Elliott Wave Full Fractal System v2.0

ลิงก์ TradingView

คำอธิบาย

Elliott Wave Full Fractal System v2.0 – Q.C. FINAL (Guaranteed R/R)

Elliott Wave Full Fractal System is a multi-timeframe wave engine that automatically labels Elliott impulses and ABC corrections, then builds a rule-based, ATR-driven risk/reward framework around the “W3–W4–W5” leg.

“Guaranteed R/R” here means every order is placed with a predefined stop-loss and take-profit that respect a minimum Reward:Risk ratio – it does not mean guaranteed profits.

Core Idea

This strategy turns a full fractal Elliott Wave labelling engine into a systematic trading model.

It scans fractal pivots on three wave degrees (Primary, Intermediate, Minor) to detect 5-wave impulses and ABC corrections.

A separate “Trading Degree” pivot stream, filtered by a 200-EMA trend filter and ATR-based dynamic pivots, is then used to find W4 pullback entries with a minimum, user-defined Reward:Risk ratio.

Default Properties & Risk Assumptions

The backtest uses realistic but conservative defaults:

// Default properties used for backtesting

strategy(

"Elliott Wave Full Fractal System - Q.C. FINAL (Guaranteed R/R)",

overlay = true,

initial_capital = 10000, // realistic account size

default_qty_type = strategy.percent_of_equity,

default_qty_value = 1, // 1% risk per trade

commission_type = strategy.commission.cash_per_contract,

commission_value = 0.005, // example stock commission

slippage = 0 // see notes below

)

Account size: 10,000 (can be changed to match your own account).

Position sizing: 1% of equity per trade to keep risk per idea sustainable and aligned with TradingView’s recommendations.

Commission: 0.005 cash per contract/share as a realistic example for stock trading.

Slippage: set to 0 in code for clarity of “pure logic” backtesting. Real-life trading will experience slippage, so users should adjust this according to their market and broker.

Always re-run the backtest after changing any of these values, and avoid using high risk fractions (5–10%+) as that is rarely sustainable.

1. Full Fractal Wave Engine

The script builds and maintains four pivot streams using ATR-adaptive fractals:

Primary Degree (Macro Trend):

Captures the large swings that define the major trend. Labels ①–⑤ and ⒶⒷⒸ using blue “Circle” labels and thicker lines.

Intermediate Degree (Trading Degree):

Captures the medium swings (swing-trading horizon). Uses teal labels ( (1)…(5), (A)(B)(C) ).

Minor Degree (Micro Structure):

Tracks short-term swings inside the larger waves. Uses red roman numerals (i…v, a b c).

ABC Corrections (Optional):

When enabled, the engine tries to detect standard A–B–C corrective structures that follow a completed 5-wave impulse and plots them with dashed lines.

Each degree uses a dynamic pivot lookback that expands when ATR is above its EMA, so the system naturally requires “stronger” pivots in volatile environments and reacts faster in quiet conditions.

2. Theory Rules & Strict Mode

Normal Mode: More permissive detection. Designed to show more wave structures for educational / exploratory use.

Strict Mode: Enforces key Elliott constraints:

Wave 3 not shorter than waves 1 and 5.

No invalid W4 overlap with W1 (for standard impulses).

ABC Logic: After a confirmed bullish impulse, the script expects a down-up-down corrective pattern (A,B,C). After a bearish impulse, it looks for up-down-up.

3. Trend Filter & Pivots

EMA Trend Filter: A configurable EMA (default 200) is used as a non-wave trend filter.

Price above EMA → Only long setups are considered.

Price below EMA → Only short setups are considered.

ATR-Adaptive Pivots: The pivot engine scales its left/right bars based on current ATR vs ATR EMA, making waves and trading pivots more robust in volatile regimes.

4. Dynamic Risk Management (Guaranteed R/R Engine)

The trading engine is designed around risk, not just pattern recognition:

ATR-Based Stop:

Stop-loss is placed at:

Entry ± ATR × Multiplier (user-configurable, default 2.0).

