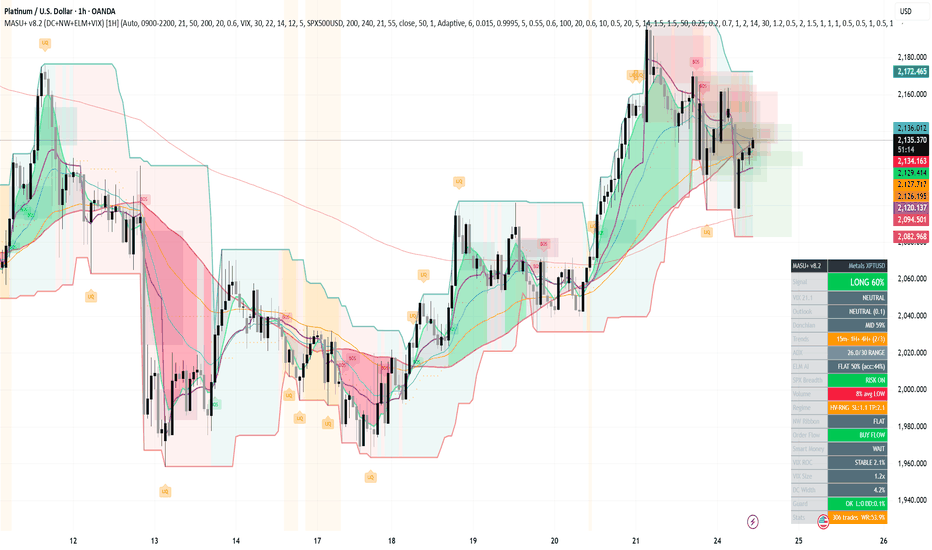

MASU+ v8.2 (DC+NW+ELM+VIX) [1H]

ลิงก์ TradingView

คำอธิบาย

# MASU+ Institutional v8.2 (DC+NW+ELM+VIX)

## Overview

MASU+ v8.2 is a multi-factor institutional-grade strategy that combines nine independent analytical components into a single weighted confluence framework. The system does not rely on any single indicator or pattern. Every entry requires agreement across trend structure, momentum, order flow, market microstructure, neural network prediction, channel position, volatility regime, and macro sentiment before a position is opened.

The strategy is designed for the 1H timeframe but functions on 15M through 4H. It supports equities, indices, forex, metals, crypto, energy, and commodities with automatic parameter adaptation per asset class.

---

## Core Architecture

The decision engine scores each trade opportunity on a weighted scale across all active components. A minimum confluence threshold must be met before any entry is permitted. Each component contributes independently, and the final score determines both the entry decision and the position size.

### 1. Nadaraya-Watson Kernel Ribbon (8 bands)

Eight Gaussian kernel regression lines with Fibonacci-spaced bandwidths (3, 5, 8, 13, 21, 34, 55, 89) form a non-parametric trend ribbon. Unlike moving averages, kernel regression provides statistically optimal smoothing without lag accumulation at longer periods.

The ribbon evaluates structural ordering: when 6 or more of 7 adjacent pairs are correctly sequenced (fast above slow for bullish, inverse for bearish), the trend filter passes. Bandwidth scaling adapts automatically to current volatility relative to its 50-period average, widening in volatile conditions and tightening in calm markets.

The slope of the fastest kernel line (NW1) serves as an additional confluence vote for directional momentum.

### 2. ELM Neural Filter (Online Learning)

An Extreme Learning Machine with 7 input features trains directly on the chart in real time:

- RSI (14) normalized

- Rate of Change (5-period)

- Distance from EMA 200 (%)

- ADX strength

- NW1 kernel slope

- NW ribbon ordering score

- Volume ratio to 20-bar average

The network outputs a probability (0.0 to 1.0) of the next N bars closing higher. Weights update on every confirmed bar using gradient descent with weight decay, creating continuous adaptation to changing market behavior.

A calibration system tracks rolling prediction accuracy and adjusts the effective weight of the ELM vote in the confluence score. If accuracy drops below 48%, the ELM contribution is automatically reduced toward zero. If accuracy exceeds 56%, the contribution is amplified up to 1.5x.

Position sizing optionally scales with signal quality: 7+ component agreement receives full allocation, 5-6 receives 80%, below 5 receives 60%.

### 3. VIX Fear and Greed Sentiment (New in v8.2)

The system pulls daily VIX data and classifies market sentiment into five regimes:

- Extreme Fear (VIX > 30): Position size reduced to 0.5x. Optional blocking of new long entries.

