Session Liquidity Sweep + Trend Confirmation

ลิงก์ TradingView

คำอธิบาย

This strategy aims to capture high-probability intraday trades by combining liquidity sweeps with a trend confirmation filter. It is designed for traders who want a systematic approach to trade breakouts during specific market sessions while controlling risk with ATR-based stops.

How it Works:

Session Filter: Trades are only considered during a defined session (default 9:30 - 11:00). This helps avoid low-volume periods that can lead to false signals.

Trend Confirmation: The strategy uses a 50-period EMA to identify the market trend. Long trades are only taken in an uptrend, and short trades in a downtrend.

Liquidity Sweep Detection:

A long entry occurs when price dips below the prior N-bar low but closes back above it, indicating a potential liquidity sweep that stops being triggered before the trend continues upward.

A short entry occurs when price spikes above the prior N-bar high but closes below it, signaling a potential sweep of stops before the downward trend resumes.

ATR-Based Risk Management:

Stop loss is calculated using the Average True Range (ATR) multiplied by a configurable factor (default 1.5).

Take profit is set based on a risk-reward ratio (default 2.5x).

Position Sizing: Default position size is 5% of equity per trade, making it suitable for risk-conscious trading.

Inputs:

Session Start/End (HHMM)

Liquidity Lookback Period (number of bars to define prior high/low)

ATR Length for stop calculation

ATR Stop Multiplier

Risk-Reward Ratio

EMA Trend Filter Length

Visuals:

Prior Liquidity High (red)

Prior Liquidity Low (green)

EMA Trend (blue)

Why Use This Strategy:

Captures stop-hunt moves often triggered by larger market participants.

Only trades with trend confirmation, reducing false signals.

Provides automatic ATR-based stop loss and take profit for consistent risk management.

Easy to adjust session time, ATR, EMA length, and risk-reward to suit your trading style.

Important Notes:

Assumes 0.05% commission and 1-pip slippage. Adjust according to your broker.

Not financial advice; intended for educational, backtesting, or paper trading purposes.

Always test strategies thoroughly before applying to live accounts.

