Double&Triple Pattern[TS_Indie]

ลิงก์ TradingView

คำอธิบาย

📌 Description – Double & Triple Pattern Indicator

The Double & Triple Pattern Indicator is developed to help traders systematically and clearly identify Double Top, Double Bottom, Triple Top, and Triple Bottom chart patterns.

⚙️ Core Logic & Working Mechanism

The Double & Triple Pattern Indicator is built on the concept of price swing formation, based on the logic of Trend Entry_0 , which focuses on structured market analysis and price action behavior.

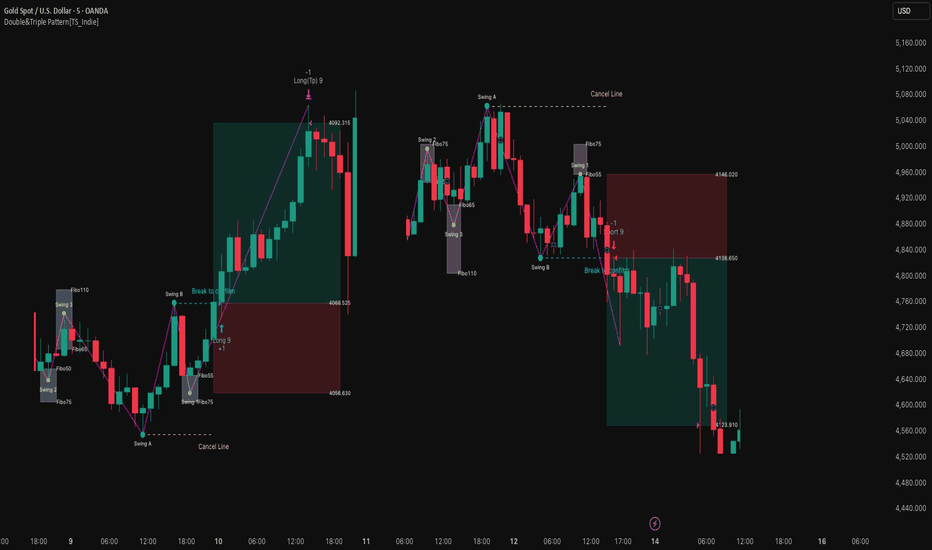

The indicator detects three main swing points (Swing 1, Swing 2, and Swing 3). A Fibonacci Box is then created using Swing A and Swing B as reference points to define the swing detection zone.

When all three swings remain inside the defined Fibonacci Box, the structure is considered a valid Price Action setup.

The indicator then plots key lines on the chart:

➩ Break Line – used to confirm the signal (confirmation)

➩ Cancel Line – used to invalidate the price action if price moves against the conditions

➛ When price breaks the Break Line , the structure is confirmed and a Pending Order is placed at Swing B , with the Stop Loss set at Swing 1.

➛ If price breaks the Cancel Line first, the price action structure is immediately invalidated.

⚙️ Fibonacci Entry Zone & Change SL Settings

➩ When Fibo Entry Zone is set to 0, the Pending Order is placed directly at Swing B.

➩ When the value is greater than 0, the Pending Order is calculated using Fibonacci levels drawn from Swing B to the Stop Loss level.

➩ Change SL allows switching the Stop Loss reference between Swing 1 and Swing A.

⚙️ Min & Max Control for Swing Size : xATR

When enabling Control Size Swing : xATR , the indicator filters Swing B based on the defined Min and Max range.

This allows traders to selectively test larger or smaller swing-based price actions , depending on their trading strategy.

⭐ Pending Order Cancellation Conditions

A Pending Order will be canceled under the following conditions:

1.A new Price Action signal appears on either the Buy or Sell side.

2.When Time Session is enabled, the Pending Order is canceled once price exits the selected session.

🕹 Order Management Rule

When there is an active open position, the indicator restricts the creation of new Pending Orders to prevent overlapping positions.

💡 Double Pattern Example

💡 Triple Pattern Example

⚠️ Disclaimer

This indicator is designed for technical analysis purposes only and does not constitute investment advice.

Users should apply proper risk management and make decisions at their own discretion.

🥂 Community Sharing

If you find parameter settings that work well or produce strong statistical results, feel free to share them with the community so we can improve and develop this indicator together.

รูป Preview

Pine Script Source

// This Pine Script® code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Truth_Strategy_Indie

//@version=6

strategy("Double&Triple Pattern[TS_Indie]" , overlay=true, max_labels_count=500 , max_lines_count = 500 ,max_boxes_count = 500, max_bars_back = 5000 , margin_long=0, margin_short=0 , initial_capital = 100000 )

Entry_Position = "====== Entry Condition ====== "

// === Input Parameters ===

rr_ratio = input.float(2, "Risk Reward Ratio", step=0.1 , inline="0.1" , group = Entry_Position )

length_atr = input.int(title="Stop loss ATR", defval=14, minval=1 , inline="0.2" , group = Entry_Position )

x_ATR = input.float( 0 , "X", step=0.1 , inline="0.2" , group = Entry_Position )

B_long = input.bool( true ,"Entry Longㅤㅤ" , inline="0.3", group = Entry_Position)

S_short = input.bool( true ,"Entry Short", inline="0.3", group = Entry_Position)

fibo_entry = input.float(0, "Fibo Entry Zone", step= 1 , inline="0.5" , group = Entry_Position )

Sl_change = input.bool(true, "Change SL" , inline="0.5" , group = Entry_Position )

stxt1 = input.string("Swing 1", "✅ [ Fibo1 ]", inline ="0.6", group = Entry_Position )

Swing1_more = input.float(55, "Min", step= 1 , inline="1" , group = Entry_Position )

Swing1_less = input.float(75, "Max", step= 1 , inline="1" , group = Entry_Position )

use_Swing2 = input.bool( true ,"[ Fibo2 ]" , inline="2", group = Entry_Position)

stxt2 = input.string("Swing 2", "", inline ="2", group = Entry_Position )

Swing2_more = input.float(50, "Min", step= 1 , inline="2.1" , group = Entry_Position )

Swing2_less = input.float(75, "Max", step= 1 , inline="2.1" , group = Entry_Position )

use_Swing3 = input.bool( true ,"[ Fibo3 ]" , inline="2.5", group = Entry_Position)

stxt3 = input.string("Swing 3", "", inline ="2.5", group = Entry_Position )

Swing3_more = input.float(65, "Min", step= 1 , inline="3" , group = Entry_Position )

Swing3_less = input.float(110, "Max", step= 1 , inline="3" , group = Entry_Position )

use_size = input.bool( false ," [ Control Size Swing : xATR]" , inline="4", group = Entry_Position)

Size_candle_more = input.float(0, "Min", step= 1 , inline="5" , group = Entry_Position )

Size_candle_less = input.float(3, "Max", step= 1 , inline="5" , group = Entry_Position )

//====== Time Filter ======

Time_Filter = "====== Time Filter ======"

s_date = input.time(timestamp("01 Jan 1970"),"Start" , inline="1" , group = Time_Filter )

en_date = input.time(timestamp("01 Jan 2500"), "End " , inline="2" , group = Time_Filter )

con_date = time >= s_date and time <= en_date

//======== session ========

_session(sess) =>

not na(time(timeframe.period, sess, "UTC+0" ))

s_New_York = input.bool( false ,"New York" , inline = "3" , group = Time_Filter )

t_New = input.session( '1300-2200', "" , inline = "3" , group = Time_Filter )

Session_1 = _session(t_New) , cf_ses1 = s_New_York ? Session_1 : false

s_London = input.bool( false ,"London" , inline = "4" , group = Time_Filter )

t_Lon = input.session( '0700-1600' , "" , inline = "4" , group = Time_Filter )