This anchors risk to current volatility.

Minimum Reward:Risk Ratio:

For each setup, the script:

Computes the distance from entry to stop (risk).

Projects a take-profit target at risk × min_rr_ratio away from entry.

Only accepts the setup if risk is positive and the required R:R ratio is achievable.

Result: Every order is created with both TP and SL at a predefined distance, so each trade starts with a known, minimum Reward:Risk profile by design.

“Guaranteed R/R” refers exclusively to this order placement logic (TP/SL geometry), not to win-rate or profitability.

5. Trading Logic – W3–W4–W5 Pattern

The Trading pivot stream (separate from visual wave degrees) looks for a simple but powerful pattern:

Bullish structure:

Sequence of pivots forms a higher-high / higher-low pattern.

Price is above the EMA trend filter.

A strong “W3” leg is confirmed with structure rules (optionally stricter in Strict mode).

Entry (Long – W4 Pullback):

The “height” of W3 is measured.

Entry is placed at a configurable Fibonacci pullback (default 50%) inside that leg.

ATR-based stop is placed below entry.

Take-profit is projected to satisfy min Reward:Risk.

Bearish structure:

Mirrored logic (lower highs/lows, price below EMA, W3 down, W4 retrace up, W5 continuation down).

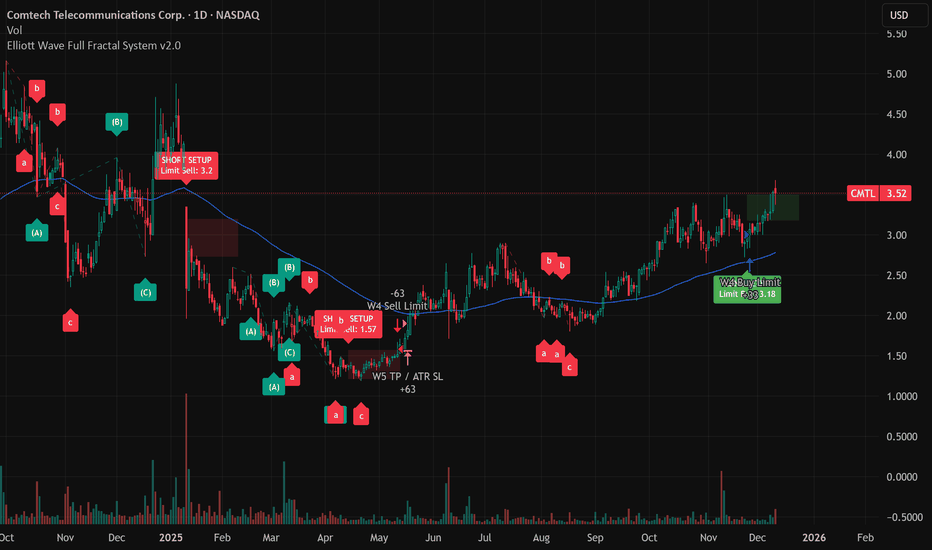

Once a valid setup is found, the script draws a colored box around the entry zone and a label describing the type of signal (“LONG SETUP” or “SHORT SETUP”) with the suggested limit price.

6. Orders & Execution

Entry Orders: The strategy uses limit orders at the computed W4 level (“Sniper Long” or “Sniper Short”).

Exits: A single strategy.exit() is attached to each entry with:

Take-profit at the projected minimum R:R target.

Stop-loss at ATR-based level.

One Trade at a Time: New setups are only used when there is no open position (strategy.opentrades == 0) to keep the logic clear and risk contained.

7. Visual Guide on the Chart

Wave Labels:

Primary: ①,②,③,④,⑤, ⒶⒷⒸ

Intermediate: (1)…(5), (A)(B)(C)

Minor: i…v, a b c

Trend EMA: Single blue EMA showing the dominant trend.

Setup Boxes:

Green transparent box → long entry zone.

