ETHModeStrategy2.2-5m -30m

ลิงก์ TradingView

คำอธิบาย

Open-source strategy for ETH.

Signals triggered on 5m chart with higher-timeframe context.

For personal automation use only.

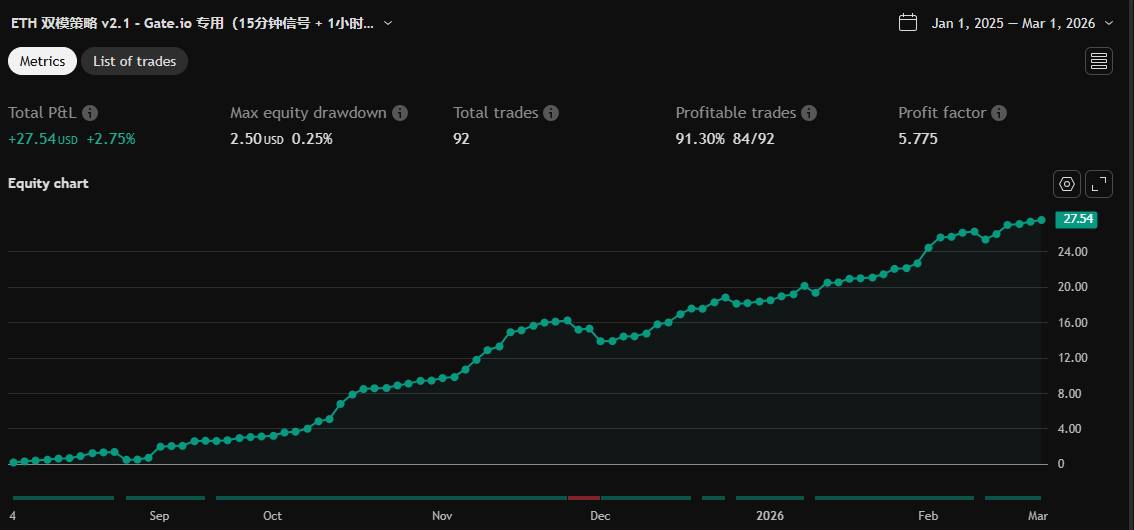

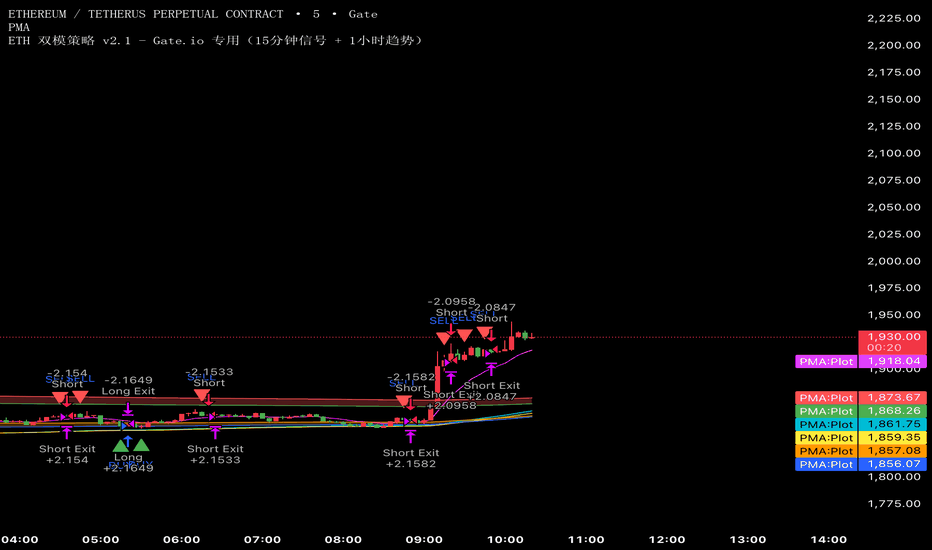

รูป Preview

Pine Script Source

//@version=5

// ⚠️ 注意:此策略默认启用移动止盈,请勿关闭以保证策略完整性

strategy("ETH 双模策略 v2.1 - Gate.io 专用(15分钟信号 + 1小时趋势)",

overlay=true,

default_qty_type=strategy.percent_of_equity,

default_qty_value=100,

initial_capital=10000,

commission_type=strategy.commission.percent,

commission_value=0.1,

margin_long=1.0,

margin_short=1.0)