Session_2 = _session(t_Lon) , cf_ses2 = s_London ? Session_2 : false

s_Tokyo = input.bool( false ,"Tokyo" , inline = "5" , group = Time_Filter )

t_Tokyo = input.session( '0000-0900' , "" , inline = "5" , group = Time_Filter )

Session_3 = _session(t_Tokyo) , cf_ses3 = s_Tokyo ? Session_3 : false

s_Sydney = input.bool( false ,"Sydney" , inline = "6" , group = Time_Filter )

t_Syd = input.session( '2100-0600' , "" , inline = "6" , group = Time_Filter )

Session_4 = _session(t_Syd) , cf_ses4 = s_Sydney ? Session_4 : false

ses_check = s_New_York or s_London or s_Tokyo or s_Sydney

time_con = cf_ses1 or cf_ses2 or cf_ses3 or cf_ses4

con_time = ses_check ? time_con : true

//======== Table ========

position(select) =>

switch select

"bottom_right" => position.bottom_right

"bottom_center" => position.bottom_center

"bottom_left" => position.bottom_left

"top_center" => position.top_center

"top_left" => position.top_left

"top_right" => position.top_right

"mid_center" => position.middle_center

"mid_left" => position.middle_left

"mid_right" => position.middle_right

result_group = "====== Trading Result Table ======"

Show_result = input.bool( true ,"Show Result" , inline = "1" , group = result_group ,tooltip = "The Profit Factor here is calculated using the formula:\n\(Number of Wins x Risk-Reward Ratio) / Number of Losses\n\This formula is based on the assumption that the risk per losing trade is fixed — for example, every losing trade costs exactly 1% of the account.\n\Because of this assumption, the calculated Profit Factor will not match TradingView’s result, since TradingView uses:\n\Gross Profit / Gross Loss\n\And in actual TradingView trades, the loss amount of each trade is not always equal, because the system doesn’t enforce a fixed-risk rule for every losing trade. " )

select_position = input.string("bottom_right", "", options = ["bottom_right", "bottom_center", "bottom_left", "top_center", "top_left" , "top_right" , "mid_center" , "mid_left" , "mid_right" ], group = result_group , inline="1" , display = display.data_window)

Factor_up = input.float( 1.3 ,"Profit Factor > " , step=0.1 , inline = "2" , group = result_group )

Factor_up_color = input(title = " " , defval = #a5d6a7 , inline = "2" , group = result_group)

Factor_donw = input.float( 1 ,"Profit Factor < " , step=0.1 , inline = "3" , group = result_group )

Factor_donw_color = input(title = " " , defval = #faa1a4 , inline = "3" , group = result_group)

display_group = "====== Display ======"

show_line = input.bool(true,'Line', inline="1" , group = display_group)

sw_line_style = input.string('⎯⎯⎯', '' , options = ['⎯⎯⎯', '----', '····'] , inline = '1' , group = display_group)

Color_sw = input(title = " " , defval = #f700ff , inline = "1" , group = display_group)

text_line2_col = input(title = "Text" , defval = #ffffff , inline = "1.5" , group = display_group)

Color_Mark_Swing_i1 = input(#ffee58, 'Swing' , inline="1.5", group = display_group)

Color_Mark_Swing_i2 = input(#00bcd4, '/ ' , inline="1.5", group = display_group)

show_CF_fibo = input.bool(true,'Box Confirm Fibo', inline="3" , group = display_group)

Size_fibo = input.string('Small', '', options = ['Tiny', 'Small', 'Normal'] , inline="3" , group= display_group)

col_cf_con1 = input(title = "Fibo Buy" , defval = color.rgb(187, 217, 251, 70) , inline = "4" , group = display_group)

col_cf_con2 = input(title = "Fibo Sell" , defval = color.rgb(225, 190, 231, 70) , inline = "4" , group = display_group)

var In_Size_fibo = Size_fibo == 'Tiny' ? size.tiny : Size_fibo == 'Small' ? size.small : size.normal

show_CF_line = input.bool(true,'Confirm Line', inline="5" , group = display_group)

Size_CF_line = input.string('Normal', '', options = ['Small', 'Normal', 'Large'] , inline="5" , group= display_group)

var In_Size_CF_line = Size_CF_line == 'Large' ? size.large : Size_CF_line == 'Small' ? size.small : size.normal

Color_tesst_1 = input(title = "Break" , defval = #00aaff , inline = "6" , group = display_group)

Color_tesst_2 = input(title = "Cancel" , defval = #ffee58 , inline = "6" , group = display_group)

show_CF_candle = input.bool(true,'Control Size Swing', inline="7" , group = display_group)

Size_CF_candle = input.string('Small', '', options = ['Small', 'Normal', 'Large'] , inline="7" , group= display_group)

var In_Size_CF_candle = Size_CF_candle == 'Large' ? size.large : Size_CF_candle == 'Small' ? size.small : size.normal

Color_candle_txt = input(title = "Text" , defval = #000000 , inline = "8" , group = display_group)

Color_candle_1 = input(title = "Max" , defval = #00aaff , inline = "8" , group = display_group)

Color_candle_2 = input(title = "Min" , defval = #ffee58 , inline = "8" , group = display_group)

TRANSP = #ffffff00

get_line_style(style) =>

out = switch style

'⎯⎯⎯' => line.style_solid

'----' => line.style_dashed

'····' => line.style_dotted

var float big_high = na , var float big_low = na , var int Bar_big_high = 0 , var int Bar_big_low = 0

var float s_high = na , var float s_low = na , var int Bar_s_high = 0 , var int Bar_s_low = 0

var bool Structure_Trend = false

bool Change_up = false , bool Change_down = false

var H_bar_ary = array.new_int(0,na) , var L_bar_ary = array.new_int(0,na)

var High_ary = array.new_float(0,na) , var Low_ary = array.new_float(0,na)

value_array_unshift(array, new_value_to_add) =>

if array.size(array) > 10

array.remove(array,10)

array.unshift(array, new_value_to_add)

//first trend

if na(s_high) and barstate.isconfirmed

if close > open

Structure_Trend := true

s_high := high

s_low := low

// Direction dwon

if not Structure_Trend and not na(s_high) and barstate.isconfirmed

//trend change up

if close > s_high

if low <= s_low

big_low := low , Bar_big_low := bar_index

if low > s_low

big_low := s_low , Bar_big_low := Bar_s_low

value_array_unshift(Low_ary , big_low) , value_array_unshift(L_bar_ary , Bar_big_low)

Structure_Trend := true , Change_up := true

s_high := high , s_low := low , Bar_s_high := bar_index , Bar_s_low := bar_index

if not Change_up and low <= s_low

s_high := high , s_low := low , Bar_s_high := bar_index , Bar_s_low := bar_index

// Direction up

if Structure_Trend and not na(s_high) and barstate.isconfirmed

//trend change down

if close < s_low

if high >= s_high

big_high := high , Bar_big_high := bar_index

if high < s_high

big_high := s_high , Bar_big_high := Bar_s_high

value_array_unshift(High_ary , big_high) , value_array_unshift(H_bar_ary , Bar_big_high)

Structure_Trend := false , Change_down := true

s_high := high , s_low := low , Bar_s_high := bar_index , Bar_s_low := bar_index

if not Change_down and high >= s_high

s_high := high , s_low := low , Bar_s_high := bar_index , Bar_s_low := bar_index

var line sm_line = na , var line sm_line2 = na

var big_line = array.new_line(7,na)

add_array_unshift(array, new_value_to_add) =>

line.delete(array.get(array, 6))

array.remove(array,6)

array.unshift(array, new_value_to_add)

if show_line

if Change_up

add_array_unshift(big_line,line.new( Bar_big_high[1] , big_high[1] , Bar_big_low , big_low ,xloc = xloc.bar_index , color = Color_sw , style = get_line_style(sw_line_style)))

if Change_down

add_array_unshift(big_line,line.new( Bar_big_high , big_high , Bar_big_low[1] , big_low[1] ,xloc = xloc.bar_index , color = Color_sw , style = get_line_style(sw_line_style)))

line.delete(sm_line[1]) , line.delete(sm_line2[1])

bb_bar = Structure_Trend ? Bar_big_low : Bar_big_high , bb_price = Structure_Trend ? big_low : big_high

cc_bar = Structure_Trend ? Bar_s_high : Bar_s_low , cc_price = Structure_Trend ? s_high : s_low

sm_line := line.new( bb_bar , bb_price , cc_bar , cc_price ,xloc = xloc.bar_index , color = Color_sw , style = get_line_style(sw_line_style))

sm_line2 := line.new( cc_bar , cc_price , bar_index , close ,xloc = xloc.bar_index , color = Color_sw , style = get_line_style(sw_line_style))

