Butterworth LPF Flip + AutoTune (PF)

ลิงก์ TradingView

คำอธิบาย

Butterworth LPF Flip + AutoTune (PF)

This strategy trades price trend flips using two Butterworth low-pass filters (a FAST filter and a SLOW filter). A trade is taken when the FAST filter crosses the SLOW filter. Optionally, the script can auto-tune the filter lengths by simulating many Fast/Slow combinations and selecting the pair with the best Profit Factor (PF).

What the Script Does

- Computes two 2‑pole Butterworth low‑pass filters on price.

- Enters LONG when FAST crosses above SLOW.

- Enters SHORT when FAST crosses below SLOW.

- Optionally simulates many Fast/Slow length combinations internally.

- Chooses the Fast/Slow pair with the highest Profit Factor.

- Trades only the selected best pair.

Manual Mode (Default)

1. Leave Auto‑Tune OFF.

2. Set:

- FAST cutoff period (bars)

- SLOW cutoff period (bars)

3. The strategy will trade using only these values.

Use this mode for normal trading or live deployment.

Auto‑Tune Mode

1. Enable Auto‑Tune.

2. Define Fast and Slow ranges:

- FAST min / max / step

- SLOW min / max / step

3. The script simulates ALL Fast × Slow combinations bar‑by‑bar.

4. Each combination tracks:

- Gross Profit

- Gross Loss

- Closed trades

- Profit Factor (PF = GP / GL)

5. At the end of the chart, the best PF pair is selected and used for trading.

Interpreting the End Box

The status label at the end of the chart reports:

- Whether Auto‑Tune is enabled

- Number of candidate pairs tested

- Best FAST period

- Best SLOW period

- Profit Factor of the best pair

- Win Rate (wins ÷ closed trades)

If PF is near 1.0 or trades are very low, expand the range or length of the test.

Best Practices

- Use Auto‑Tune ONLY for research and optimization.

- After finding good parameters, disable Auto‑Tune and trade manually.

- Keep Fast < Slow (logical separation).

- Longer charts produce more reliable PF results.

- Avoid very small step sizes (performance + noise).

Known Limitations

- Pine Script runs bar‑by‑bar; tuning is approximate, not vectorized.

- Large grids increase execution time.

- Results are historical and NOT predictive.

- Not suitable for live auto‑optimization.

Summary

This script is best viewed as a *research tool first, strategy second*. Use it to discover stable Fast/Slow regimes, then lock them in for simple, repeatable trading.

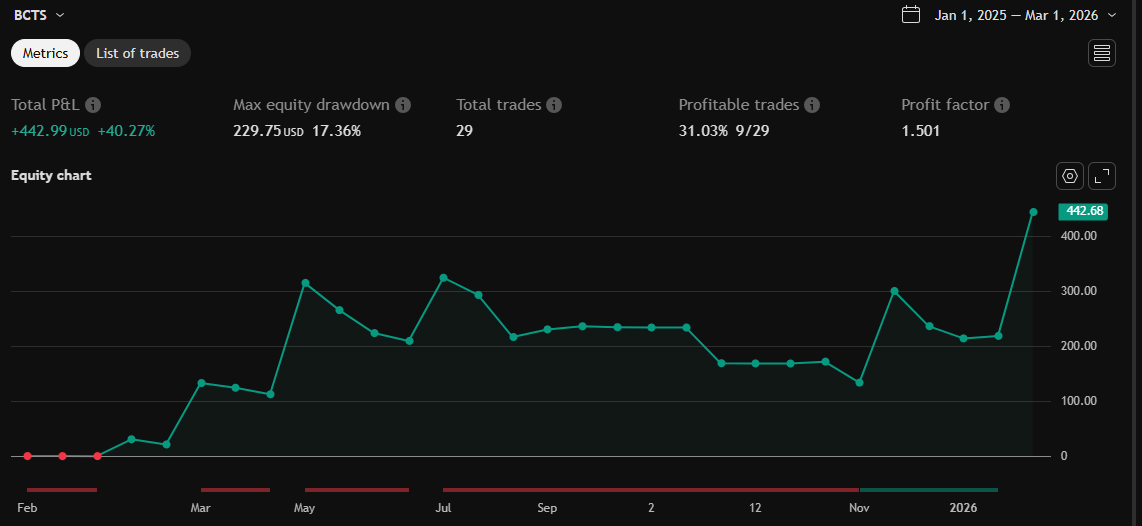

รูป Preview

Pine Script Source

//@version=6

strategy("BCTS", "BCTS", overlay = true,

initial_capital = 100000, pyramiding = 0,

commission_type = strategy.commission.percent, commission_value = 0.0,

max_bars_back = 5000)