// ====================== 参数设置 ======================

rsiLen = input.int(2, "CRSI - RSI周期")

streakLen = input.int(3, "CRSI - Streak周期")

prcLen = input.int(80, "CRSI - 百分位窗口")

crsiOversold = input.int(25, "CRSI 超卖阈值", minval=10, maxval=40, group="信号阈值")

crsiOverbought = input.int(75, "CRSI 超买阈值", minval=60, maxval=90, group="信号阈值")

keltnerLength = input.int(18, "Keltner EMA周期")

keltnerMult = input.float(1.5, "Keltner 乘数")

// 风控参数

useStopLoss = input.bool(true, "启用止损?", group="风控")

slAtrMult = input.float(2.2, "止损 ATR 倍数", minval=0.5, maxval=5.0, group="风控")

useTakeProfit = input.bool(true, "启用止盈?", group="风控")

tpRatio = input.float(2.5, "盈亏比 (TP/SL)", minval=0.5, maxval=5.0, group="风控")

useTrailingStop = input.bool(true, "启用移动止盈?", group="风控") // ✅ 默认开启!

trailActivationMult = input.float(1.5, "追踪激活倍数 (ATR)", minval=0.5, maxval=5.0, group="风控")

trailOffsetMult = input.float(1.0, "追踪回撤倍数 (ATR)", minval=0.5, maxval=3.0, group="风控")

minDistance = input.int(5, "最小信号间隔(K线数)", minval=1, group="风控")

minHoldBars = input.int(5, "最小持仓时间(K线数)", minval=1, group="风控")

// ====================== 时间框架 ======================

signalTf = "15" // ✅ 15分钟:信号生成周期

trendTf = "60" // ✅ 1小时:趋势判断周期

// ====================== CRSI 函数 ======================

crsiFunc() =>

rsi1 = ta.rsi(close, rsiLen)

streak = 0

streak := close > close[1] ? (streak[1] > 0 ? streak[1] + 1 : 1) :

close < close[1] ? (streak[1] < 0 ? streak[1] - 1 : -1) : 0

rsi2 = ta.rsi(streak, streakLen)

percentRank = ta.percentrank(close - close[1], prcLen)

(rsi1 + rsi2 + percentRank) / 3

// ====================== 多时间框架数据(基于15分钟)=======================

[crsi_15m, close_15m, open_15m, high_15m, low_15m, atr_15m, basis_15m] = request.security(syminfo.tickerid, signalTf, [crsiFunc(), close, open, high, low, ta.atr(10), ta.ema(close, keltnerLength)])

// 获取1小时CRSI用于趋势判断

crsi_1h = request.security(syminfo.tickerid, trendTf, crsiFunc())

// 判断是否为15分钟K线的收盘时刻

isSignalBar = ta.change(time(signalTf)) != 0

// ====================== 原始信号(纯净,无任何限制)=======================

inRange = crsi_1h >= 40 and crsi_1h <= 60

trendBull = crsi_1h > 60

trendBear = crsi_1h < 40

crsiOversoldSignal = crsi_15m <= crsiOversold

crsiOverboughtSignal = crsi_15m >= crsiOverbought

bullishCandle = close_15m > open_15m and (close_15m - open_15m) >= (high_15m - low_15m) * 0.3

bearishCandle = close_15m < open_15m and (open_15m - close_15m) >= (high_15m - low_15m) * 0.3