//===================================================

atr_sl = ta.ema(ta.tr(true), length_atr)

var int c_order_buy = 0 , var int c_order_sell = 0

var float stop_loss_long = 0 , var float stop_loss_short = 0

var float take_profit_long = 0 , var float take_profit_short = 0

var float open_long = 0 , var float open_short = 0

var int time_buy = 0 , var int time_sell = 0

bool cencel_buy = false , bool cencel_sell = false

bool im_buy_signal = false , bool im_sell_signal = false

bool buy_signal = false , bool sell_signal = false

var bool pending_buy = false , var bool pending_sell = false

var float Fibo_1 = na , var float Fibo_2 = na , var float Fibo_3 = na

var bool cf_con_buy = false , var bool cf_con_sell = false

bar_plus1 = 1 , bar_plus = 2

//Condition Buy

var float sl_b = na , var float entry_b = na , var float sl2_b = na

var int bar_sl_b = 0 , var int bar_entry_b = 0 , var int bar_sl2_b = 0

var int bar_last_b = 0 , var float last_b = na

if strategy.position_size > 0

pending_buy := false

if strategy.closedtrades > strategy.closedtrades[1] and pending_buy and barstate.isconfirmed

im_buy_signal := true , pending_buy := false

if pending_buy and con_time[1] and not con_time and barstate.isconfirmed

strategy.cancel("Long "+str.tostring(c_order_buy))

pending_buy := false , cencel_buy := true

if Change_up and array.size(High_ary) > 4

H_0 = array.get(High_ary,0) , H_1 = array.get(High_ary,1) , H_2 = array.get(High_ary,2)

L_0 = array.get(Low_ary,0) , L_1 = array.get(Low_ary,1) , L_2 = array.get(Low_ary,2) , L_3 = array.get(Low_ary,3) , L_4 = array.get(Low_ary,4)

bar_H_0 = array.get(H_bar_ary,0) , bar_H_1 = array.get(H_bar_ary,1) , bar_H_2 = array.get(H_bar_ary,2)

bar_L_0 = array.get(L_bar_ary,0) , bar_L_1 = array.get(L_bar_ary,1) , bar_L_2 = array.get(L_bar_ary,2)

Fibo1_more = H_0-(Swing1_more/100)*(H_0-L_1) , Fibo1_less = H_0-(Swing1_less/100)*(H_0-L_1)

Fibo2_more = H_0-(Swing2_more/100)*(H_0-L_1) , Fibo2_less = H_0-(Swing2_less/100)*(H_0-L_1)

Fibo3_more = L_1+(Swing3_more/100)*(H_0-L_1) , Fibo3_less = L_1+(Swing3_less/100)*(H_0-L_1)

Price_more = (Size_candle_more * atr_sl) + L_1 , Price_less = (Size_candle_less * atr_sl) + L_1

cf_buy1 = L_0 <= Fibo1_more and L_0 >= Fibo1_less

cf_buy2 = use_Swing2 ? L_2 <= Fibo2_more and L_2 >= Fibo2_less : true

cf_buy3 = use_Swing3 ? H_1 >= Fibo3_more and H_1 <= Fibo3_less : true

cf_buy4 = use_size ? H_0 > Price_more and H_0 < Price_less : true

if cf_buy1 and cf_buy2 and cf_buy3 and cf_buy4

if cf_con_sell

cf_con_sell := false

if pending_sell

strategy.cancel("Short "+str.tostring(c_order_sell))

pending_sell := false , cencel_sell := true

if pending_buy

strategy.cancel("Long "+str.tostring(c_order_buy))

pending_buy := false , cencel_buy := true

if B_long and strategy.position_size == 0

cf_con_buy := true

sl_b := L_0 < L_1 ? L_0 : L_1 , bar_sl_b := L_0 < L_1 ? bar_L_0 : bar_L_1

sl2_b := L_0 < L_1 ? L_1 : L_0 , bar_sl2_b := L_0 < L_1 ? bar_L_1 : bar_L_0

last_b := L_0 , bar_last_b := bar_L_0

entry_b := H_0 , bar_entry_b := bar_H_0

if B_long

if show_CF_fibo

lbl_swing1_a = label.new( bar_L_0+bar_plus , Fibo1_more , "Fibo"+str.tostring(Swing1_more) , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_swing1_b = label.new( bar_L_0+bar_plus , Fibo1_less , "Fibo"+str.tostring(Swing1_less) , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_swing1_c = label.new( bar_L_0 , L_0 , stxt1 , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_up, size = In_Size_fibo)

box_cfbuy1_his = box.new(xloc = xloc.bar_index , left = bar_L_0-bar_plus1 , top = Fibo1_more, right = bar_L_0+bar_plus1 , bottom = Fibo1_less , border_color = col_cf_con1 ,bgcolor = col_cf_con1)

if use_Swing2

i_Mark_2 = label.new(bar_L_2, L_2 ,xloc = xloc.bar_index, text = "●",color = TRANSP, style = label.style_label_center,textcolor = Color_Mark_Swing_i1,size = size.small)

if show_CF_fibo

lbl_swing2_a = label.new( bar_L_2+bar_plus , Fibo2_more , "Fibo"+str.tostring(Swing2_more) , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_swing2_b = label.new( bar_L_2+bar_plus , Fibo2_less , "Fibo"+str.tostring(Swing2_less) , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_swing2_c = label.new( bar_L_2 , L_2 , stxt2 , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_up, size = In_Size_fibo)

box_cfbuy2_his = box.new(xloc = xloc.bar_index , left = bar_L_2-bar_plus1 , top = Fibo2_more, right = bar_L_2+bar_plus1 , bottom = Fibo2_less , border_color = col_cf_con1 ,bgcolor = col_cf_con1)

if use_Swing3

i_Mark_3 = label.new(bar_H_1, H_1 ,xloc = xloc.bar_index, text = "●",color = TRANSP, style = label.style_label_center,textcolor = Color_Mark_Swing_i1,size = size.small)

if show_CF_fibo

lbl_swing3_a = label.new( bar_H_1+bar_plus , Fibo3_more , "Fibo"+str.tostring(Swing3_more) , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_swing3_b = label.new( bar_H_1+bar_plus , Fibo3_less , "Fibo"+str.tostring(Swing3_less) , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_swing3_c = label.new( bar_H_1 , H_1 , stxt3 , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_down, size = In_Size_fibo)

box_cfbuy3_his = box.new(xloc = xloc.bar_index , left = bar_H_1-bar_plus1 , top = Fibo3_more, right = bar_H_1+bar_plus1 , bottom = Fibo3_less , border_color = col_cf_con1 ,bgcolor = col_cf_con1)

line_1 = line.new( bar_L_0 , L_0 , bar_H_0 , H_0 ,xloc = xloc.bar_index , color = Color_sw , style = get_line_style(sw_line_style))

line_2 = line.new( bar_L_1 , L_1 , bar_H_0 , H_0 ,xloc = xloc.bar_index , color = Color_sw , style = get_line_style(sw_line_style))