- Fear (VIX 22-30): Position size reduced to 0.75x. Confluence weight favors short direction.

- Neutral (VIX 14-22): Standard sizing. No directional bias from sentiment.

- Greed (VIX 12-14): Position size increased to 1.15x. Confluence weight favors long direction.

- Extreme Greed (VIX < 12): Position size increased to 1.3x. Strong long bias.

VIX momentum is tracked via 5-period rate of change. A spike above +5% ("Panic Spike") forces position sizing down to 0.7x regardless of the absolute VIX level. A drop below -5% ("Relief") signals improving conditions.

The system also evaluates VIX relative to its 20-day SMA. When VIX exceeds 120% of its own average, an additional bearish penalty is applied to the market prediction score.

These three inputs (level, momentum, relative position) are combined into a Market Prediction score ranging from -2.0 to +2.0, translated into a directional outlook: Bullish, Lean Bull, Neutral, Lean Bear, or Bearish. This outlook is displayed on the dashboard and included in alert messages.

### 4. Donchian Channel (Enhanced in v8.2)

A 20-period Donchian Channel provides three functions:

Trend Filter: Price above the channel midpoint permits long entries; below permits shorts. This single rule eliminates the majority of counter-trend entries.

Breakout Trigger: A confirmed close above the prior upper band or below the prior lower band generates a fourth entry type alongside trend, breakout, and mean-reversion triggers.

Squeeze Detection: When channel width (as a percentage of price) falls below 60% of its 50-period average, the system flags a squeeze condition. Historically, volatility contractions of this magnitude precede directional moves. The squeeze is highlighted with an orange background tint and displayed on the dashboard.

Channel position is calculated as a 0-100% scale (distance from lower to upper band) and classified into zones: BOT, LOWER, MID, UPPER, TOP. This provides immediate context for whether price is extended or has room to move.

Optional: Stop loss can be placed at the opposite channel boundary instead of ATR-based calculation.

### 5. Market Breadth (SPX Proxy)

Daily SPX500 close relative to its 200-period EMA serves as a risk-on/risk-off filter. When SPX trades above the 200 EMA, the system adds a confluence vote for long entries. Short entries are not penalized during risk-off conditions, as they align with the broader environment.

### 6. Multi-Timeframe Trend Filter

The 4H timeframe EMA 21/55 crossover and close position relative to EMA 21 must confirm the trade direction. This is weighted at 2.0x in the confluence system, making it the single most influential component. A trade that lacks higher-timeframe confirmation must compensate with strength across all other components.

### 7. Order Flow Analysis

Intraday VWAP is calculated from tick-level volume and price. Cumulative Volume Delta (CVD) tracks the running balance of buying versus selling pressure. The order flow filter requires either:

- CVD above its 20-period SMA and rising, with price above VWAP (bullish)

- CVD below its SMA and falling, with price below VWAP (bearish)

This ensures entries align with actual capital flow, not just price movement.

### 8. Smart Money Concepts

The system identifies and visualizes five institutional patterns:

Order Blocks: The last opposing candle before an impulsive move. Bullish OB (green box) marks institutional demand; bearish OB (red box) marks supply.

Fair Value Gaps: Three-candle price gaps exceeding 0.5x ATR where ranges do not overlap. These unfilled gaps act as magnets for price.

Liquidity Sweeps: Price briefly exceeds a key high or low but closes back inside, indicating stop-hunting by institutional participants. Marked with orange "LIQ" labels.

Break of Structure: A confirmed close beyond the last swing high (bullish BOS) or swing low (bearish BOS) signals trend continuation or reversal. Marked with green/red "BOS" labels.

Demand and Supply Zones: Areas of strong impulsive price action preceded by opposing candles. These zones persist until invalidated by price.

### 9. Volatility Regime Adaptation

ATR percentile rank over 100 periods classifies the current environment:

- High Volatility + Trending (HV-TR): SL 1.5 ATR, TP 2.5 ATR. Full parameters.

- High Volatility + Ranging (HV-RNG): SL 1.2 ATR, TP 1.8 ATR. Tighter targets.

- Low Volatility + Trending (LV-TR): SL 1.5 ATR, TP 2.5 ATR. Standard trend parameters.

- Low Volatility + Ranging (LV-RNG): SL 1.0 ATR, TP 1.5 ATR. Conservative.

This prevents the system from using trending-market stops in a range environment and vice versa.