rangeBuy = inRange and (low_15m < basis_15m - keltnerMult * atr_15m) and crsiOversoldSignal and bullishCandle

rangeSell = inRange and (high_15m > basis_15m + keltnerMult * atr_15m) and crsiOverboughtSignal and bearishCandle

trendBuyPullback = trendBull and crsiOversoldSignal and (close_15m <= (basis_15m - keltnerMult * atr_15m) * 1.02)

trendSellPullback = trendBear and crsiOverboughtSignal and (close_15m >= (basis_15m + keltnerMult * atr_15m) * 0.98)

trendBuyBreakout = trendBull and (high_15m > (basis_15m + keltnerMult * atr_15m)[1]) and (close_15m < basis_15m + keltnerMult * atr_15m) and crsiOversoldSignal

trendSellBreakout = trendBear and (low_15m < (basis_15m - keltnerMult * atr_15m)[1]) and (close_15m > basis_15m - keltnerMult * atr_15m) and crsiOverboughtSignal

trendBuy = trendBuyPullback or trendBuyBreakout

trendSell = trendSellPullback or trendSellBreakout

// ✅【关键】原始信号:仅用于显示和警报,不受任何限制

rawBuySignal = isSignalBar and (rangeBuy or trendBuy)

rawSellSignal = isSignalBar and (rangeSell or trendSell)

// ====================== 可视化 & 警报 ======================

plotshape(rawBuySignal, title="Buy Signal", location=location.belowbar, color=color.green, style=shape.triangleup, text="BUY", size=size.small)

plotshape(rawSellSignal, title="Sell Signal", location=location.abovebar, color=color.red, style=shape.triangledown, text="SELL", size=size.small)

// ✅ 警报基于原始信号 → Gate.io 能收到每一个15分钟信号

alertcondition(rawBuySignal, title="ETH BUY", message="【ETH】15分钟买入信号!")

alertcondition(rawSellSignal, title="ETH SELL", message="【ETH】15分钟卖出信号!")

// ====================== 交易执行逻辑(带风控)=======================

var int lastTradeBar = na

var int longEntryBar = na

var int shortEntryBar = na

if isSignalBar

canTrade = na(lastTradeBar) or (bar_index - lastTradeBar >= minDistance)

// 开多

if rawBuySignal and canTrade

strategy.entry("Long", strategy.long)

lastTradeBar := bar_index

longEntryBar := bar_index

longStop = close_15m - slAtrMult * atr_15m

longTarget = close_15m + tpRatio * slAtrMult * atr_15m

if useStopLoss

strategy.exit("Long Exit", from_entry="Long",

stop=longStop,

limit=useTakeProfit ? longTarget : na,

trail_points=useTrailingStop ? trailActivationMult * atr_15m : na,

trail_offset=useTrailingStop ? trailOffsetMult * atr_15m : na)

// 开空

if rawSellSignal and canTrade

strategy.entry("Short", strategy.short)

lastTradeBar := bar_index

shortEntryBar := bar_index

shortStop = close_15m + slAtrMult * atr_15m

shortTarget = close_15m - tpRatio * slAtrMult * atr_15m

if useStopLoss

strategy.exit("Short Exit", from_entry="Short",

stop=shortStop,

limit=useTakeProfit ? shortTarget : na,

trail_points=useTrailingStop ? trailActivationMult * atr_15m : na,

trail_offset=useTrailingStop ? trailOffsetMult * atr_15m : na)

// 最小持仓保护

canCloseLong = not na(longEntryBar) and (bar_index - longEntryBar >= minHoldBars)

canCloseShort = not na(shortEntryBar) and (bar_index - shortEntryBar >= minHoldBars)

// 反向平仓(受最小持仓保护)

if isSignalBar

if rawSellSignal and canCloseLong

strategy.close("Long")

if rawBuySignal and canCloseShort

strategy.close("Short")