line_3 = line.new( bar_L_1 , L_1 , bar_H_1 , H_1 ,xloc = xloc.bar_index , color = Color_sw , style = get_line_style(sw_line_style))

line_4 = line.new( bar_L_2 , L_2 , bar_H_1 , H_1 ,xloc = xloc.bar_index , color = Color_sw , style = get_line_style(sw_line_style))

line_5 = line.new( bar_L_2 , L_2 , bar_H_2 , H_2 ,xloc = xloc.bar_index , color = Color_sw , style = get_line_style(sw_line_style))

i_Mark_1 = label.new(bar_L_0, L_0 ,xloc = xloc.bar_index, text = "●",color = TRANSP, style = label.style_label_center,textcolor = Color_Mark_Swing_i1,size = size.small)

i_Mark_4 = label.new(bar_H_0, H_0 ,xloc = xloc.bar_index, text = "●",color = TRANSP, style = label.style_label_center,textcolor = Color_Mark_Swing_i2,size = size.normal)

i_Mark_5 = label.new(bar_L_1, L_1 ,xloc = xloc.bar_index, text = "●",color = TRANSP, style = label.style_label_center,textcolor = Color_Mark_Swing_i2,size = size.normal)

lbl_swing_A = label.new( bar_L_1 , L_1 , "Swing A" , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_up, size = In_Size_fibo)

lbl_swing_B = label.new( bar_H_0 , H_0 , "Swing B" , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_down, size = In_Size_fibo)

if use_size and show_CF_candle

line_size_1 = line.new( bar_L_1 , Price_more , bar_H_0 , Price_more ,xloc = xloc.bar_index , color = Color_candle_2 , style = get_line_style(sw_line_style))

line_size_2 = line.new( bar_L_1 , Price_less , bar_H_0 , Price_less ,xloc = xloc.bar_index , color = Color_candle_1 , style = get_line_style(sw_line_style))

lbl_size_a = label.new( (bar_L_1+bar_H_0)/2 , Price_more , "Min" , xloc = xloc.bar_index , color = Color_candle_2, textcolor = Color_candle_txt, style = label.style_label_center, size = In_Size_CF_candle)

lbl_size_b = label.new( (bar_L_1+bar_H_0)/2 , Price_less , "Max" , xloc = xloc.bar_index , color = Color_candle_1, textcolor = Color_candle_txt, style = label.style_label_center, size = In_Size_CF_candle)

Line_draw_buy = false , var wait_b_line = false

if cf_con_buy and B_long and close >= entry_b and barstate.isconfirmed and strategy.position_size == 0

cf_con_buy := false , Line_draw_buy := true , wait_b_line := true

if con_time and con_date

buy_signal := true

if cf_con_buy and B_long and close <= sl_b and barstate.isconfirmed and strategy.position_size == 0

cf_con_buy := false , Line_draw_buy := true

line_last = line.new( Bar_big_high , big_high , bar_last_b , last_b ,xloc = xloc.bar_index , color = Color_sw , style = get_line_style(sw_line_style))

if wait_b_line and Change_down and barstate.isconfirmed

line_last = line.new( Bar_big_high , big_high , bar_last_b , last_b ,xloc = xloc.bar_index , color = Color_sw , style = get_line_style(sw_line_style))

wait_b_line := false

var line lineB_to_CF = na , var line lineB_to_cancel = na

var label lblB_to_CF = na , var label lblB_to_cancel = na

if cf_con_buy and show_CF_line and barstate.isconfirmed

line.delete(lineB_to_CF[1]) , line.delete(lineB_to_cancel[1]) , label.delete(lblB_to_CF[1]) , label.delete(lblB_to_cancel[1])

lineB_to_CF := line.new( bar_entry_b , entry_b , bar_index , entry_b ,xloc = xloc.bar_index , color = Color_tesst_1 , style = line.style_dashed )

lineB_to_cancel := line.new( bar_sl_b , sl_b , bar_index , sl_b ,xloc = xloc.bar_index , color = Color_tesst_2 , style = line.style_dashed )

lblB_to_CF := label.new(bar_index, entry_b , "Break to confitm" ,xloc = xloc.bar_index, color = TRANSP, textcolor = Color_tesst_1, style = label.style_label_down, size = In_Size_CF_line)

lblB_to_cancel := label.new(bar_index, sl_b , "Cancel Line",xloc = xloc.bar_index, color = TRANSP, textcolor = Color_tesst_2, style = label.style_label_up, size = In_Size_CF_line)

if Line_draw_buy and show_CF_line and barstate.isconfirmed

line.delete(lineB_to_CF[1]) , line.delete(lineB_to_cancel[1]) , label.delete(lblB_to_CF[1]) , label.delete(lblB_to_cancel[1])

lineB_CF = line.new( bar_entry_b , entry_b , bar_index , entry_b ,xloc = xloc.bar_index , color = Color_tesst_1 , style = line.style_dashed )

lineB_cancel = line.new( bar_sl_b , sl_b , bar_index , sl_b ,xloc = xloc.bar_index , color = Color_tesst_2 , style = line.style_dashed )

lblB_cf = label.new(bar_index, entry_b , "Break to confitm" ,xloc = xloc.bar_index, color = #ffffff00, textcolor = Color_tesst_1, style = label.style_label_down, size = In_Size_CF_line)

lblB_cancel = label.new(bar_index, sl_b , "Cancel Line" ,xloc = xloc.bar_index, color = #ffffff00, textcolor = Color_tesst_2, style = label.style_label_up, size = In_Size_CF_line)

//Condition Sell

var float sl_s = na , var float entry_s = na , var float sl2_s = na

var int bar_sl_s = 0 , var int bar_entry_s = 0 , var int bar_sl2_s = 0

var float last_s = na , var int bar_last_s = 0

if strategy.position_size < 0

pending_sell := false

if strategy.closedtrades > strategy.closedtrades[1] and pending_sell and barstate.isconfirmed

im_sell_signal := true , pending_sell := false

if pending_sell and con_time[1] and not con_time and barstate.isconfirmed

strategy.cancel("Short "+str.tostring(c_order_sell))

pending_sell := false , cencel_sell := true

if Change_down and array.size(Low_ary) > 4

H_0 = array.get(High_ary,0) , H_1 = array.get(High_ary,1) , H_2 = array.get(High_ary,2) , H_3 = array.get(High_ary,3) , H_4 = array.get(High_ary,4)

L_0 = array.get(Low_ary,0) , L_1 = array.get(Low_ary,1) , L_2 = array.get(Low_ary,2)

bar_H_0 = array.get(H_bar_ary,0) , bar_H_1 = array.get(H_bar_ary,1) , bar_H_2 = array.get(H_bar_ary,2)

bar_L_0 = array.get(L_bar_ary,0) , bar_L_1 = array.get(L_bar_ary,1) , bar_L_2 = array.get(L_bar_ary,2)

Fibo1_more = L_0+(Swing1_more/100)*(H_1-L_0) , Fibo1_less = L_0+(Swing1_less/100)*(H_1-L_0)

Fibo2_more = L_0+(Swing2_more/100)*(H_1-L_0) , Fibo2_less = L_0+(Swing2_less/100)*(H_1-L_0)

Fibo3_more = H_1-(Swing3_more/100)*(H_1-L_0) , Fibo3_less = H_1-(Swing3_less/100)*(H_1-L_0)