---

## Entry Logic

Four trigger types generate entries:

1. Trend Following: EMA 21/50 crossover with ADX above threshold, price beyond EMA 200, and above-average volume.

2. Breakout: Close beyond 20-bar high/low with volume confirmation.

3. Mean Reversion: Price beyond Bollinger Bands with RSI reversal signal in ranging conditions.

4. Donchian Breakout: Close beyond prior Donchian upper/lower band with volume confirmation.

Every trigger must additionally pass all active filters: MTF trend, NW Kernel Ribbon, Order Flow, Smart Money, Donchian Channel trend, ELM neural, VIX sentiment, and minimum weighted confluence score.

---

## Exit Logic

Partial Take Profit: 50% of position closes at 1.5 ATR in profit. This locks in gains while allowing the remainder to capture extended moves.

Trailing Stop: Remaining position uses an adaptive trailing stop that activates after price moves 25% of the full TP distance. Trail offset is 0.2 ATR.

Hard Stop: Regime-adapted ATR-based stop loss. Optionally replaced by the opposite Donchian Channel boundary.

Asset-Adaptive Adverse Exit: Stocks use a tighter 0.7 ATR adverse threshold; other asset classes use 1.0 ATR.

---

## Risk Management

Equity Guard: Pauses trading after 5 consecutive losses or when drawdown exceeds 15% from peak equity. Resumes after a 50-bar cooldown period.

VIX-Adjusted Sizing: Position size scales from 0.5x (extreme fear) to 1.3x (extreme greed) based on real-time VIX classification. VIX panic spikes override to 0.7x regardless of level.

Quality-Based Sizing: Signal quality (confluence score relative to maximum possible) further adjusts position size from 0.6x to 1.0x.

---

## Asset Detection

The system automatically identifies the instrument type from the ticker name and adjusts behavior accordingly. Supported groups: Metals, Crypto, Indices, Energy, Forex, Stocks, Commodities. Manual override is available via dropdown.

---

## Dashboard

Two display modes: Full (20 rows) and Compact (12 rows). All information is color-coded:

- Signal direction with confidence percentage

- VIX level and sentiment classification

- Market prediction outlook with directional score

- Donchian position, zone, squeeze/expansion status

- Multi-timeframe trend alignment (15M, 1H, 4H)

- ADX with trend/range classification

- ELM AI prediction with rolling accuracy

- SPX breadth status

- Volume relative to average with spike/low warnings

- Volatility regime with current SL/TP multipliers

- NW Ribbon state and ordering count

- Order Flow direction

- Smart Money status with BOS alerts

- VIX momentum and size multiplier

- Equity guard status with loss count and drawdown

- Trade statistics with win rate

---

## Alert Format

Alerts include: direction, entry type (TREND/BRKOUT/MREV/DC), asset type, confidence percentage, ELM probability, VIX sentiment, market outlook, Donchian zone, and volatility regime.

Example: BUY XAUUSD | TREND | Metals | Conf:87% | AI:0.72 | VIX:NEUTRAL | LEAN BULL | DC:UPPER | HV-TR

---

## Configuration Notes

The strategy ships with defaults optimized for 1H charts. For other timeframes:

- 15M: Reduce Donchian period to 14. Consider lowering ADX threshold to 25.

- 4H: Increase Donchian period to 30. NW lookback can be reduced to 40.

- Daily: Increase Donchian period to 55. Disable time filter.

For crypto markets, disable the time filter (24/7 trading) and consider disabling market breadth (SPX correlation varies).

Commission is set at $7 per order and slippage at 2 ticks. Adjust these to match your broker.

---

## Disclaimer

This strategy is provided for educational and analytical purposes. Past performance in backtesting does not guarantee future results. Trading involves substantial risk of loss. Always use proper risk management and test thoroughly on a demo account before deploying capital.

Partnership Vector, LLC | BertTradeTech | Mark Novak

รูป Preview

Pine Script Source

//@version=6

strategy("MASU+ v8.2 (DC+NW+ELM+VIX) [1H]", overlay=true,

default_qty_type=strategy.percent_of_equity, default_qty_value=10,

pyramiding=0, calc_on_every_tick=true,

max_labels_count=500, max_lines_count=200, max_boxes_count=300,

commission_type=strategy.commission.cash_per_order, commission_value=7.0, slippage=2)

// ═══════════════════════════════════════════════════════════════════════════

// 1. SETTINGS

// ═══════════════════════════════════════════════════════════════════════════

// ASSET TYPE

asset_type_input = input.string("Auto", "Asset Type", options=["Auto", "Metals", "Stocks", "Crypto", "Indices", "Commodities", "Forex", "Energy"], group="Asset Detection",

tooltip="Auto: detect from ticker. Affects SL/TP and adverse exit.")