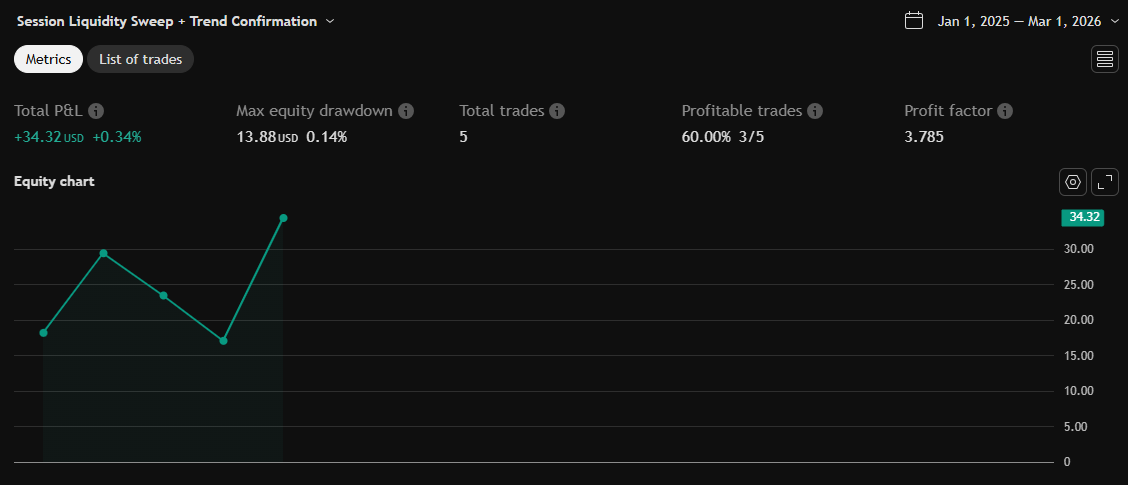

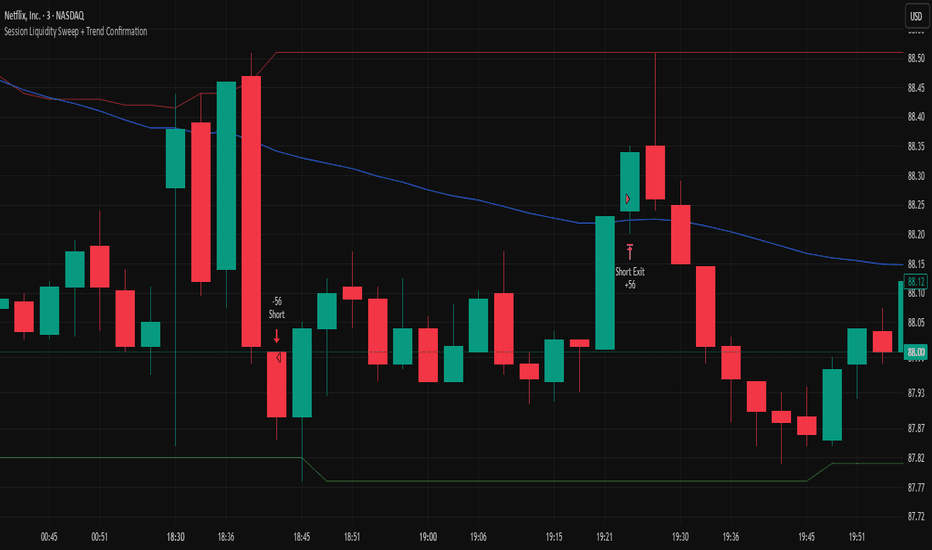

รูป Preview

Pine Script Source

// This Pine Script® code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © AIScripts

//@version=6

strategy(

"Session Liquidity Sweep + Trend Confirmation",

overlay=true,

initial_capital=100000,

default_qty_type=strategy.percent_of_equity,

default_qty_value=5,

commission_type=strategy.commission.percent,

commission_value=0.05,

slippage=1

)

// ─────────────────────

// INPUTS

// ─────────────────────

sessionStart = input.int(930, "Session Start (HHMM)")

sessionEnd = input.int(1100, "Session End (HHMM)")

lookbackBars = input.int(20, "Liquidity Lookback")

atrLen = input.int(14, "ATR Length")

slMult = input.float(1.5, "Stop ATR Multiplier")

rr = input.float(2.5, "Risk-Reward")

emaTrendLen = input.int(50, "EMA Trend Filter")

// ─────────────────────

// SESSION FILTER

// ─────────────────────

hourMinute = hour * 100 + minute

inSession = (hourMinute >= sessionStart) and (hourMinute <= sessionEnd)

// ─────────────────────

// TREND FILTER

// ─────────────────────

emaTrend = ta.ema(close, emaTrendLen)

trendUp = close > emaTrend

trendDown = close < emaTrend

// ─────────────────────

// LIQUIDITY LEVELS

// ─────────────────────

prevHigh = ta.highest(high[1], lookbackBars)

prevLow = ta.lowest(low[1], lookbackBars)

// ─────────────────────

// SWEEP + CONFIRMATION

// ─────────────────────

sweepHigh = (high > prevHigh) and (close < prevHigh)

sweepLow = (low < prevLow) and (close > prevLow)

// ─────────────────────

// ATR FOR RISK

// ─────────────────────

atrVal = ta.atr(atrLen)

// ─────────────────────

// ENTRY CONDITIONS

// ─────────────────────

longCond = inSession and sweepLow and trendUp and (close > open) and (strategy.position_size == 0)

shortCond = inSession and sweepHigh and trendDown and (close < open) and (strategy.position_size == 0)

if longCond

strategy.entry("Long", strategy.long)

if shortCond

strategy.entry("Short", strategy.short)

// ─────────────────────

// RISK MANAGEMENT

// ─────────────────────

longStop = strategy.position_avg_price - atrVal * slMult

longLimit = strategy.position_avg_price + atrVal * slMult * rr

shortStop = strategy.position_avg_price + atrVal * slMult

shortLimit = strategy.position_avg_price - atrVal * slMult * rr

strategy.exit("Long Exit", "Long", stop=longStop, limit=longLimit)

strategy.exit("Short Exit", "Short", stop=shortStop, limit=shortLimit)

// ─────────────────────

// VISUALS

// ─────────────────────

plot(prevHigh, "Prior Liquidity High", color=color.new(color.red, 40))

plot(prevLow, "Prior Liquidity Low", color=color.new(color.green, 40))

plot(emaTrend, "EMA Trend", color=color.new(color.blue, 0))