Price_more = H_1 - (Size_candle_more * atr_sl) , Price_less = H_1 - (Size_candle_less * atr_sl)

cf_sell1 = H_0 >= Fibo1_more and H_0 <= Fibo1_less

cf_sell2 = use_Swing2 ? H_2 >= Fibo2_more and H_2 <= Fibo2_less : true

cf_sell3 = use_Swing3 ? L_1 <= Fibo3_more and L_1 >= Fibo3_less : true

cf_sell4 = use_size ? L_0 <= Price_more and L_0 >= Price_less : true

if cf_sell1 and cf_sell2 and cf_sell3 and cf_sell4

if cf_con_buy

cf_con_buy := false

if pending_buy

strategy.cancel("Long "+str.tostring(c_order_buy))

pending_buy := false , cencel_buy := true

if pending_sell

strategy.cancel("Short "+str.tostring(c_order_sell))

pending_sell := false , cencel_sell := true

if S_short and strategy.position_size == 0

cf_con_sell := true

sl_s := H_0 > H_1 ? H_0 : H_1 , bar_sl_s := H_0 > H_1 ? bar_H_0 : bar_H_1

sl2_s := H_0 > H_1 ? H_1 : H_0 , bar_sl2_s := H_0 > H_1 ? bar_H_1 : bar_H_0

last_s := H_0 , bar_last_s := bar_H_0

entry_s := L_0 , bar_entry_s := bar_L_0

if S_short

if show_CF_fibo

lbl_swing1_a = label.new( bar_H_0+bar_plus , Fibo1_more , "Fibo"+str.tostring(Swing1_more) , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_swing1_b = label.new( bar_H_0+bar_plus , Fibo1_less , "Fibo"+str.tostring(Swing1_less) , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_swing1_c = label.new( bar_H_0 , H_0 , stxt1 , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_down, size = In_Size_fibo)

box_cfbuy1_his = box.new(xloc = xloc.bar_index , left = bar_H_0-bar_plus1 , top = Fibo1_more, right = bar_H_0+bar_plus1 , bottom = Fibo1_less , border_color = col_cf_con2 ,bgcolor = col_cf_con2)

if use_Swing2

i_Mark_2 = label.new(bar_H_2, H_2 ,xloc = xloc.bar_index, text = "●",color = TRANSP, style = label.style_label_center,textcolor = Color_Mark_Swing_i1,size = size.small)

if show_CF_fibo

lbl_swing2_a = label.new( bar_H_2+bar_plus , Fibo2_more , "Fibo"+str.tostring(Swing2_more) , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_swing2_b = label.new( bar_H_2+bar_plus , Fibo2_less , "Fibo"+str.tostring(Swing2_less) , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_swing2_c = label.new( bar_H_2 , H_2 , stxt2 , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_down, size = In_Size_fibo)

box_cfbuy2_his = box.new(xloc = xloc.bar_index , left = bar_H_2-bar_plus1 , top = Fibo2_more, right = bar_H_2+bar_plus1 , bottom = Fibo2_less , border_color = col_cf_con2 ,bgcolor = col_cf_con2)

if use_Swing3

i_Mark_3 = label.new(bar_L_1, L_1 ,xloc = xloc.bar_index, text = "●",color = TRANSP, style = label.style_label_center,textcolor = Color_Mark_Swing_i1,size = size.small)

if show_CF_fibo

lbl_swing3_a = label.new( bar_L_1+bar_plus , Fibo3_more , "Fibo"+str.tostring(Swing3_more) , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_swing3_b = label.new( bar_L_1+bar_plus , Fibo3_less , "Fibo"+str.tostring(Swing3_less) , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_swing3_c = label.new( bar_L_1 , L_1 , stxt3 , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_up, size = In_Size_fibo)

box_cfbuy3_his = box.new(xloc = xloc.bar_index , left = bar_L_1-bar_plus1 , top = Fibo3_more, right = bar_L_1+bar_plus1 , bottom = Fibo3_less , border_color = col_cf_con2 ,bgcolor = col_cf_con2)

line_1 = line.new( bar_H_0 , H_0 , bar_L_0 , L_0 ,xloc = xloc.bar_index , color = Color_sw , style = get_line_style(sw_line_style))

line_2 = line.new( bar_H_1 , H_1 , bar_L_0 , L_0 ,xloc = xloc.bar_index , color = Color_sw , style = get_line_style(sw_line_style))

line_3 = line.new( bar_H_1 , H_1 , bar_L_1 , L_1 ,xloc = xloc.bar_index , color = Color_sw , style = get_line_style(sw_line_style))

line_4 = line.new( bar_H_2 , H_2 , bar_L_1 , L_1 ,xloc = xloc.bar_index , color = Color_sw , style = get_line_style(sw_line_style))

line_5 = line.new( bar_H_2 , H_2 , bar_L_2 , L_2 ,xloc = xloc.bar_index , color = Color_sw , style = get_line_style(sw_line_style))

i_Mark_1 = label.new(bar_H_0, H_0 ,xloc = xloc.bar_index, text = "●",color = TRANSP, style = label.style_label_center,textcolor = Color_Mark_Swing_i1,size = size.small)

i_Mark_4 = label.new(bar_L_0, L_0 ,xloc = xloc.bar_index, text = "●",color = TRANSP, style = label.style_label_center,textcolor = Color_Mark_Swing_i2,size = size.normal)

i_Mark_5 = label.new(bar_H_1, H_1 ,xloc = xloc.bar_index, text = "●",color = TRANSP, style = label.style_label_center,textcolor = Color_Mark_Swing_i2,size = size.normal)

lbl_swing_A = label.new( bar_H_1 , H_1 , "Swing A" , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_down, size = In_Size_fibo)

lbl_swing_B = label.new( bar_L_0 , L_0 , "Swing B" , xloc = xloc.bar_index , color = TRANSP, textcolor = text_line2_col, style = label.style_label_up, size = In_Size_fibo)

if use_size and show_CF_candle

line_size_1 = line.new( bar_H_1 , Price_more , bar_L_0 , Price_more ,xloc = xloc.bar_index , color = Color_candle_2 , style = get_line_style(sw_line_style))

line_size_2 = line.new( bar_H_1 , Price_less , bar_L_0 , Price_less ,xloc = xloc.bar_index , color = Color_candle_1 , style = get_line_style(sw_line_style))

lbl_size_a = label.new( (bar_H_1+bar_L_0)/2 , Price_more , "Min", xloc = xloc.bar_index , color = Color_candle_2, textcolor = Color_candle_txt, style = label.style_label_center, size = In_Size_CF_candle)

lbl_size_b = label.new( (bar_H_1+bar_L_0)/2 , Price_less , "Max", xloc = xloc.bar_index , color = Color_candle_1, textcolor = Color_candle_txt, style = label.style_label_center, size = In_Size_CF_candle)

Line_draw_sell = false , var wait_s_line = false

if cf_con_sell and S_short and close <= entry_s and barstate.isconfirmed and strategy.position_size == 0

cf_con_sell := false , Line_draw_sell := true , wait_s_line := true

if con_time and con_date

sell_signal := true

if cf_con_sell and S_short and close >= sl_s and barstate.isconfirmed and strategy.position_size == 0

cf_con_sell := false , Line_draw_sell := true

line_last = line.new( Bar_big_low , big_low , bar_last_s, last_s ,xloc = xloc.bar_index , color = Color_sw , style = get_line_style(sw_line_style))

if wait_s_line and Change_up and barstate.isconfirmed

line_last = line.new( Bar_big_low , big_low , bar_last_s, last_s ,xloc = xloc.bar_index , color = Color_sw , style = get_line_style(sw_line_style))

wait_s_line := false

var line lineS_to_CF = na , var line lineS_to_cancel = na

var label lblS_to_CF = na , var label lblS_to_cancel = na

if cf_con_sell and show_CF_line and barstate.isconfirmed

line.delete(lineS_to_CF[1]) , line.delete(lineS_to_cancel[1]) , label.delete(lblS_to_CF[1]) , label.delete(lblS_to_cancel[1])

lineS_to_CF := line.new( bar_entry_s , entry_s , bar_index , entry_s ,xloc = xloc.bar_index , color = Color_tesst_1 , style = line.style_dashed )