Red transparent box → short entry zone.

Labels: “LONG SETUP / SHORT SETUP” labels mark the proposed limit entry with price.

8. How to Use This Strategy

Attach the strategy to your chart

Choose your market (stocks, indices, FX, crypto, futures, etc.) and timeframe (for example 1h, 4h, or Daily). Then add the strategy to the chart from your Scripts list.

Start with the default settings

Leave all inputs on their defaults first. This lets you see the “intended” behaviour and the exact properties used for the published backtest (account size, 1% risk, commission, etc.).

Study the wave map

Zoom in and out and look at the three wave degrees:

Blue circles → Primary degree (big picture trend).

Teal (1)…(5) → Intermediate degree (swing structure).

Red i…v → Minor degree (micro waves).

Use this to understand how the engine is interpreting the Elliott structure on your symbol.

Watch for valid setups

Look for the coloured boxes and labels:

Green box + “LONG SETUP” label → potential W4 pullback long in an uptrend.

Red box + “SHORT SETUP” label → potential W4 pullback short in a downtrend.

Only trades in the direction of the EMA trend filter are allowed by the strategy.

Check the Reward:Risk of each idea

For each setup, inspect:

Limit entry price.

ATR-based stop level.

Projected take-profit level.

Make sure the minimum Reward:Risk ratio matches your own rules before you consider trading it.

Backtest and evaluate

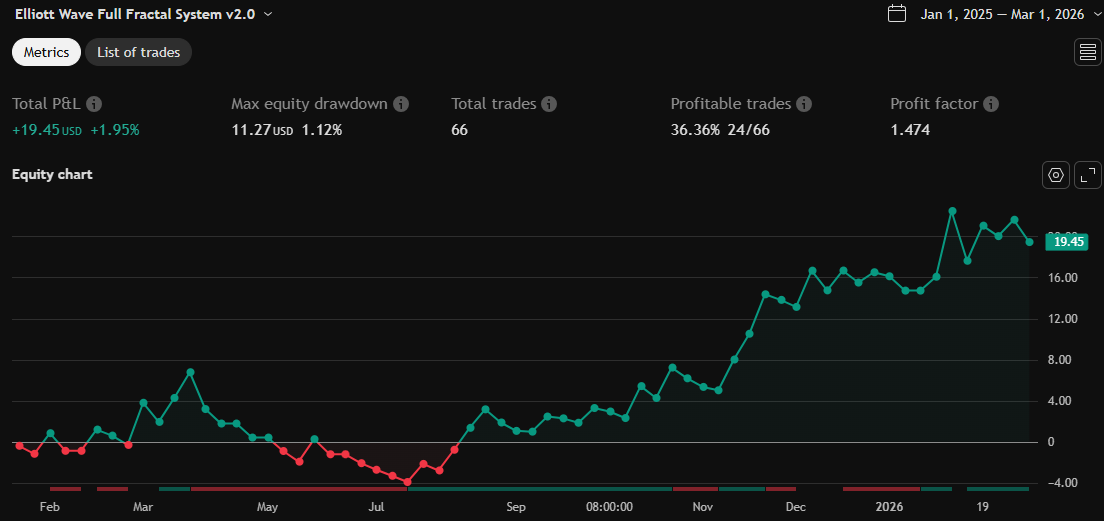

Open the Strategy Tester:

Verify you have a decent sample size (ideally 100+ trades).

Check drawdowns, average trade, win-rate and R:R distribution.

Change markets and timeframes to see where the logic behaves best.

Adapt to your own risk profile

If you plan to use it live:

Set Initial Capital to your real account size.

Adjust default_qty_value to a risk level you are comfortable with (often 0.5–2% per trade).

Set commission and slippage to realistic broker values.

Re-run the backtest after every major change.

Use as a framework, not a signal machine

Treat this as a structured Elliott/R:R framework:

Filter signals by higher-timeframe trend, major S/R, volume, or fundamentals.

Optionally hide some wave degrees or ABC labels if you want a cleaner chart.