// TIME FILTER

use_time_filter = input.bool(true, "Trade Only During Session", group="Time Filter")

trading_session = input.session("0900-2200", "Trading Hours", group="Time Filter")

// TREND

trend_ema_fast = input.int(21, "Trend EMA Fast", minval=5, group="Trend")

trend_ema_slow = input.int(50, "Trend EMA Slow", minval=10, group="Trend")

trend_ema_filter = input.int(200, "Trend Filter EMA", minval=50, group="Trend")

// DONCHIAN CHANNEL (enhanced v8.2)

use_donchian = input.bool(true, "Enable Donchian Channel", group="Donchian Channel")

dc_length = input.int(20, "Donchian Period", minval=5, maxval=100, group="Donchian Channel",

tooltip="Standard: 20. Crypto: 14-20. Stocks: 20-55.")

dc_show = input.bool(true, "Show Donchian Lines", group="Donchian Channel")

dc_use_breakout = input.bool(true, "Use DC Breakout Signals", group="Donchian Channel")

dc_use_for_sl = input.bool(false, "Use DC for Stop Loss", group="Donchian Channel",

tooltip="SL = opposite channel band instead of ATR-based.")

dc_squeeze_mult = input.float(0.6, "Squeeze Threshold (x avg)", minval=0.3, maxval=0.9, step=0.1, group="Donchian Channel",

tooltip="Channel width below this fraction of average = squeeze alert.")

// VIX FEAR & GREED (NEW v8.2)

use_vix_sentiment = input.bool(true, "Enable VIX Sentiment", group="VIX Fear & Greed",

tooltip="v8.2: Uses VIX to gauge market fear/greed. Adjusts entry bias and position sizing.")

vix_symbol = input.symbol("CBOE:VIX", "VIX Symbol", group="VIX Fear & Greed")

vix_extreme_fear = input.float(30.0, "Extreme Fear (VIX >)", minval=20, maxval=50, step=1, group="VIX Fear & Greed")

vix_fear = input.float(22.0, "Fear (VIX >)", minval=15, maxval=40, step=1, group="VIX Fear & Greed")

vix_greed = input.float(14.0, "Greed (VIX <)", minval=8, maxval=20, step=1, group="VIX Fear & Greed")

vix_extreme_greed = input.float(12.0, "Extreme Greed (VIX <)", minval=5, maxval=15, step=1, group="VIX Fear & Greed")

vix_roc_period = input.int(5, "VIX ROC Period", minval=1, maxval=20, group="VIX Fear & Greed",

tooltip="Rate of change period for VIX momentum. Rising VIX = increasing fear.")

vix_use_as_filter = input.bool(false, "Block Entries on Extreme Fear", group="VIX Fear & Greed",

tooltip="When enabled, blocks new LONG entries when VIX > Extreme Fear threshold.")

vix_size_adjust = input.bool(true, "Adjust Position Size by Sentiment", group="VIX Fear & Greed",

tooltip="Reduce position size in fear, increase in greed. Max 1.3x in extreme greed, min 0.5x in extreme fear.")

show_vix_bg = input.bool(true, "Show VIX Background Tint", group="VIX Fear & Greed",

tooltip="Subtle background color: green = greed, red = fear.")

// MARKET BREADTH (SPX proxy)

use_market_breadth = input.bool(true, "Enable Market Breadth", group="Market Breadth",

tooltip="Uses SPX500 daily trend as risk-on/off proxy.")

mb_symbol = input.symbol("OANDA:SPX500USD", "Breadth Proxy Symbol", group="Market Breadth")

mb_ema_len = input.int(200, "Breadth EMA Length", minval=50, group="Market Breadth")

// MTF FILTER

use_mtf_filter = input.bool(true, "Use MTF Filter", group="MTF Filter")

mtf_timeframe = input.timeframe("240", "Higher Timeframe", group="MTF Filter")

mtf_ema_fast_len = input.int(21, "MTF EMA Fast", minval=5, group="MTF Filter")

mtf_ema_slow_len = input.int(55, "MTF EMA Slow", minval=10, group="MTF Filter")