//────────────────────────────────────────────────────────────────────

// Inputs

//────────────────────────────────────────────────────────────────────

BW_src = input.source(close, "Source")

BW_showFast = input.bool(true, "Show FAST LPF")

BW_showSlow = input.bool(true, "Show SLOW LPF")

BW_fastPerManual = input.int(250, "FAST cutoff period (manual, bars)", minval = 2)

BW_slowPerManual = input.int(1000, "SLOW cutoff period (manual, bars)", minval = 2)

BW_useLongs = input.bool(true, "Enable Longs")

BW_useShorts = input.bool(true, "Enable Shorts")

grpAT = "AutoTune"

BW_autoTune = input.bool(false, "Auto-tune Fast/Slow on Profit Factor (internal sim)", group=grpAT)

BW_fastMinIn = input.int(250, "FAST min", minval=2, group=grpAT)

BW_fastMaxIn = input.int(1000, "FAST max", minval=2, group=grpAT)

BW_fastStepIn = input.int(50, "FAST step", minval=1, group=grpAT)

BW_slowMinIn = input.int(1000, "SLOW min", minval=2, group=grpAT)

BW_slowMaxIn = input.int(2000, "SLOW max", minval=2, group=grpAT)

BW_slowStepIn = input.int(50, "SLOW step", minval=1, group=grpAT)

BW_minTrades = input.int(25, "Min CLOSED sim trades to qualify", minval=0, group=grpAT)

//────────────────────────────────────────────────────────────────────

// Butterworth helpers (2-pole)

//────────────────────────────────────────────────────────────────────

BW_coeffs(int _periodInt) =>

float p = float(_periodInt)

float om = math.tan(math.pi / p)

float n = 1.0 / (1.0 + math.sqrt(2.0) * om + om * om)

float b0 = (om * om) * n

float b1 = 2.0 * b0

float b2 = b0

float a1 = 2.0 * (om * om - 1.0) * n

float a2 = (1.0 - math.sqrt(2.0) * om + om * om) * n

[b0, b1, b2, a1, a2]

BW_butter2pole_single(float _x, int _periodInt) =>

[b0, b1, b2, a1, a2] = BW_coeffs(_periodInt)

var float y = na

y := b0 * _x +

b1 * nz(_x[1], _x) +

b2 * nz(_x[2], _x) -

a1 * nz(y[1], _x) -

a2 * nz(y[2], _x)

y

//────────────────────────────────────────────────────────────────────

// AutoTune state

//────────────────────────────────────────────────────────────────────

var bool BW_built = false

var array<int> BW_fastList = array.new_int()

var array<int> BW_slowList = array.new_int()

var array<float> BW_f_b0 = array.new_float()

var array<float> BW_f_b1 = array.new_float()

var array<float> BW_f_b2 = array.new_float()

var array<float> BW_f_a1 = array.new_float()

var array<float> BW_f_a2 = array.new_float()

var array<float> BW_s_b0 = array.new_float()

var array<float> BW_s_b1 = array.new_float()

var array<float> BW_s_b2 = array.new_float()

var array<float> BW_s_a1 = array.new_float()

var array<float> BW_s_a2 = array.new_float()

var array<float> BW_f_y1 = array.new_float()

var array<float> BW_f_y2 = array.new_float()

var array<float> BW_s_y1 = array.new_float()

var array<float> BW_s_y2 = array.new_float()

var array<float> BW_f_prev = array.new_float()

var array<float> BW_s_prev = array.new_float()

var array<int> BW_pos = array.new_int()

var array<float> BW_entry = array.new_float()

var array<float> BW_gp = array.new_float()

var array<float> BW_gl = array.new_float()

