Simple RSI Strategy - Rule Based Higher Timeframe Trading

ลิงก์ TradingView

คำอธิบาย

HOW IT WORKS

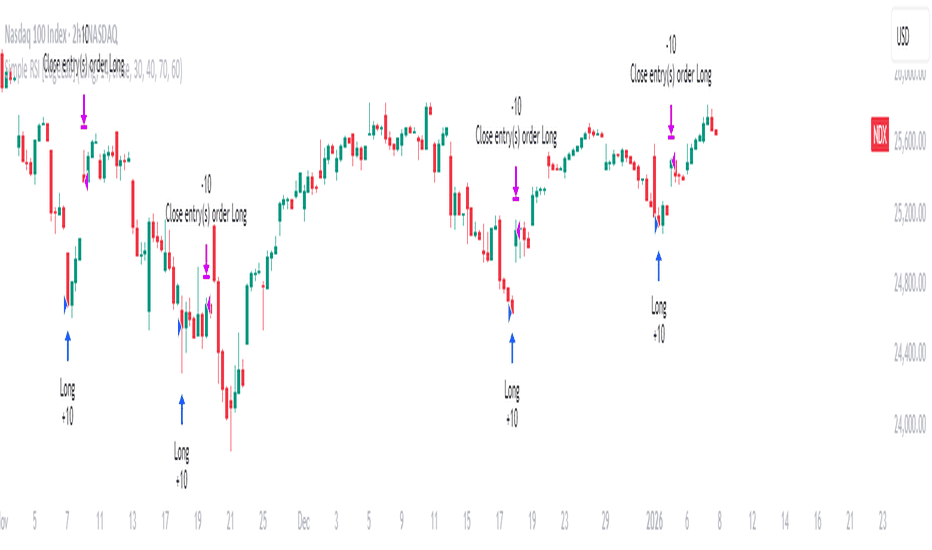

With the default settings, the strategy buys when RSI reaches 30 and closes when RSI reaches 40 .

That’s it.

A simple, rule-based mean reversion strategy designed for higher timeframes , where market noise is lower and trading becomes easier to manage.

Core logic:

Long when RSI moves into oversold territory

Exit when RSI mean-reverts upward

Optional short trades from overbought levels

One position at a time (no pyramiding)

No filters.

No discretion.

Just clear, testable rules.

MARKETS & TIMEFRAMES

This strategy is intended for:

Indices (Nasdaq, S&P 500, DAX, etc.)

Liquid futures and CFDs

Higher timeframes: 2H, 4H and Daily

The published example is Nasdaq (NDX) on the 2-hour timeframe .

Higher timeframes are strongly recommended.

HOW TO USE IT

Apply the strategy on a higher timeframe

Adjust RSI levels per market if needed

Use TradingView alerts to avoid constant screen-watching

Focus on execution, risk control, and consistency

This strategy is meant to be a building block , not a complete trading business on its own.

For long-term consistency, it works best when combined with other uncorrelated, rule-based systems.

IMPORTANT

This is not financial advice

All results are historical and not indicative of future performance

Always forward-test and apply proper risk management

For additional notes, setups and related systems, visit my TradingView profile page .

รูป Preview

Pine Script Source

//@version=6

strategy(

"Simple RSI [EdgeLab]",

overlay = true,

initial_capital = 100000,

default_qty_type = strategy.percent_of_equity,

default_qty_value = 100,

pyramiding = 0,

process_orders_on_close = true,

margin_long = 0,

margin_short = 0)

//────────────────────

// Inputs (tooltips show as the little "i" icon)

//────────────────────

dir = input.string(

"Long",

"Trade Direction",

options = ["Long", "Short", "Both"],

tooltip = "Choose which trades the strategy is allowed to take:\n• Long = buy signals only\n• Short = sell signals only\n• Both = long and short signals",

group = "General")

len = input.int(

14,

"RSI Length",

minval = 1,

tooltip = "How many bars the RSI calculation uses.\nHigher = smoother/slower signals.\nLower = faster/more signals.",

group = "General")

src = input.source(

close,

"RSI Source",

tooltip = "Which price the RSI is calculated from.\nClose is the most common choice.",

group = "General")

// Long levels

entryL = input.int(

30,

"Long: Enter when RSI ≤",

minval = 1,

maxval = 99,

tooltip = "Long entry trigger.\nWhen RSI drops to this level or lower, the strategy opens a LONG.\nLower value = fewer entries (more 'oversold').",

group = "Long")

exitL = input.int(

40,

"Long: Exit when RSI ≥",

minval = 2,

maxval = 100,

tooltip = "Long exit trigger.\nWhen RSI rises to this level or higher, the strategy closes the LONG.\nHigher value = holds longer before exiting.",

group = "Long")

// Short levels

entryS = input.int(

70,

"Short: Enter when RSI ≥",

minval = 1,

maxval = 99,

tooltip = "Short entry trigger.\nWhen RSI rises to this level or higher, the strategy opens a SHORT.\nHigher value = fewer entries (more 'overbought').",

group = "Short")

exitS = input.int(

60,

"Short: Exit when RSI ≤",

minval = 1,

maxval = 99,

tooltip = "Short exit trigger.\nWhen RSI drops to this level or lower, the strategy closes the SHORT.\nLower value = holds longer before exiting.",

group = "Short")

// Direction flags

allowLong = dir == "Long" or dir == "Both"

allowShort = dir == "Short" or dir == "Both"

//────────────────────

// RSI

//────────────────────

r = ta.rsi(src, len)

//────────────────────

// Entry / exit conditions (enter only on first cross of level)

//────────────────────

// Long

enterLong = allowLong and ta.crossunder(r, entryL) and strategy.position_size == 0

exitLong = allowLong and ta.crossover(r, exitL) and strategy.position_size > 0

// Short

enterShort = allowShort and ta.crossover(r, entryS) and strategy.position_size == 0

exitShort = allowShort and ta.crossunder(r, exitS) and strategy.position_size < 0

//────────────────────

// Orders

//────────────────────

if enterLong

strategy.entry("Long", strategy.long)

if exitLong

strategy.close("Long")

if enterShort

strategy.entry("Short", strategy.short)

if exitShort

strategy.close("Short")

//────────────────────

// Alertconditions (for "Create Alert" dialog)

//────────────────────

alertcondition(enterLong, "Enter Long", "Enter LONG: RSI crossed down into the long entry level.")

alertcondition(exitLong, "Exit Long", "Exit LONG: RSI crossed up into the long exit level.")

alertcondition(enterShort, "Enter Short", "Enter SHORT: RSI crossed up into the short entry level.")

alertcondition(exitShort, "Exit Short", "Exit SHORT: RSI crossed down into the short exit level.")