lineS_to_cancel := line.new( bar_sl_s , sl_s , bar_index , sl_s ,xloc = xloc.bar_index , color = Color_tesst_2 , style = line.style_dashed )

lblS_to_CF := label.new(bar_index, entry_s , "Break to confitm" ,xloc = xloc.bar_index, color = TRANSP, textcolor = Color_tesst_1, style = label.style_label_up, size = In_Size_CF_line)

lblS_to_cancel := label.new(bar_index, sl_s , "Cancel Line",xloc = xloc.bar_index, color = TRANSP, textcolor = Color_tesst_2, style = label.style_label_down, size = In_Size_CF_line)

if Line_draw_sell and show_CF_line and barstate.isconfirmed

line.delete(lineS_to_CF[1]) , line.delete(lineS_to_cancel[1]) , label.delete(lblS_to_CF[1]) , label.delete(lblS_to_cancel[1])

lineS_CF = line.new( bar_entry_s , entry_s , bar_index , entry_s ,xloc = xloc.bar_index , color = Color_tesst_1 , style = line.style_dashed )

lineS_cancel = line.new( bar_sl_s , sl_s , bar_index , sl_s ,xloc = xloc.bar_index , color = Color_tesst_2 , style = line.style_dashed )

lblS_cf = label.new(bar_index, entry_s , "Break to confitm" ,xloc = xloc.bar_index, color = TRANSP, textcolor = Color_tesst_1, style = label.style_label_up, size = In_Size_CF_line)

lblS_cancel = label.new(bar_index, sl_s , "Cancel Line" ,xloc = xloc.bar_index, color = TRANSP, textcolor = Color_tesst_2, style = label.style_label_down, size = In_Size_CF_line)

// === Position Size ===

risk_pips = atr_sl * x_ATR

value_remove2(va1 , va2 , size) =>

array.remove(va1,size) , array.remove(va2,size)

var tp_buy = array.new_float(0,na) , var sl_buy = array.new_float(0,na)

var tp_sell = array.new_float(0,na) , var sl_sell = array.new_float(0,na)

var int Loss_Buy = 0 , var int Win_Buy = 0 , var float sl_trade_buy = na , var float tp_trade_buy = na

var int Loss_Sell = 0 , var int Win_Sell = 0 , var float sl_trade_sell = na , var float tp_trade_sell = na

if cencel_buy and array.size(tp_buy) > 0

tp_trade_buy := na , sl_trade_buy := na

for i = array.size(tp_buy)-1 to 0

value_remove2( tp_buy , sl_buy , i)

if cencel_sell and array.size(tp_sell) > 0

tp_trade_sell := na , sl_trade_sell := na

for i = array.size(tp_sell)-1 to 0

value_remove2( tp_sell , sl_sell , i)

// === Long Entry ===

if buy_signal and con_time and con_date and barstate.isconfirmed

sl_cal_long = Sl_change ? sl2_b : sl_b

open_long := entry_b-math.abs((fibo_entry / 100)*(entry_b-sl_cal_long))

stop_loss_long := sl_cal_long - risk_pips

take_profit_long := open_long + (open_long - stop_loss_long)*rr_ratio

c_order_buy += 1

cs_buy = str.tostring(c_order_buy)

strategy.entry("Long "+cs_buy, strategy.long , na , limit = open_long )

strategy.exit("Long Exit "+cs_buy , "Long "+cs_buy , stop = stop_loss_long , limit = take_profit_long , comment_profit = "Long(Tp) "+cs_buy ,comment_loss = "Long(SL) "+cs_buy )

p_entry = "\n\nEntry price = "+str.tostring( open_long , format.mintick)

p_sl = "\n\nStop loss = "+str.tostring(stop_loss_long, format.mintick)

p_tp = "\n\nTarget profit = "+str.tostring(take_profit_long, format.mintick)

alert("Long_"+p_entry+p_sl+p_tp, alert.freq_all)

pending_buy := true , time_buy := bar_index

array.unshift(tp_buy, take_profit_long) , array.unshift(sl_buy,stop_loss_long)

// === Short Entry ===

if sell_signal and con_time and con_date and barstate.isconfirmed

sl_cal_short = Sl_change ? sl2_s : sl_s

open_short := entry_s+((fibo_entry / 100) *(sl_cal_short-entry_s))

stop_loss_short := sl_cal_short + risk_pips

take_profit_short := open_short - (stop_loss_short - open_short)*rr_ratio

c_order_sell += 1

cs_sell = str.tostring(c_order_sell)

strategy.entry("Short "+cs_sell, strategy.short , na , limit = open_short )

strategy.exit("Short Exit "+cs_sell ,"Short "+cs_sell , stop = stop_loss_short , limit = take_profit_short , comment_profit = "Short(Tp) "+cs_sell ,comment_loss = "Short(SL) "+cs_sell )

p_entry = "\n\nEntry price = "+str.tostring( open_short , format.mintick)

p_sl = "\n\nStop loss = "+str.tostring(stop_loss_short, format.mintick)

p_tp = "\n\nTarget profit = "+str.tostring(take_profit_short, format.mintick)

alert("Short_"+p_entry+p_sl+p_tp, alert.freq_all)

pending_sell := true , time_sell := bar_index

array.unshift(tp_sell, take_profit_short) , array.unshift(sl_sell,stop_loss_short)

//show pending

n_bar = 5

col_1 = color.rgb(8, 153, 129, 80), col_2 = color.rgb(242, 54, 70, 80)

box box_entrybuy_1_his = na , box box_entrybuy_2_his = na

box box_entrysell_1_his = na , box box_entrysell_2_his = na

label lbl_entry_his = na , label lbl_tp_his = na , label lbl_sl_his = na

var label lbl_entry_t = na , var label lbl_tp_t = na , var label lbl_sl_t = na

var box box_entry_t1 = na , var box box_entry_t2 = na

//show Buy

if strategy.position_size > 0 or im_buy_signal and barstate.isconfirmed

box.delete(box_entry_t1[1]) , box.delete(box_entry_t2[1]) , label.delete(lbl_entry_t[1]) , label.delete(lbl_tp_t[1]) , label.delete(lbl_sl_t[1])

box.delete(box_entrybuy_1_his[1]) , box.delete(box_entrybuy_2_his[1]) , label.delete(lbl_entry_his[1]) , label.delete(lbl_tp_his[1]) , label.delete(lbl_sl_his[1])

box_entrybuy_1_his := box.new(xloc = xloc.bar_index ,left = time_buy , top = take_profit_long, right = bar_index+n_bar , bottom = open_long , border_color = col_1 ,bgcolor = col_1)

box_entrybuy_2_his := box.new(xloc = xloc.bar_index ,left = time_buy , top = open_long, right = bar_index+n_bar , bottom = stop_loss_long , border_color = col_2 ,bgcolor = col_2)

lbl_entry_his := label.new(bar_index+n_bar, open_long , str.tostring(open_long,format.mintick) ,xloc = xloc.bar_index, color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_tp_his := label.new(bar_index+n_bar, take_profit_long , str.tostring(take_profit_long,format.mintick),xloc = xloc.bar_index, color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_sl_his := label.new(bar_index+n_bar, stop_loss_long , str.tostring(stop_loss_long,format.mintick) ,xloc = xloc.bar_index, color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

if cencel_buy and barstate.isconfirmed

box.delete(box_entry_t1[1]) , box.delete(box_entry_t2[1]) , label.delete(lbl_entry_t[1]) , label.delete(lbl_tp_t[1]) , label.delete(lbl_sl_t[1])

box.delete(box_entrybuy_1_his[1]) , box.delete(box_entrybuy_2_his[1]) , label.delete(lbl_entry_his[1]) , label.delete(lbl_tp_his[1]) , label.delete(lbl_sl_his[1])

box_entrybuy_1_his := box.new(xloc = xloc.bar_index ,left = time_buy[1] , top = take_profit_long[1] , right = time_buy[1]+n_bar , bottom = open_long[1] , border_color = col_1 ,bgcolor = col_1)

box_entrybuy_2_his := box.new(xloc = xloc.bar_index ,left = time_buy[1] , top = open_long[1] , right = time_buy[1]+n_bar , bottom = stop_loss_long[1] , border_color = col_2 ,bgcolor = col_2)

lbl_entry_his := label.new(time_buy[1]+n_bar, open_long[1] , str.tostring(open_long[1],format.mintick) ,xloc = xloc.bar_index, color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_tp_his := label.new(time_buy[1]+n_bar, take_profit_long[1] , str.tostring(take_profit_long[1],format.mintick),xloc = xloc.bar_index, color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_sl_his := label.new(time_buy[1]+n_bar, stop_loss_long[1] , str.tostring(stop_loss_long[1],format.mintick) ,xloc = xloc.bar_index, color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