var array<int> BW_tr = array.new_int()

var int BW_bestFast = na

var int BW_bestSlow = na

var float BW_bestPF = na

var int BW_bestTR = na

// Track last inputs (NO na on bool)

var bool BW_hasLast = false

var bool BW_lastAutoTune = false

var int BW_lastFastMin = 0

var int BW_lastFastMax = 0

var int BW_lastFastStep = 0

var int BW_lastSlowMin = 0

var int BW_lastSlowMax = 0

var int BW_lastSlowStep = 0

var int BW_lastMinTrades = 0

// sanitize ranges

int BW_fastMin = math.min(BW_fastMinIn, BW_fastMaxIn)

int BW_fastMax = math.max(BW_fastMinIn, BW_fastMaxIn)

int BW_fastStep = math.max(BW_fastStepIn, 1)

int BW_slowMin = math.min(BW_slowMinIn, BW_slowMaxIn)

int BW_slowMax = math.max(BW_slowMinIn, BW_slowMaxIn)

int BW_slowStep = math.max(BW_slowStepIn, 1)

bool BW_paramsChanged =

not BW_hasLast or

BW_lastAutoTune != BW_autoTune or

BW_lastFastMin != BW_fastMin or

BW_lastFastMax != BW_fastMax or

BW_lastFastStep != BW_fastStep or

BW_lastSlowMin != BW_slowMin or

BW_lastSlowMax != BW_slowMax or

BW_lastSlowStep != BW_slowStep or

BW_lastMinTrades != BW_minTrades

bool BW_needBuild =

BW_autoTune and (

BW_paramsChanged or

not BW_built or

array.size(BW_f_b0) == 0 or

array.size(BW_s_b0) == 0

)

//────────────────────────────────────────────────────────────────────

// BUILD candidates

//────────────────────────────────────────────────────────────────────

if BW_needBuild

BW_lastAutoTune := BW_autoTune

BW_lastFastMin := BW_fastMin

BW_lastFastMax := BW_fastMax

BW_lastFastStep := BW_fastStep

BW_lastSlowMin := BW_slowMin

BW_lastSlowMax := BW_slowMax

BW_lastSlowStep := BW_slowStep

BW_lastMinTrades := BW_minTrades

BW_hasLast := true

BW_bestFast := na

BW_bestSlow := na

BW_bestPF := na

BW_bestTR := na

array.clear(BW_fastList)

array.clear(BW_slowList)

int f = BW_fastMin

while f <= BW_fastMax

array.push(BW_fastList, f)

f += BW_fastStep

int s = BW_slowMin

while s <= BW_slowMax

array.push(BW_slowList, s)

s += BW_slowStep

int nFast = array.size(BW_fastList)

int nSlow = array.size(BW_slowList)

int nCand = nFast * nSlow

// reset arrays with deterministic size

BW_f_b0 := array.new_float(nCand, 0.0)

BW_f_b1 := array.new_float(nCand, 0.0)

BW_f_b2 := array.new_float(nCand, 0.0)

BW_f_a1 := array.new_float(nCand, 0.0)

BW_f_a2 := array.new_float(nCand, 0.0)

BW_s_b0 := array.new_float(nCand, 0.0)

BW_s_b1 := array.new_float(nCand, 0.0)

BW_s_b2 := array.new_float(nCand, 0.0)

BW_s_a1 := array.new_float(nCand, 0.0)

BW_s_a2 := array.new_float(nCand, 0.0)

float seed = nz(BW_src, close)

BW_f_y1 := array.new_float(nCand, seed)

BW_f_y2 := array.new_float(nCand, seed)

BW_s_y1 := array.new_float(nCand, seed)

BW_s_y2 := array.new_float(nCand, seed)

BW_f_prev := array.new_float(nCand, seed)

BW_s_prev := array.new_float(nCand, seed)

BW_pos := array.new_int(nCand, 0)

BW_entry := array.new_float(nCand, na)

BW_gp := array.new_float(nCand, 0.0)

BW_gl := array.new_float(nCand, 0.0)

BW_tr := array.new_int(nCand, 0)

// fill coeffs by index

if nCand > 0

int iF = 0

while iF < nFast

int fastP = array.get(BW_fastList, iF)

