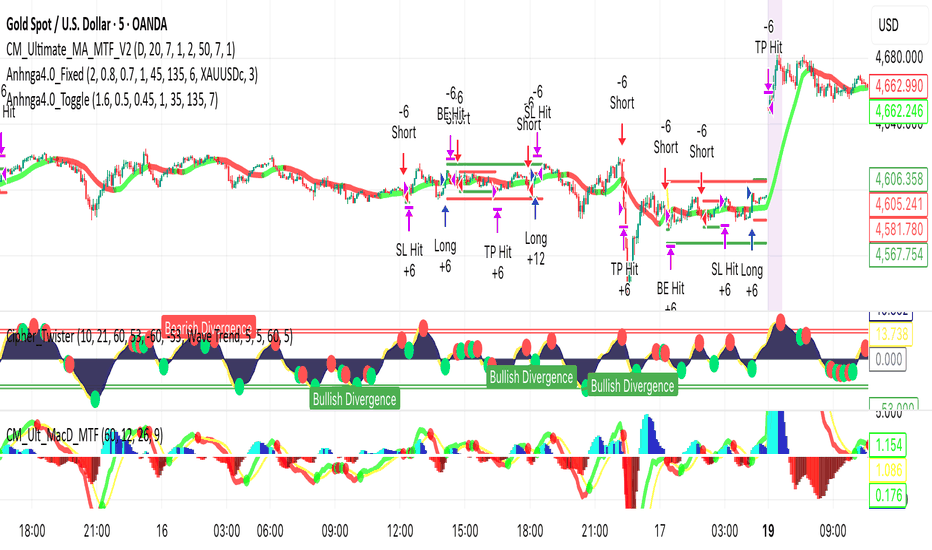

รูป Preview

Pine Script Source

//@version=5

strategy(title="Anhnga4.0 - Filter Toggle", shorttitle="Anhnga4.0_Toggle", overlay=true, initial_capital=5000, default_qty_type=strategy.fixed, default_qty_value=1)

// --- 1. INPUTS ---

bb_mult = input.float(1.5, "BB Stop Loss Multiplier", minval=0.1, step=0.1, group="Risk Management")

rr_ratio = input.float(2.0, "Risk:Reward Ratio", minval=0.1, step=0.1, group="Risk Management")

use_breakeven = input.bool(true, "Enable Breakeven?", group="Breakeven Settings")

be_activation = input.float(1.0, "Breakeven Trigger (RR)", minval=0.1, step=0.1, group="Breakeven Settings")

lookback_window = input.int(4, "Signal Window (Bars)", minval=1, maxval=5, group="Strategy Logic")

ma50_len = input.int(50, "MA 50 Length", group="Strategy Logic")

ma200_len = input.int(200, "MA 200 Length", group="Strategy Logic")

// --- TOGGLE FOR OVEREXTENSION ---

use_overext_filt = input.bool(true, "Enable Overextension Filter?", tooltip="If checked, trades will be skipped if price is too far from MA 50", group="Strategy Logic")

atr_limit = input.float(4.0, "Overextension ATR Limit", minval=1.0, step=0.5, group="Strategy Logic")

// --- 2. INDICATORS ---

ma50 = ta.sma(close, ma50_len)

ma200 = ta.sma(close, ma200_len)

basis = ta.sma(close, 20)

atr = ta.atr(14)

dev = bb_mult * ta.stdev(close, 20)

lower_bb = basis - dev

upper_bb = basis + dev

// WaveTrend

wt1 = ta.ema((hlc3 - ta.ema(hlc3, 10)) / (0.015 * ta.ema(math.abs(hlc3 - ta.ema(hlc3, 10)), 10)), 21)

wt2 = ta.sma(wt1, 4)

// --- 3. LOGIC ---

cross_long = ta.crossover(wt1, wt2) and wt1 < 0

cross_short = ta.crossunder(wt1, wt2) and wt1 > 0

var int last_traded_cross_idx = -1

last_cross_long_idx = ta.valuewhen(cross_long, bar_index, 0)

last_cross_short_idx = ta.valuewhen(cross_short, bar_index, 0)

in_long_window = (bar_index - last_cross_long_idx) <= lookback_window

in_short_window = (bar_index - last_cross_short_idx) <= lookback_window

// Trend Filters

long_ma_filt = (close > basis) and (close > ma50) and (close > ma200)

short_ma_filt = (close < basis) and (close < ma50) and (close < ma200)

// Calculate Overextension

dist_from_ma = math.abs(close - ma50)

is_overextended = dist_from_ma > (atr * atr_limit)

// Filter Logic

ext_check = use_overext_filt ? not is_overextended : true

long_condition = in_long_window and long_ma_filt and ext_check and last_traded_cross_idx != last_cross_long_idx

short_condition = in_short_window and short_ma_filt and ext_check and last_traded_cross_idx != last_cross_short_idx

// --- 4. PERSISTENT EXIT & BREAKEVEN LOGIC ---

var float sl_price = na

var float tp_price = na

var float entry_risk = na

var bool is_breakeven = false

if (long_condition or short_condition) and strategy.position_size == 0

last_traded_cross_idx := long_condition ? last_cross_long_idx : last_cross_short_idx

sl_price := long_condition ? lower_bb : upper_bb

entry_risk := math.abs(close - sl_price)

tp_price := long_condition ? close + (entry_risk * rr_ratio) : close - (entry_risk * rr_ratio)

is_breakeven := false

if strategy.position_size != 0 and use_breakeven and not is_breakeven

if strategy.position_size > 0 and (high - strategy.position_avg_price) / entry_risk >= be_activation

sl_price := strategy.position_avg_price

is_breakeven := true

else if strategy.position_size < 0 and (strategy.position_avg_price - low) / entry_risk >= be_activation

sl_price := strategy.position_avg_price

is_breakeven := true

// --- 5. EXECUTION ---

if (long_condition)

strategy.entry("Long", strategy.long)

if (short_condition)

strategy.entry("Short", strategy.short)

if strategy.position_size != 0

strategy.exit("Exit", stop=sl_price, limit=tp_price,

comment_loss=is_breakeven ? "BE Hit" : "SL Hit",

comment_profit="TP Hit")

// --- 6. VISUALS ---

plot(strategy.position_size != 0 ? sl_price : na, "Stop Level", color=is_breakeven ? color.yellow : color.red, style=plot.style_linebr, linewidth=2)

plot(strategy.position_size != 0 ? tp_price : na, "Target Level", color=color.green, style=plot.style_linebr, linewidth=2)

bgcolor(use_overext_filt and is_overextended ? color.new(color.purple, 90) : na)