//show sell

if strategy.position_size < 0 or im_sell_signal and barstate.isconfirmed

box.delete(box_entry_t1[1]) , box.delete(box_entry_t2[1]) , label.delete(lbl_entry_t[1]) , label.delete(lbl_tp_t[1]) , label.delete(lbl_sl_t[1])

box.delete(box_entrysell_1_his[1]) , box.delete(box_entrysell_2_his[1]) , label.delete(lbl_entry_his[1]) , label.delete(lbl_tp_his[1]) , label.delete(lbl_sl_his[1])

box_entrysell_1_his := box.new(xloc = xloc.bar_index , left = time_sell , top = take_profit_short, right = bar_index+n_bar , bottom = open_short , border_color = col_1 ,bgcolor = col_1)

box_entrysell_2_his := box.new(xloc = xloc.bar_index , left = time_sell , top = open_short, right = bar_index+n_bar , bottom = stop_loss_short , border_color = col_2 ,bgcolor = col_2)

lbl_entry_his := label.new(bar_index+n_bar , open_short , str.tostring(open_short,format.mintick) ,xloc = xloc.bar_index, color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_tp_his := label.new(bar_index+n_bar , take_profit_short , str.tostring(take_profit_short,format.mintick),xloc = xloc.bar_index, color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_sl_his := label.new(bar_index+n_bar , stop_loss_short , str.tostring(stop_loss_short,format.mintick) ,xloc = xloc.bar_index, color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

if cencel_sell and barstate.isconfirmed

box.delete(box_entry_t1[1]) , box.delete(box_entry_t2[1]) , label.delete(lbl_entry_t[1]) , label.delete(lbl_tp_t[1]) , label.delete(lbl_sl_t[1])

box.delete(box_entrysell_1_his[1]) , box.delete(box_entrysell_2_his[1]) , label.delete(lbl_entry_his[1]) , label.delete(lbl_tp_his[1]) , label.delete(lbl_sl_his[1])

box_entrysell_1_his := box.new(xloc = xloc.bar_index , left = time_sell[1] , top = take_profit_short[1], right = time_sell[1]+n_bar , bottom = open_short[1] , border_color = col_1 ,bgcolor = col_1)

box_entrysell_2_his := box.new(xloc = xloc.bar_index , left = time_sell[1] , top = open_short[1], right = time_sell[1]+n_bar , bottom = stop_loss_short[1] , border_color = col_2 ,bgcolor = col_2)

lbl_entry_his := label.new(time_sell[1]+n_bar , open_short[1] , str.tostring(open_short[1],format.mintick) ,xloc = xloc.bar_index, color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_tp_his := label.new(time_sell[1]+n_bar , take_profit_short[1] , str.tostring(take_profit_short[1],format.mintick),xloc = xloc.bar_index, color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_sl_his := label.new(time_sell[1]+n_bar , stop_loss_short[1] , str.tostring(stop_loss_short[1],format.mintick) ,xloc = xloc.bar_index, color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

if buy_signal and barstate.isconfirmed

box.delete(box_entry_t1[1]) , box.delete(box_entry_t2[1]) , label.delete(lbl_entry_t[1]) , label.delete(lbl_tp_t[1]) , label.delete(lbl_sl_t[1])

box_entry_t1 := box.new(xloc = xloc.bar_index ,left = time_buy , top = take_profit_long, right = bar_index+n_bar , bottom = open_long , border_color = col_1 ,bgcolor = col_1)

box_entry_t2 := box.new(xloc = xloc.bar_index ,left = time_buy , top = open_long, right = bar_index+n_bar , bottom = stop_loss_long , border_color = col_2 ,bgcolor = col_2)

lbl_entry_t := label.new(bar_index+n_bar, open_long , str.tostring(open_long,format.mintick) ,xloc = xloc.bar_index, color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_tp_t := label.new(bar_index+n_bar, take_profit_long , str.tostring(take_profit_long,format.mintick),xloc = xloc.bar_index, color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_sl_t := label.new(bar_index+n_bar, stop_loss_long , str.tostring(stop_loss_long,format.mintick) ,xloc = xloc.bar_index, color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

if sell_signal and barstate.isconfirmed

box.delete(box_entrysell_1_his[1]) , box.delete(box_entry_t2[1]) , label.delete(lbl_entry_t[1]) , label.delete(lbl_tp_t[1]) , label.delete(lbl_sl_t[1])

box_entry_t1 := box.new(xloc = xloc.bar_index , left = time_sell , top = take_profit_short, right = bar_index+n_bar , bottom = open_short , border_color = col_1 ,bgcolor = col_1)

box_entry_t2 := box.new(xloc = xloc.bar_index , left = time_sell , top = open_short, right = bar_index+n_bar , bottom = stop_loss_short , border_color = col_2 ,bgcolor = col_2)

lbl_entry_t := label.new(bar_index+n_bar , open_short , str.tostring(open_short,format.mintick) ,xloc = xloc.bar_index, color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_tp_t := label.new(bar_index+n_bar , take_profit_short , str.tostring(take_profit_short,format.mintick),xloc = xloc.bar_index, color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

lbl_sl_t := label.new(bar_index+n_bar , stop_loss_short , str.tostring(stop_loss_short,format.mintick) ,xloc = xloc.bar_index, color = TRANSP, textcolor = text_line2_col, style = label.style_label_center, size = In_Size_fibo)

if Show_result and barstate.isconfirmed

//Check SL buy

if array.size(sl_buy) > 0 and not na(array.get(sl_buy,0))

sl_trade_buy := array.get(sl_buy,0)

if low <= sl_trade_buy and ( strategy.position_size[1] > 0 or im_buy_signal) and array.size(sl_buy) > 0

sl_trade_buy := na , tp_trade_buy := na

for i = array.size(sl_buy)-1 to 0

if low <= array.get(sl_buy,i) and not na(array.get(sl_buy,i))

Loss_Buy += 1

value_remove2( tp_buy , sl_buy , i)

//check TP buy

if array.size(tp_buy) > 0 and not na(array.get(tp_buy,0))

tp_trade_buy := array.get(tp_buy,0)

if high >= tp_trade_buy and ( strategy.position_size[1] > 0 or im_buy_signal) and array.size(tp_buy) > 0

tp_trade_buy := na , sl_trade_buy := na

for i = array.size(tp_buy)-1 to 0

if high >= array.get(tp_buy,i) and not na(array.get(tp_buy,i))

Win_Buy += 1

value_remove2( tp_buy , sl_buy , i)

//Check SL Sell

if array.size(sl_sell) > 0 and not na(array.get(sl_sell,0))

sl_trade_sell := array.get(sl_sell,0)

if high >= sl_trade_sell and ( strategy.position_size[1] < 0 or im_sell_signal) and array.size(sl_sell) > 0

sl_trade_sell := na , tp_trade_sell := na

for i = array.size(sl_sell)-1 to 0

if high >= array.get(sl_sell,i) and not na(array.get(sl_sell,i))