// NW KERNEL RIBBON

use_nw_ribbon = input.bool(true, "Use NW Kernel Ribbon", group="NW Ribbon")

nw_src = input.source(close, "Source", group="NW Ribbon")

nw_lookback = input.int(50, "Lookback Window", minval=10, maxval=200, group="NW Ribbon")

nw_bw_scale = input.float(1.0, "Bandwidth Scale", minval=0.3, maxval=3.0, step=0.1, group="NW Ribbon")

nw_bw_mode = input.string("Adaptive", "Bandwidth Mode", options=["Fixed", "Adaptive"], group="NW Ribbon")

nw_ribbon_threshold = input.int(6, "Ribbon Threshold (of 7)", minval=4, maxval=7, group="NW Ribbon")

show_nw_ribbon = input.bool(true, "Show NW Ribbon", group="NW Ribbon")

// ELM NEURAL FILTER

use_elm = input.bool(true, "Enable ELM Filter", group="ELM Neural")

elm_lr = input.float(0.015, "Learning Rate", step=0.005, group="ELM Neural")

elm_weight_decay = input.float(0.9995, "Weight Decay", minval=0.990, maxval=1.0, step=0.0005, group="ELM Neural")

elm_target_bars = input.int(5, "Target Lookahead Bars", minval=1, maxval=20, group="ELM Neural")

elm_conf_soft = input.float(0.55, "Soft Confidence", step=0.05, group="ELM Neural")

elm_use_block = input.bool(false, "AI Can Block?", group="ELM Neural")

elm_conf_hard = input.float(0.60, "Block Threshold", step=0.05, group="ELM Neural")

elm_size_impact = input.bool(true, "Quality Affects Size", group="ELM Neural")

elm_use_calibration = input.bool(true, "Use Calibration", group="ELM Neural")

elm_calibration_window = input.int(100, "Calibration Window", minval=20, group="ELM Neural")

// ORDER FLOW

use_order_flow = input.bool(true, "Enable Order Flow", group="Order Flow")

show_vwap = input.bool(true, "Show VWAP", group="Order Flow")

cvd_length = input.int(20, "CVD Period", minval=1, group="Order Flow")

cvd_threshold = input.float(0.6, "CVD Threshold", minval=0.1, maxval=1.0, step=0.1, group="Order Flow")

// SMART MONEY

use_smc = input.bool(true, "Enable Smart Money", group="Smart Money")

show_order_blocks = input.bool(true, "Show Order Blocks", group="Smart Money")

show_fvg = input.bool(true, "Show FVG", group="Smart Money")

show_liquidity = input.bool(true, "Show Liquidity Sweeps", group="Smart Money")

show_bos = input.bool(true, "Show BOS/CHoCH", group="Smart Money")

ob_lookback = input.int(10, "OB Lookback", minval=5, group="Smart Money")

fvg_min_size = input.float(0.5, "FVG Min Size (ATR)", minval=0.1, step=0.1, group="Smart Money")

liquidity_lookback = input.int(20, "Liquidity Lookback", minval=10, group="Smart Money")

bos_pivot_length = input.int(5, "BOS Pivot Length", minval=3, group="Smart Money")

// RISK MANAGEMENT

atr_length = input.int(14, "ATR Period", minval=1, group="Risk")

base_sl_atr = input.float(1.5, "Base SL (ATR)", minval=0.5, step=0.1, group="Risk")

partial_tp_atr = input.float(1.5, "Partial TP (ATR)", minval=0.5, step=0.1, group="Risk",

tooltip="Close partial_tp_pct% at this ATR level. Remainder runs with trail.")

partial_tp_pct = input.float(50.0, "Partial TP %", minval=10, maxval=90, step=10, group="Risk")

use_trailing = input.bool(true, "Use Trailing Stop", group="Risk")

trail_activation_pct = input.float(0.25, "Trail Activation (% of TP)", minval=0.1, maxval=0.9, step=0.05, group="Risk")

trail_offset_atr = input.float(0.2, "Trail Offset (ATR)", minval=0.05, step=0.05, group="Risk")

adverse_stocks_atr = input.float(0.7, "Adverse Exit Stocks (ATR)", minval=0.3, step=0.1, group="Risk")

adverse_other_atr = input.float(1.0, "Adverse Exit Others (ATR)", minval=0.5, step=0.1, group="Risk")

hard_sl_atr = input.float(2.0, "Hard SL (ATR)", minval=1.0, step=0.1, group="Risk")

// FILTERS

adx_length = input.int(14, "ADX Period", minval=1, group="Filters")

adx_threshold = input.int(30, "ADX Min Threshold", minval=15, maxval=50, group="Filters")

volume_spike_mult = input.float(1.2, "Volume Spike Mult", minval=1.0, step=0.1, group="Filters")

volume_floor_pct = input.float(0.5, "Volume Floor (% of avg)", minval=0.1, maxval=1.0, step=0.1, group="Filters")