Combine the system’s structure with your own trade management and discretion.

Best Practices & Limitations

This is an approximate Elliott Wave engine based on fractal pivots. It does not replace a full discretionary Elliott analysis.

All wave counts are algorithmic and can differ from a manual analyst’s interpretation.

Like any backtest, results depend heavily on:

Symbol and timeframe.

Sample size (more trades are better).

Realistic commission/slippage settings.

The 0-slippage default is chosen only to show the “raw logic”. In real markets, slippage can significantly impact performance.

No strategy wins all the time. Losing streaks and drawdowns will still occur even with a strict R:R framework.

Disclaimer

This script is for educational and research purposes only and does not constitute financial advice or a recommendation to buy or sell any security. Past performance, whether real or simulated, is not indicative of future results. Always test on multiple symbols/timeframes, use conservative risk, and consult your financial advisor before trading live capital.

รูป Preview

Pine Script Source

// This Pine Script® code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © mbedaiwi2

//@version=6

strategy(

"Elliott Wave Full Fractal System v2.0",

overlay = true,

max_labels_count = 500,

max_lines_count = 500,

max_boxes_count = 500,

initial_capital = 10000,

default_qty_type = strategy.percent_of_equity,

default_qty_value = 1,

commission_type = strategy.commission.cash_per_contract,

commission_value = 0.005,

slippage = 0

)

// 1. SETTINGS -------------------------------------------------------------

// 1.1 Wave degrees

grpCycle = "1. Primary Degree (Macro Trend)"

showPrimary = input.bool(true, "Show Primary Waves (1, 2...)", group = grpCycle)

lenPriL = input.int(21, "Primary Lookback Left", group = grpCycle)

lenPriR = input.int(21, "Primary Lookback Right", group = grpCycle)

grpInter = "2. Intermediate Degree (Trading Degree)"

showInter = input.bool(true, "Show Intermediate Waves ((1), (2)...)", group = grpInter)

lenIntL = input.int(5, "Intermediate Lookback Left", minval = 2, group = grpInter)

lenIntR = input.int(5, "Intermediate Lookback Right", minval = 2, group = grpInter)

grpMinor = "3. Minor Degree (Micro Structure)"

showMinor = input.bool(true, "Show Minor Waves (i, ii...)", group = grpMinor)

lenMinL = input.int(3, "Minor Lookback Left", group = grpMinor)

lenMinR = input.int(3, "Minor Lookback Right", group = grpMinor)

// 1.2 Rules

grpRules = "Theory Rules"

rule_Strict = input.bool(false, "Strict Rules (No Overlap, W3 Not Shortest)", group = grpRules)

showABC = input.bool(true, "Show ABC Corrections", group = grpRules)

// 1.3 Pivot / ATR

grpVol = "Pivot Dynamics"

atr_len = input.int(14, "ATR Lookback for Dynamic Pivots", group = grpVol)

// 1.4 EMA Trend Filter

grpFilter = "4. Trend Filter (Non-Wave)"

ema_len = input.int(200, "EMA Trend Filter Length", group = grpFilter)

ema_filter = ta.ema(close, ema_len)

plot(ema_filter, color = color.blue, title = "Trend EMA")

// 1.5 Dynamic Risk Management

grpRisk = "5. Dynamic Risk Management"

atr_stop_mult = input.float(2.0, "ATR Stop Multiplier (Stop = Entry +/- ATR*X)", minval = 1.0, step = 0.1, group = grpRisk)

min_rr_ratio = input.float(2.0, "Minimum Reward/Risk Ratio (TP Target)", minval = 1.5, step = 0.5, group = grpRisk)

// 1.6 Trading Settings

grpTrade = "STRATEGY SETTINGS"

trade_on = input.bool(true, "Active Trading Signals", group = grpTrade)

fib_entry = input.float(0.50, "W4 Entry Fib", minval = 0.2, maxval = 0.7, step = 0.02, group = grpTrade)

fib_target = input.float(1.618, "W5 Target Extension (Deprecated)", group = grpTrade)