Loss_Sell += 1

value_remove2( tp_sell , sl_sell , i)

//check TP Sell

if array.size(tp_sell) > 0 and not na(array.get(tp_sell,0))

tp_trade_sell := array.get(tp_sell,0)

if low <= tp_trade_sell and ( strategy.position_size[1] < 0 or im_sell_signal) and array.size(tp_sell) > 0

tp_trade_sell := na , sl_trade_sell := na

for i = array.size(tp_sell)-1 to 0

if low <= array.get(tp_sell,i) and not na(array.get(tp_sell,i))

Win_Sell += 1

value_remove2( tp_sell , sl_sell , i)

// === Plotting ===

bgcolor(s_New_York and cf_ses1 ? color.rgb(255, 251, 0, 92) : na ,title = "New York")

bgcolor(s_London and cf_ses2 ? color.rgb(255, 0, 255, 92) : na ,title = "London")

bgcolor(s_Tokyo and cf_ses3? color.rgb(111, 255, 82, 92) : na ,title = "Tokyo")

bgcolor(s_Sydney and cf_ses4? color.rgb(82, 122, 255, 92) : na ,title = "Sydney")

Location_session = ((9*60*60) / timeframe.in_seconds(timeframe.period)) / 2

Lbl_New_York = not cf_ses1 and cf_ses1 != cf_ses1[1] and s_New_York and t_New == '1300-2200' and timeframe.in_seconds(timeframe.period) <= 32400

plotshape( Lbl_New_York , "Session New York", shape.labeldown, location.bottom, na , offset = -Location_session , text = "New York", textcolor = #fffb00, size = size.tiny, display = display.all - display.status_line, editable = false)

Lbl_London = not cf_ses2 and cf_ses2 != cf_ses2[1] and s_London and t_Lon == '0700-1600' and timeframe.in_seconds(timeframe.period) <= 32400

plotshape( Lbl_London , "Session London", shape.labeldown, location.bottom, na , offset = -Location_session , text = "London", textcolor = #ff00ff , size = size.tiny, display = display.all - display.status_line, editable = false)

Lbl_Tokyo = not cf_ses3 and cf_ses3 != cf_ses3[1] and s_Tokyo and t_Tokyo == '0000-0900' and timeframe.in_seconds(timeframe.period) <= 32400

plotshape( Lbl_Tokyo , "Session Tokyo", shape.labeldown, location.bottom, na , offset = -Location_session , text = "Tokyo", textcolor = #6fff52 , size = size.tiny, display = display.all - display.status_line, editable = false)

Lbl_Sydney = not cf_ses4 and cf_ses4 != cf_ses4[1] and s_Sydney and t_Syd == '2100-0600' and timeframe.in_seconds(timeframe.period) <= 32400

plotshape( Lbl_Sydney , "Session Sydney", shape.labeldown, location.bottom, na , offset = -Location_session , text = "Sydney", textcolor = #527aff , size = size.tiny, display = display.all - display.status_line, editable = false)

var table Balane_status = table.new( position(select_position) , 6 , 6 , border_width = 1)

Total_all = Win_Buy + Loss_Buy + Win_Sell + Loss_Sell

if Show_result and (Total_all > Total_all[1]) and barstate.isconfirmed

Long_all = Win_Buy + Loss_Buy , Short_all = Win_Sell + Loss_Sell

Total_win = Win_Buy + Win_Sell , Total_loss = Loss_Buy + Loss_Sell

Factor_all = (Total_win*rr_ratio)/Total_loss

Factor_buy = (Win_Buy*rr_ratio)/Loss_Buy

Factor_sell = (Win_Sell*rr_ratio)/Loss_Sell

txt1_1 = str.tostring(Total_all,format.volume)

txt1_2 = str.tostring(Long_all,format.volume)

txt1_3 = str.tostring(Short_all,format.volume)

txt2_1 = str.tostring(Total_win,format.volume)

txt3_1 = str.tostring(Total_loss,format.volume)

txt4_1 = str.tostring((Total_win/Total_all)*100,format.percent)

txt5_1 = str.format("{0,number,#.##}", Factor_all )

txt2_2 = str.tostring(Win_Buy,format.volume)

txt3_2 = str.tostring(Loss_Buy,format.volume)

txt4_2 = str.tostring((Win_Buy/Long_all)*100,format.percent)

txt5_2 = str.format("{0,number,#.##}", Factor_buy )

txt2_3 = str.tostring(Win_Sell,format.volume)

txt3_3 = str.tostring(Loss_Sell,format.volume)

txt4_3 = str.tostring((Win_Sell/Short_all)*100,format.percent)

txt5_3 = str.format("{0,number,#.##}", Factor_sell)

Factor_all_color = Factor_all > Factor_up ? Factor_up_color : Factor_all < Factor_donw ? Factor_donw_color : color.white

Factor_buy_color = Factor_buy > Factor_up ? Factor_up_color : Factor_buy < Factor_donw ? Factor_donw_color : color.white

Factor_sell_color = Factor_sell > Factor_up ? Factor_up_color : Factor_sell < Factor_donw ? Factor_donw_color : color.white

table.cell(Balane_status , 1 , 1 , txt1_1 , bgcolor = color.black , text_color = Factor_all_color )

table.cell(Balane_status , 2 , 1 , txt2_1 , bgcolor = color.black , text_color = Factor_all_color )

table.cell(Balane_status , 3 , 1 , txt3_1 , bgcolor = color.black , text_color = Factor_all_color )

table.cell(Balane_status , 4 , 1 , txt4_1 , bgcolor = color.black , text_color = Factor_all_color )

table.cell(Balane_status , 5 , 1 , txt5_1 , bgcolor = color.black , text_color = Factor_all_color )

table.cell(Balane_status , 1 , 2 , txt1_2 , bgcolor = color.black , text_color = Factor_buy_color )

table.cell(Balane_status , 2 , 2 , txt2_2 , bgcolor = color.black , text_color = Factor_buy_color )

table.cell(Balane_status , 3 , 2 , txt3_2 , bgcolor = color.black , text_color = Factor_buy_color )

table.cell(Balane_status , 4 , 2 , txt4_2 , bgcolor = color.black , text_color = Factor_buy_color )

table.cell(Balane_status , 5 , 2 , txt5_2 , bgcolor = color.black , text_color = Factor_buy_color )

table.cell(Balane_status , 1 , 3 , txt1_3 , bgcolor = color.black , text_color = Factor_sell_color )

table.cell(Balane_status , 2 , 3 , txt2_3 , bgcolor = color.black , text_color = Factor_sell_color )

table.cell(Balane_status , 3 , 3 , txt3_3 , bgcolor = color.black , text_color = Factor_sell_color )

table.cell(Balane_status , 4 , 3 , txt4_3 , bgcolor = color.black , text_color = Factor_sell_color )

table.cell(Balane_status , 5 , 3 , txt5_3 , bgcolor = color.black , text_color = Factor_sell_color )

table.cell(Balane_status , 0 , 1 , "Total" , bgcolor = color.black , text_color = color.white )

table.cell(Balane_status , 0 , 2 , "Long" , bgcolor = color.black , text_color = color.white )

table.cell(Balane_status , 0 , 3 , "Short" , bgcolor = color.black , text_color = color.white )

table.cell(Balane_status , 1 , 0 , "All" , bgcolor = color.black , text_color = color.white )

table.cell(Balane_status , 2 , 0 , "Win" , bgcolor = color.black , text_color = color.white )

table.cell(Balane_status , 3 , 0 , "Loss" , bgcolor = color.black , text_color = color.white )

table.cell(Balane_status , 4 , 0 , "Winrate" , bgcolor = color.black , text_color = color.white )

table.cell(Balane_status , 5 , 0 , "Profit\n\Factor" , bgcolor = color.black , text_color = color.white )