// CONFLUENCE WEIGHTS (v8.2: +VIX)

w_mtf = input.float(2.0, "W: MTF", minval=0, maxval=5, step=0.5, group="Weights")

w_ribbon = input.float(1.5, "W: NW Ribbon", minval=0, maxval=5, step=0.5, group="Weights")

w_elm = input.float(1.0, "W: ELM AI", minval=0, maxval=5, step=0.5, group="Weights")

w_of = input.float(1.0, "W: Order Flow", minval=0, maxval=5, step=0.5, group="Weights")

w_smc = input.float(1.0, "W: Smart Money", minval=0, maxval=5, step=0.5, group="Weights")

w_adx = input.float(0.5, "W: ADX Trend", minval=0, maxval=5, step=0.5, group="Weights")

w_slope = input.float(0.5, "W: NW Slope", minval=0, maxval=5, step=0.5, group="Weights")

w_donchian = input.float(1.0, "W: Donchian", minval=0, maxval=5, step=0.5, group="Weights")

w_breadth = input.float(0.5, "W: Market Breadth", minval=0, maxval=5, step=0.5, group="Weights")

w_vix = input.float(1.0, "W: VIX Sentiment", minval=0, maxval=5, step=0.5, group="Weights")

min_confluence = input.float(3.0, "Min Confluence to Enter", minval=0.5, maxval=15, step=0.5, group="Weights")

// ALERTS

alert_confidence_pct = input.float(85.0, "Alert at Confidence %", minval=50, maxval=100, step=5, group="Alerts")

// DISPLAY

showDashboard = input.bool(true, "Show Dashboard", group="Display")

show_sl_tp_lines = input.bool(true, "Show SL/TP Lines", group="Display")

dash_style = input.string("Full", "Dashboard Style", options=["Full", "Compact"], group="Display")

// VOLATILITY REGIME

use_vol_regime = input.bool(true, "Enable Vol Regime", group="Volatility")

atr_percentile_length = input.int(100, "ATR Percentile Period", minval=20, group="Volatility")

// EQUITY GUARD

use_equity_guard = input.bool(true, "Enable Equity Guard", group="Equity Guard")

max_consec_losses = input.int(5, "Max Consec Losses", minval=2, group="Equity Guard")

max_drawdown_pct = input.float(15.0, "Max DD % to Pause", minval=5, maxval=50, group="Equity Guard")

guard_cooldown_length = input.int(50, "Guard Cooldown (bars)", minval=10, group="Equity Guard")

// ═══════════════════════════════════════════════════════════════════════════

// 2. ASSET TYPE DETECTION (expanded v8.2)

// ═══════════════════════════════════════════════════════════════════════════

f_has(string src, string sub) => str.contains(str.upper(src), str.upper(sub))

f_detectAsset() =>

sym = str.upper(syminfo.ticker)

if asset_type_input != "Auto"

asset_type_input

else if f_has(sym,"XAU") or f_has(sym,"XAG") or f_has(sym,"XPT") or f_has(sym,"XPD") or f_has(sym,"GOLD") or f_has(sym,"SILVER") or f_has(sym,"GC1") or f_has(sym,"SI1")

"Metals"

else if f_has(sym,"BTC") or f_has(sym,"ETH") or f_has(sym,"SOL") or f_has(sym,"DOGE") or f_has(sym,"XRP") or f_has(sym,"AAVE") or f_has(sym,"ADA") or f_has(sym,"BNB") or f_has(sym,"AVAX") or f_has(sym,"DOT") or f_has(sym,"LINK") or f_has(sym,"SHIB") or f_has(sym,"LTC") or f_has(sym,"HBAR") or f_has(sym,"CELO") or f_has(sym,"KAS") or f_has(sym,"ETC") or f_has(sym,"NEAR") or f_has(sym,"ATOM") or syminfo.type == "crypto"

"Crypto"

else if f_has(sym,"NAS100") or f_has(sym,"US500") or f_has(sym,"US2000") or f_has(sym,"US30") or f_has(sym,"SPX") or f_has(sym,"NDX") or f_has(sym,"DAX") or f_has(sym,"DE40") or f_has(sym,"UK100") or f_has(sym,"FTSE") or f_has(sym,"EU50") or f_has(sym,"FR40") or f_has(sym,"JP225") or f_has(sym,"NIK") or syminfo.type == "index"