[fb0, fb1, fb2, fa1, fa2] = BW_coeffs(fastP)

int iS = 0

while iS < nSlow

int slowP = array.get(BW_slowList, iS)

[sb0, sb1, sb2, sa1, sa2] = BW_coeffs(slowP)

int k = iF * nSlow + iS

array.set(BW_f_b0, k, fb0), array.set(BW_f_b1, k, fb1), array.set(BW_f_b2, k, fb2), array.set(BW_f_a1, k, fa1), array.set(BW_f_a2, k, fa2)

array.set(BW_s_b0, k, sb0), array.set(BW_s_b1, k, sb1), array.set(BW_s_b2, k, sb2), array.set(BW_s_a1, k, sa1), array.set(BW_s_a2, k, sa2)

iS += 1

iF += 1

BW_built := (nCand > 0 and array.size(BW_tr) == nCand)

// if autotune off

if not BW_autoTune

BW_built := false

//────────────────────────────────────────────────────────────────────

// Per-bar simulation update

//────────────────────────────────────────────────────────────────────

int BW_nCand = array.size(BW_tr)

int BW_nSlow = array.size(BW_slowList)

bool BW_ready = BW_autoTune and BW_built and BW_nCand > 0 and BW_nSlow > 0

if BW_ready and bar_index >= 2

float x = nz(BW_src, close)

float x1 = nz(BW_src[1], x)

float x2 = nz(BW_src[2], x)

int k = 0

while k < BW_nCand

float fb0 = array.get(BW_f_b0, k), fb1 = array.get(BW_f_b1, k), fb2 = array.get(BW_f_b2, k), fa1 = array.get(BW_f_a1, k), fa2 = array.get(BW_f_a2, k)

float sb0 = array.get(BW_s_b0, k), sb1 = array.get(BW_s_b1, k), sb2 = array.get(BW_s_b2, k), sa1 = array.get(BW_s_a1, k), sa2 = array.get(BW_s_a2, k)

float fy1 = array.get(BW_f_y1, k), fy2 = array.get(BW_f_y2, k)

float sy1 = array.get(BW_s_y1, k), sy2 = array.get(BW_s_y2, k)

float fNew = fb0*x + fb1*x1 + fb2*x2 - fa1*fy1 - fa2*fy2

float sNew = sb0*x + sb1*x1 + sb2*x2 - sa1*sy1 - sa2*sy2

array.set(BW_f_y2, k, fy1), array.set(BW_f_y1, k, fNew)

array.set(BW_s_y2, k, sy1), array.set(BW_s_y1, k, sNew)

float fPrev = array.get(BW_f_prev, k)

float sPrev = array.get(BW_s_prev, k)

bool crossUp = (fPrev <= sPrev) and (fNew > sNew)

bool crossDn = (fPrev >= sPrev) and (fNew < sNew)

array.set(BW_f_prev, k, fNew)

array.set(BW_s_prev, k, sNew)

int pos = array.get(BW_pos, k)

float entry = array.get(BW_entry, k)

float gp = array.get(BW_gp, k)

float gl = array.get(BW_gl, k)

int tr = array.get(BW_tr, k)

// CROSS UP: close old pos (if any), then open long

if crossUp

if pos != 0 and not na(entry)

float pnl = pos == 1 ? (close - entry) : (entry - close)

tr += 1

if pnl > 0

gp += pnl

else

gl += -pnl

pos := 1

entry := close

// CROSS DN: close old pos (if any), then open short

if crossDn

if pos != 0 and not na(entry)

float pnl = pos == 1 ? (close - entry) : (entry - close)

tr += 1

if pnl > 0

gp += pnl

else

gl += -pnl

pos := -1

entry := close

array.set(BW_pos, k, pos)

array.set(BW_entry, k, entry)

array.set(BW_gp, k, gp)

array.set(BW_gl, k, gl)

array.set(BW_tr, k, tr)

k += 1

// Force-close all simulated open positions on the last bar

if BW_ready and barstate.islastconfirmedhistory

int k2 = 0

while k2 < BW_nCand

int pos2 = array.get(BW_pos, k2)

float entry2 = array.get(BW_entry, k2)

