NQ Scalper (EMA Trend + Pullback Reclaim) [v5]

ลิงก์ TradingView

คำอธิบาย

NQ Scalper (EMA Trend + Pullback Reclaim) is a fast intraday strategy built for 1–5 minute charts. It trades pullbacks in the direction of trend using a 100 EMA trend filter and a fast EMA reclaim trigger. RSI confirmation helps filter weak setups, and an optional VWAP filter can further align entries with intraday bias.

The strategy uses ATR-based stop loss and take profit, with an optional trailing stop. Designed primarily for NQ/MNQ scalping during regular market hours. Best used for backtesting, optimization, and forward testing with proper risk management.

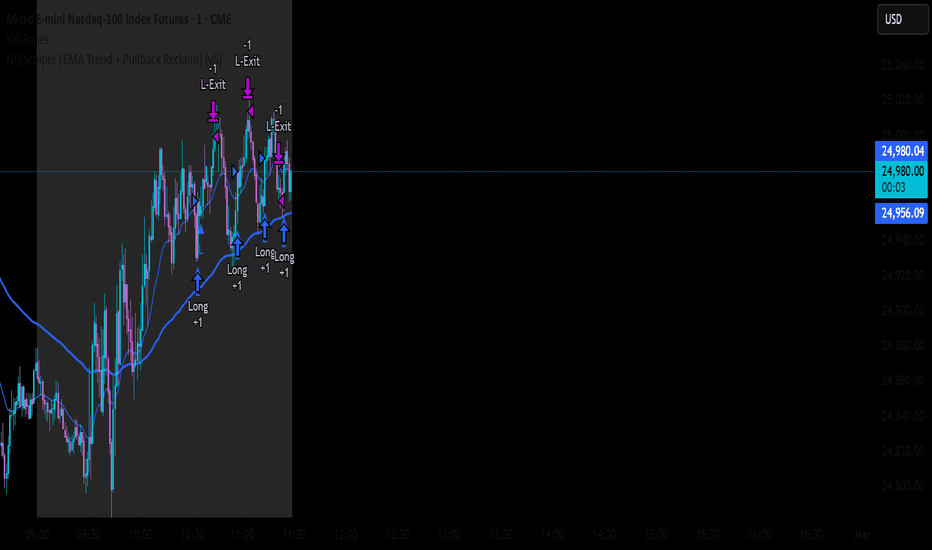

รูป Preview

Pine Script Source

//@version=5

strategy("NQ Scalper (EMA Trend + Pullback Reclaim) [v5]",

overlay=true,

calc_on_every_tick=true,

process_orders_on_close=true,

initial_capital=10000,

commission_type=strategy.commission.cash_per_contract,

commission_value=0.5)

// ─────────────────────────────────────────────────────────────────────────────

// Inputs

// ─────────────────────────────────────────────────────────────────────────────

groupTrend = "Trend / Signals"

emaTrendLen = input.int(100, "Trend EMA Length", minval=1, group=groupTrend)

emaFastLen = input.int(21, "Fast EMA Length", minval=1, group=groupTrend)

rsiLen = input.int(14, "RSI Length", minval=1, group=groupTrend)

rsiLongMin = input.int(52, "RSI Min for Long", minval=1, maxval=99, group=groupTrend)

rsiShortMax = input.int(48, "RSI Max for Short", minval=1, maxval=99, group=groupTrend)

useVWAP = input.bool(false, "Use VWAP filter (optional)", group=groupTrend)

groupRisk = "Risk / Exits"

atrLen = input.int(14, "ATR Length", minval=1, group=groupRisk)

stopATR = input.float(1.2, "Stop = ATR x", minval=0.1, step=0.1, group=groupRisk)

targetATR = input.float(1.6, "Target = ATR x", minval=0.1, step=0.1, group=groupRisk)

useTrail = input.bool(false, "Use Trailing Stop", group=groupRisk)

trailATR = input.float(1.0, "Trail = ATR x", minval=0.1, step=0.1, group=groupRisk)

groupSession = "Session Filter"

useSession = input.bool(true, "Trade only in session", group=groupSession)

sessionInput = input.session("0930-1600", "Session (exchange time)", group=groupSession)