"Indices"

else if f_has(sym,"BCO") or f_has(sym,"WTICO") or f_has(sym,"NATGAS") or f_has(sym,"XCU") or f_has(sym,"CL1") or f_has(sym,"NG1") or f_has(sym,"USOIL") or f_has(sym,"UKOIL") or f_has(sym,"BRENT")

"Energy"

else if f_has(sym,"EUR") or f_has(sym,"GBP") or f_has(sym,"JPY") or f_has(sym,"CHF") or f_has(sym,"AUD") or f_has(sym,"NZD") or f_has(sym,"CAD") and syminfo.type == "forex"

"Forex"

else

"Stocks"

current_asset_type = f_detectAsset()

is_stocks = current_asset_type == "Stocks"

adverse_atr = is_stocks ? adverse_stocks_atr : adverse_other_atr

// ═══════════════════════════════════════════════════════════════════════════

// 3. CORE INDICATORS

// ═══════════════════════════════════════════════════════════════════════════

atr = ta.atr(atr_length)

ema_fast = ta.ema(close, trend_ema_fast)

ema_slow = ta.ema(close, trend_ema_slow)

ema_filter = ta.ema(close, trend_ema_filter)

[diPlus, diMinus, adx] = ta.dmi(adx_length, adx_length)

rsi = ta.rsi(close, 14)

volume_sma = ta.sma(volume, 20)

volume_spike = volume > volume_sma * volume_spike_mult

volume_floor_ok = volume_sma > 0 ? volume >= volume_sma * volume_floor_pct : true

bb_basis = ta.sma(close, 20)

bb_dev = 2.0 * ta.stdev(close, 20)

bb_upper = bb_basis + bb_dev

bb_lower = bb_basis - bb_dev

highest_high = ta.highest(high, 20)

lowest_low = ta.lowest(low, 20)

// ═══════════════════════════════════════════════════════════════════════════

// 4. DONCHIAN CHANNEL (enhanced v8.2)

// ═══════════════════════════════════════════════════════════════════════════

dc_upper = ta.highest(high, dc_length)

dc_lower = ta.lowest(low, dc_length)

dc_mid = (dc_upper + dc_lower) / 2.0

dc_width = dc_upper - dc_lower

dc_width_pct = dc_mid > 0 ? dc_width / dc_mid * 100 : 0

dc_width_avg = ta.sma(dc_width_pct, 50)

// Squeeze detection: channel narrower than threshold * average

dc_squeeze = dc_width_avg > 0 ? dc_width_pct < dc_width_avg * dc_squeeze_mult : false

dc_expanding = dc_width_pct > dc_width_pct[1] and dc_width_pct[1] > dc_width_pct[2]

// Donchian signals

dc_breakout_long = close > dc_upper[1] and close[1] <= dc_upper[2]

dc_breakout_short = close < dc_lower[1] and close[1] >= dc_lower[2]

dc_trend_long = close > dc_mid

dc_trend_short = close < dc_mid

dc_filter_long = not use_donchian or dc_trend_long

dc_filter_short = not use_donchian or dc_trend_short

// Position within channel (0 = bottom, 100 = top)

dc_position_pct = dc_width > 0 ? (close - dc_lower) / dc_width * 100 : 50

dc_zone = dc_position_pct >= 90 ? "TOP" : dc_position_pct >= 60 ? "UPPER" : dc_position_pct >= 40 ? "MID" : dc_position_pct >= 10 ? "LOWER" : "BOT"

// ═══════════════════════════════════════════════════════════════════════════

// 5. VIX FEAR & GREED SENTIMENT (NEW v8.2)

// ═══════════════════════════════════════════════════════════════════════════

vix_close = request.security(vix_symbol, "D", close, lookahead=barmerge.lookahead_off)

vix_high = request.security(vix_symbol, "D", ta.highest(close, 5), lookahead=barmerge.lookahead_off)

vix_low = request.security(vix_symbol, "D", ta.lowest(close, 5), lookahead=barmerge.lookahead_off)

vix_sma20 = request.security(vix_symbol, "D", ta.sma(close, 20), lookahead=barmerge.lookahead_off)

vix_roc = request.security(vix_symbol, "D", ta.roc(close, vix_roc_period), lookahead=barmerge.lookahead_off)

// Classify sentiment

vix_val = nz(vix_close, 18)

vix_sentiment = vix_val >= vix_extreme_fear ? 1 : vix_val >= vix_fear ? 2 : vix_val > vix_greed ? 3 : vix_val > vix_extreme_greed ? 4 : 5