float gp2 = array.get(BW_gp, k2)

float gl2 = array.get(BW_gl, k2)

int tr2 = array.get(BW_tr, k2)

if pos2 != 0 and not na(entry2)

float pnl2 = pos2 == 1 ? (close - entry2) : (entry2 - close)

tr2 += 1

if pnl2 > 0

gp2 += pnl2

else

gl2 += -pnl2

array.set(BW_pos, k2, 0)

array.set(BW_entry, k2, na)

array.set(BW_gp, k2, gp2)

array.set(BW_gl, k2, gl2)

array.set(BW_tr, k2, tr2)

k2 += 1

// Pick best PF at end

if BW_ready and barstate.islastconfirmedhistory

float bestPF = -1.0

int bestK = na

int k3 = 0

while k3 < BW_nCand

float gp = array.get(BW_gp, k3)

float gl = array.get(BW_gl, k3)

int tr = array.get(BW_tr, k3)

float pf = gl > 0 ? gp / gl : (gp > 0 ? 999999.0 : 0.0)

if tr >= BW_minTrades and pf > bestPF

bestPF := pf

bestK := k3

k3 += 1

if not na(bestK)

int bestFastIdx = int(math.floor(bestK / BW_nSlow))

int bestSlowIdx = bestK - bestFastIdx * BW_nSlow

if bestFastIdx >= 0 and bestFastIdx < array.size(BW_fastList) and bestSlowIdx >= 0 and bestSlowIdx < array.size(BW_slowList)

BW_bestFast := array.get(BW_fastList, bestFastIdx)

BW_bestSlow := array.get(BW_slowList, bestSlowIdx)

BW_bestPF := bestPF

BW_bestTR := array.get(BW_tr, bestK)

//────────────────────────────────────────────────────────────────────

// Choose periods to trade/plot

//────────────────────────────────────────────────────────────────────

int BW_fastPer = (BW_autoTune and not na(BW_bestFast)) ? BW_bestFast : BW_fastPerManual

int BW_slowPer = (BW_autoTune and not na(BW_bestSlow)) ? BW_bestSlow : BW_slowPerManual

float BW_fast = BW_butter2pole_single(BW_src, BW_fastPer)

float BW_slow = BW_butter2pole_single(BW_src, BW_slowPer)

// Flip strategy

bool BW_longSig = ta.crossover(BW_fast, BW_slow)

bool BW_shortSig = ta.crossunder(BW_fast, BW_slow)

if BW_longSig

if BW_useShorts

strategy.close("S")

if BW_useLongs

strategy.entry("L", strategy.long)

if BW_shortSig

if BW_useLongs

strategy.close("L")

if BW_useShorts

strategy.entry("S", strategy.short)

//────────────────────────────────────────────────────────────────────

// Plots + status box

//────────────────────────────────────────────────────────────────────

plot(BW_src, "Source", color = color.new(color.gray, 70))

plot(BW_showFast ? BW_fast : na, "FAST Butterworth LPF", color = color.new(color.aqua, 0), linewidth = 2)

plot(BW_showSlow ? BW_slow : na, "SLOW Butterworth LPF", color = color.new(color.orange, 0), linewidth = 2)

var label BW_lbl = na

if barstate.islastconfirmedhistory

label.delete(BW_lbl)

string atLine =

"AT=" + (BW_autoTune ? "ON" : "OFF") +

" built=" + (BW_built ? "Y" : "N") +

" cand=" + str.tostring(BW_nCand) +

" minTR=" + str.tostring(BW_minTrades)

string bestLine =

(BW_autoTune and not na(BW_bestFast)) ?

("Best Fast=" + str.tostring(BW_bestFast) +

" Best Slow=" + str.tostring(BW_bestSlow) +

"\nPF=" + str.tostring(BW_bestPF, "#.###") +

" TR=" + str.tostring(BW_bestTR)) :

("Manual Fast=" + str.tostring(BW_fastPerManual) +

" Slow=" + str.tostring(BW_slowPerManual))

BW_lbl := label.new(bar_index, high, atLine + "\n" + bestLine,

style=label.style_label_down, textcolor=color.white, color=color.new(color.black, 0))