// 2. GLOBAL ARRAYS & STATE (Unchanged)

var int[] pri_idx = array.new_int()

var float[] pri_prc = array.new_float()

var int[] pri_typ = array.new_int()

var int[] int_idx = array.new_int()

var float[] int_prc = array.new_float()

var int[] int_typ = array.new_int()

var int[] min_idx = array.new_int()

var float[] min_prc = array.new_float()

var int[] min_typ = array.new_int()

var int[] trd_idx = array.new_int()

var float[] trd_prc = array.new_float()

var int[] trd_typ = array.new_int()

var int[] lastIdxArr = array.new_int(3, 0)

var int[] lastW5IdxArr = array.new_int(3, 0)

var bool[] lastWasBullArr = array.new_bool(3, false)

// 3. HELPER FUNCTIONS ---------------------------------------------------------

// Visual Styles

f_get_style(_degree) =>

color waveColor = color.new(color.blue, 0)

string fmt = "Circle"

int w = 2

if _degree == "Primary"

waveColor := color.new(color.blue, 0)

fmt := "Circle"

w := 3

else if _degree == "Intermediate"

waveColor := color.new(color.teal, 0)

fmt := "Paren"

w := 2

else

waveColor := color.new(color.red, 0)

fmt := "Roman"

w := 1

[waveColor, fmt, w]

// Label Drawer

f_draw_wave(int _idx, float _price, int _count, bool _isBull, string _degree) =>

[cWave, fmt, wid] = f_get_style(_degree)

string txt = ""

if fmt == "Circle"

txt := _count == 1 ? "①" : _count == 2 ? "②" : _count == 3 ? "③" : _count == 4 ? "④" : _count == 5 ? "⑤" : _count == 11 ? "Ⓐ" : _count == 12 ? "Ⓑ" : _count == 13 ? "Ⓒ" : "?"

else if fmt == "Paren"

txt := _count == 1 ? "(1)" : _count == 2 ? "(2)" : _count == 3 ? "(3)" : _count == 4 ? "(4)" : _count == 5 ? "(5)" : _count == 11 ? "(A)" : _count == 12 ? "(B)" : _count == 13 ? "(C)" : "?"

else

txt := _count == 1 ? "i" : _count == 2 ? "ii" : _count == 3 ? "iii" : _count == 4 ? "iv" : _count == 5 ? "v" : _count == 11 ? "a" : _count == 12 ? "b" : _count == 13 ? "c" : "?"

label.new(

_idx, _price, txt, xloc = xloc.bar_index, yloc = _isBull ? yloc.abovebar : yloc.belowbar,

style = _isBull ? label.style_label_down : label.style_label_up, color = cWave, textcolor = color.white,

size = _degree == "Primary" ? size.normal : size.small)

// Utility: limit array size

f_trim_arrays(int[] idx, float[] prc, int[] typ, int maxSize) =>

while array.size(idx) > maxSize

array.shift(idx)

array.shift(prc)

array.shift(typ)

// Dynamic Pivot Updater

f_update_pivots(int _L, int _R, int[] idx, float[] prc, int[] typ) =>

float atrValue = ta.atr(atr_len)

float avgAtr = ta.ema(atrValue, 50)

int dynamic_L = math.round(_L * (atrValue > avgAtr ? 1.5 : 1.0))

int dynamic_R = math.round(_R * (atrValue > avgAtr ? 1.5 : 1.0))

dynamic_L := math.max(2, dynamic_L)

dynamic_R := math.max(2, dynamic_R)

float ph = ta.pivothigh(high, dynamic_L, dynamic_R)

float pl = ta.pivotlow(low, dynamic_L, dynamic_R)

if not na(ph)

array.push(idx, bar_index[dynamic_R])

array.push(prc, ph)

array.push(typ, 1)

if not na(pl)

array.push(idx, bar_index[dynamic_R])

array.push(prc, pl)

array.push(typ, -1)

f_trim_arrays(idx, prc, typ, 300)