// Position sizing (simple)

groupSize = "Position Sizing"

qtyContracts = input.int(1, "Contracts", minval=1, group=groupSize)

// ─────────────────────────────────────────────────────────────────────────────

// Indicators

// ─────────────────────────────────────────────────────────────────────────────

emaTrend = ta.ema(close, emaTrendLen)

emaFast = ta.ema(close, emaFastLen)

rsiVal = ta.rsi(close, rsiLen)

atrVal = ta.atr(atrLen)

vwapVal = ta.vwap(hlc3)

// Session logic

inSession = not na(time(timeframe.period, sessionInput))

allowTrade = useSession ? inSession : true

// ─────────────────────────────────────────────────────────────────────────────

// Signal Logic (Pullback + Reclaim)

// Long idea:

// 1) Overall trend bullish: close > EMA trend

// 2) Price pulls back under fast EMA, then reclaims it (cross up)

// 3) RSI confirms strength

// Short idea is inverse.

// ─────────────────────────────────────────────────────────────────────────────

trendLong = close > emaTrend

trendShort = close < emaTrend

vwapLongOk = useVWAP ? close >= vwapVal : true

vwapShortOk = useVWAP ? close <= vwapVal : true

pullbackLong = close[1] < emaFast[1] and ta.crossover(close, emaFast)

pullbackShort = close[1] > emaFast[1] and ta.crossunder(close, emaFast)

rsiLongOk = rsiVal >= rsiLongMin

rsiShortOk = rsiVal <= rsiShortMax

longSignal = allowTrade and trendLong and pullbackLong and rsiLongOk and vwapLongOk

shortSignal = allowTrade and trendShort and pullbackShort and rsiShortOk and vwapShortOk

// ─────────────────────────────────────────────────────────────────────────────

// Entries

// ─────────────────────────────────────────────────────────────────────────────

if (longSignal) and strategy.position_size <= 0

strategy.entry("Long", strategy.long, qty=qtyContracts)

if (shortSignal) and strategy.position_size >= 0

strategy.entry("Short", strategy.short, qty=qtyContracts)

// ─────────────────────────────────────────────────────────────────────────────

// Exits (ATR-based)

// ─────────────────────────────────────────────────────────────────────────────

longStop = strategy.position_avg_price - atrVal * stopATR

longTarget = strategy.position_avg_price + atrVal * targetATR

shortStop = strategy.position_avg_price + atrVal * stopATR

shortTarget = strategy.position_avg_price - atrVal * targetATR

// Optional trailing stop

trailPts = atrVal * trailATR

if strategy.position_size > 0

if useTrail

strategy.exit("L-Exit", from_entry="Long", limit=longTarget, trail_points=trailPts)

else

strategy.exit("L-Exit", from_entry="Long", stop=longStop, limit=longTarget)

if strategy.position_size < 0

if useTrail

strategy.exit("S-Exit", from_entry="Short", limit=shortTarget, trail_points=trailPts)

else

strategy.exit("S-Exit", from_entry="Short", stop=shortStop, limit=shortTarget)

// ─────────────────────────────────────────────────────────────────────────────

// Visuals

// ─────────────────────────────────────────────────────────────────────────────

plot(emaTrend, "EMA Trend", linewidth=2)

plot(emaFast, "EMA Fast", linewidth=1)

plot(useVWAP ? vwapVal : na, "VWAP", linewidth=1)

plotshape(longSignal, title="Long Signal", style=shape.triangleup, location=location.belowbar, size=size.tiny, text="L")

plotshape(shortSignal, title="Short Signal", style=shape.triangledown, location=location.abovebar, size=size.tiny, text="S")