// Visualization Engine for one degree

f_process_degree(string _degName, int _degIndex, bool _show, int[] idx, float[] prc, int[] typ) =>

if not _show

[0, 0, false]

else

int lastIdx = array.get(lastIdxArr, _degIndex)

int lastW5Idx = array.get(lastW5IdxArr, _degIndex)

bool lastWasBull = array.get(lastWasBullArr, _degIndex)

if array.size(idx) >= 6

int sz = array.size(idx)

int i0 = array.get(idx, sz - 6)

int i1 = array.get(idx, sz - 5)

int i2 = array.get(idx, sz - 4)

int i3 = array.get(idx, sz - 3)

int i4 = array.get(idx, sz - 2)

int i5 = array.get(idx, sz - 1)

float p0 = array.get(prc, sz - 6)

float p1 = array.get(prc, sz - 5)

float p2 = array.get(prc, sz - 4)

float p3 = array.get(prc, sz - 3)

float p4 = array.get(prc, sz - 2)

float p5 = array.get(prc, sz - 1)

int t0 = array.get(typ, sz - 6)

// ── IMPULSE WAVE DETECTION ───────────────────────────────────────

if i0 > lastIdx

// Bullish 5-wave

if t0 == -1 and p1 > p0 and p3 > p1 and p5 > p3 and p2 > p0 and p4 > p2

bool r3_gt_r1 = rule_Strict ? (math.abs(p3 - p2) > math.abs(p1 - p0)) : true

bool r4_no_overlap = rule_Strict ? (p4 > p1) : true

float len1 = math.abs(p1 - p0)

float len3 = math.abs(p3 - p2)

float len5 = math.abs(p5 - p4)

float min_len = math.min(len1, math.min(len3, len5))

bool r3_not_short = rule_Strict ? (len3 > min_len) : true

if r3_gt_r1 and r4_no_overlap and r3_not_short

lastIdx := i5

lastW5Idx := i5

lastWasBull := true

f_draw_wave(i1, p1, 1, true, _degName)

f_draw_wave(i2, p2, 2, true, _degName)

f_draw_wave(i3, p3, 3, true, _degName)

f_draw_wave(i4, p4, 4, true, _degName)

f_draw_wave(i5, p5, 5, true, _degName)

[c, _, w] = f_get_style(_degName)

line.new(i0, p0, i1, p1, color = c, width = w)

line.new(i1, p1, i2, p2, color = c, width = w)

line.new(i2, p2, i3, p3, color = c, width = w)

line.new(i3, p3, i4, p4, color = c, width = w)

line.new(i4, p4, i5, p5, color = c, width = w)

// Bearish 5-wave

else if t0 == 1 and p1 < p0 and p3 < p1 and p5 < p3 and p2 < p0 and p4 < p2

bool r3b_gt_r1b = rule_Strict ? (math.abs(p2 - p3) > math.abs(p0 - p1)) : true

bool r4b_no_overlap = rule_Strict ? (p4 < p1) : true

float len1b = math.abs(p0 - p1)

float len3b = math.abs(p2 - p3)

float len5b = math.abs(p4 - p5)

float min_lenb = math.min(len1b, math.min(len3b, len5b))

bool r3_not_short_b = rule_Strict ? (len3b > min_lenb) : true

if r3b_gt_r1b and r4b_no_overlap and r3_not_short_b

lastIdx := i5

lastW5Idx := i5

lastWasBull := false

f_draw_wave(i1, p1, 1, false, _degName)

f_draw_wave(i2, p2, 2, false, _degName)

f_draw_wave(i3, p3, 3, false, _degName)

f_draw_wave(i4, p4, 4, false, _degName)

f_draw_wave(i5, p5, 5, false, _degName)

[c, _, w] = f_get_style(_degName)

line.new(i0, p0, i1, p1, color = c, width = w)

line.new(i1, p1, i2, p2, color = c, width = w)

line.new(i2, p2, i3, p3, color = c, width = w)

line.new(i3, p3, i4, p4, color = c, width = w)

line.new(i4, p4, i5, p5, color = c, width = w)

// ── ABC CORRECTION DETECTION ─────────────────────────────────────

if showABC and lastW5Idx > 0 and i3 >= lastW5Idx

int ia = i3, ib = i4, ic = i5

float pa = p3, pb = p4, pc = p5

// After bullish impulse: look for down-up-down

if lastWasBull and p3 < p2

if pc < pa and pb < array.get(prc, sz - 4)

lastIdx := ic

f_draw_wave(ia, pa, 11, false, _degName) // A

f_draw_wave(ib, pb, 12, true, _degName) // B

f_draw_wave(ic, pc, 13, false, _degName) // C

[cA, _, _wA] = f_get_style(_degName)

line.new(i2, p2, ia, pa, color = color.new(cA, 50), width = 1, style = line.style_dashed)

line.new(ia, pa, ib, pb, color = color.new(cA, 50), width = 1, style = line.style_dashed)

line.new(ib, pb, ic, pc, color = color.new(cA, 50), width = 1, style = line.style_dashed)

// After bearish impulse: look for up-down-up

if not lastWasBull and p3 > p2

if pc > pa and pb > array.get(prc, sz - 4)

lastIdx := ic

f_draw_wave(ia, pa, 11, true, _degName) // A

f_draw_wave(ib, pb, 12, false, _degName) // B

f_draw_wave(ic, pc, 13, true, _degName) // C

[cB, _, _wB] = f_get_style(_degName)

line.new(i2, p2, ia, pa, color = color.new(cB, 50), width = 1, style = line.style_dashed)

line.new(ia, pa, ib, pb, color = color.new(cB, 50), width = 1, style = line.style_dashed)

line.new(ib, pb, ic, pc, color = color.new(cB, 50), width = 1, style = line.style_dashed)

// Save updated state back into arrays

array.set(lastIdxArr, _degIndex, lastIdx)

array.set(lastW5IdxArr, _degIndex, lastW5Idx)

array.set(lastWasBullArr, _degIndex, lastWasBull)

[lastIdx, lastW5Idx, lastWasBull]

// 4. UPDATE PIVOTS (once per bar) ---------------------------------------------

f_update_pivots(lenPriL, lenPriR, pri_idx, pri_prc, pri_typ)

f_update_pivots(lenIntL, lenIntR, int_idx, int_prc, int_typ)

f_update_pivots(lenMinL, lenMinR, min_idx, min_prc, min_typ)

f_update_pivots(lenIntL, lenIntR, trd_idx, trd_prc, trd_typ)

// 5. DRAW WAVES FOR EACH DEGREE -----------------------------------------------

f_process_degree("Primary", 0, showPrimary, pri_idx, pri_prc, pri_typ)

f_process_degree("Intermediate", 1, showInter, int_idx, int_prc, int_typ)

f_process_degree("Minor", 2, showMinor, min_idx, min_prc, min_typ)

// 6. TRADING ENGINE -----------------------------------------------------------

// Trade state

var int trade_lastW3 = 0

var int trade_dir = 0

var float trade_entry = na

var float trade_stop = na

var float trade_tp = na

// 6.1 Setup detection based on trading pivots

if trade_on and array.size(trd_idx) >= 4

int sz = array.size(trd_idx)

int i3 = array.get(trd_idx, sz - 1)

float p0 = array.get(trd_prc, sz - 4)

float p1 = array.get(trd_prc, sz - 3)

float p2 = array.get(trd_prc, sz - 2)

float p3 = array.get(trd_prc, sz - 1)

int t0 = array.get(trd_typ, sz - 4)

int t3 = array.get(trd_typ, sz - 1)

// **FIXED: ATR calculation moved here**

float current_atr = ta.atr(atr_len)

// Only react to a fresh pivot sequence

if i3 > trade_lastW3

bool is_bull_trend = close > ema_filter

bool is_bear_trend = close < ema_filter

// ── LONG SETUP

if t0 == -1 and t3 == 1 and is_bull_trend

bool isBullStruct = (p1 > p0) and (p2 > p0) and (p2 < p1) and (p3 > p1)

float len1 = math.abs(p1 - p0)

float len3 = math.abs(p3 - p2)

bool r3_gt1 = rule_Strict ? (len3 > len1) : true

if isBullStruct and r3_gt1

trade_lastW3 := i3

float w3_height = p3 - p2

float entryPrice = p3 - (w3_height * fib_entry)

float stopPrice = entryPrice - (current_atr * atr_stop_mult)

// Calculate TP to GUARANTEE min_rr_ratio

float risk_long = entryPrice - stopPrice

float tpPrice = entryPrice + (risk_long * min_rr_ratio)

// Check stop viability and ensure risk > 0

bool rr_ok = risk_long > 0

if entryPrice > stopPrice and rr_ok

trade_dir := 1

trade_entry := entryPrice

trade_stop := stopPrice

trade_tp := tpPrice

box.new(bar_index, p3, bar_index + 20, entryPrice, xloc = xloc.bar_index, bgcolor = color.new(color.green, 85), border_color = na)

label.new(bar_index, entryPrice, "LONG SETUP\nLimit Buy: " + str.tostring(entryPrice, "#.##"), xloc = xloc.bar_index, yloc = yloc.belowbar, style = label.style_label_up, color = color.green, textcolor = color.white, size = size.small)

// ── SHORT SETUP

else if t0 == 1 and t3 == -1 and is_bear_trend

bool isBearStruct = (p1 < p0) and (p2 < p0) and (p2 > p1) and (p3 < p1)

float len1b = math.abs(p0 - p1)

float len3b = math.abs(p2 - p3)

bool r3_gt1b = rule_Strict ? (len3b > len1b) : true

if isBearStruct and r3_gt1b

trade_lastW3 := i3

float w3_height = p2 - p3

float entryPrice = p3 + (w3_height * fib_entry)

float stopPrice = entryPrice + (current_atr * atr_stop_mult)

// Calculate TP to GUARANTEE min_rr_ratio

float risk_short = stopPrice - entryPrice

float tpPrice = entryPrice - (risk_short * min_rr_ratio)

// Check stop viability and ensure risk > 0

bool rr_ok = risk_short > 0

if entryPrice < stopPrice and rr_ok

trade_dir := -1

trade_entry := entryPrice

trade_stop := stopPrice

trade_tp := tpPrice

box.new(bar_index, p3, bar_index + 20, entryPrice, xloc = xloc.bar_index, bgcolor = color.new(color.red, 85), border_color = na)

label.new(bar_index, entryPrice, "SHORT SETUP\nLimit Sell: " + str.tostring(entryPrice, "#.##"), xloc = xloc.bar_index, yloc = yloc.abovebar, style = label.style_label_down, color = color.red, textcolor = color.white, size = size.small)

// 7. ORDER EXECUTION ----------------------------------------------------------

// Long execution

if trade_dir == 1 and strategy.opentrades == 0

strategy.order("Sniper Long", strategy.long, limit = trade_entry, comment = "W4 Buy Limit")

strategy.exit("TP/SL Long", "Sniper Long", limit = trade_tp, stop = trade_stop, comment = "W5 TP / ATR SL")

trade_dir := 0

trade_entry := na

trade_stop := na

trade_tp := na

// Short execution

if trade_dir == -1 and strategy.opentrades == 0

strategy.order("Sniper Short", strategy.short, limit = trade_entry, comment = "W4 Sell Limit")

strategy.exit("TP/SL Short", "Sniper Short", limit = trade_tp, stop = trade_stop, comment = "W5 TP / ATR SL")

trade_dir := 0

trade_entry := na

trade_stop := na

trade_tp := na