// 1=Extreme Fear, 2=Fear, 3=Neutral, 4=Greed, 5=Extreme Greed

vix_label = vix_sentiment == 1 ? "EXTREME FEAR" : vix_sentiment == 2 ? "FEAR" : vix_sentiment == 3 ? "NEUTRAL" : vix_sentiment == 4 ? "GREED" : "EXTREME GREED"

// VIX momentum: rising VIX = panic building, falling VIX = calm returning

vix_roc_val = nz(vix_roc, 0)

vix_rising = vix_roc_val > 5 // VIX jumped 5%+ = panic spike

vix_falling = vix_roc_val < -5 // VIX dropping 5%+ = relief

vix_momentum = vix_rising ? "PANIC SPIKE" : vix_falling ? "RELIEF" : "STABLE"

// VIX relative to its 20-day SMA (overbought/oversold)

vix_above_sma = nz(vix_sma20, 18) > 0 ? vix_val / vix_sma20 : 1.0

vix_elevated = vix_above_sma > 1.2 // VIX 20%+ above its average = unusually fearful

// Market prediction score (-2 to +2)

// Negative = bearish outlook (high fear, rising VIX)

// Positive = bullish outlook (low fear, falling VIX)

vix_prediction = 0.0

vix_prediction += vix_sentiment == 5 ? 1.0 : vix_sentiment == 4 ? 0.5 : vix_sentiment == 3 ? 0.0 : vix_sentiment == 2 ? -0.5 : -1.0

vix_prediction += vix_falling ? 0.5 : vix_rising ? -0.5 : 0.0

vix_prediction += vix_elevated ? -0.5 : 0.0

// Translate prediction to market outlook

market_outlook = vix_prediction >= 1.0 ? "BULLISH" : vix_prediction >= 0.3 ? "LEAN BULL" : vix_prediction <= -1.0 ? "BEARISH" : vix_prediction <= -0.3 ? "LEAN BEAR" : "NEUTRAL"

// VIX-based position size multiplier

vix_size_mult = 1.0

if vix_size_adjust and use_vix_sentiment

vix_size_mult := vix_sentiment == 5 ? 1.3 : vix_sentiment == 4 ? 1.15 : vix_sentiment == 3 ? 1.0 : vix_sentiment == 2 ? 0.75 : 0.5

// Override: if VIX is spiking, always reduce

if vix_rising

vix_size_mult := math.min(vix_size_mult, 0.7)

// VIX filter for entries

vix_block_long = use_vix_sentiment and vix_use_as_filter and vix_sentiment == 1

// In extreme fear: block longs. Shorts are OK (contrarian requires caution).

// VIX confluence: adds weight for longs in greed, shorts in fear

vix_favors_long = use_vix_sentiment and (vix_sentiment >= 3 and not vix_rising)

vix_favors_short = use_vix_sentiment and (vix_sentiment <= 2 or vix_rising)

// ═══════════════════════════════════════════════════════════════════════════

// 6. MARKET BREADTH (SPX proxy)

// ═══════════════════════════════════════════════════════════════════════════

mb_close = request.security(mb_symbol, "D", close, lookahead=barmerge.lookahead_off)

mb_ema = request.security(mb_symbol, "D", ta.ema(close, mb_ema_len), lookahead=barmerge.lookahead_off)

market_risk_on = mb_close > mb_ema

mb_status = market_risk_on ? "RISK ON" : "RISK OFF"

mb_filter_long = not use_market_breadth or market_risk_on

mb_filter_short = not use_market_breadth or true

// ═══════════════════════════════════════════════════════════════════════════

// 7. NW KERNEL RIBBON

// ═══════════════════════════════════════════════════════════════════════════

f_nw_endpoint(float src, float h, int lookback) =>

float sum_w = 0.0

float sum_wy = 0.0

for i = 0 to lookback - 1

float u = float(i) / h

float w = math.exp(-0.5 * u * u)

sum_w += w

sum_wy += w * nz(src[i])

sum_w > 0 ? sum_wy / sum_w : src

atr_norm_pct = atr / close * 100

atr_norm_sma = ta.sma(atr_norm_pct, 50)

adaptive_scale = nw_bw_mode == "Adaptive" ? math.max(0.5, math.min(2.5, atr_norm_sma > 0 ? atr_norm_pct / atr_norm_sma : 1.0)) : 1.0

bw_scale = nw_bw_scale * adaptive_scale

nw1 = f_nw_endpoint(nw_src, 3.0 * bw_scale, nw_lookback)

nw2 = f_nw_endpoint(nw_src, 5.0 * bw_scale, nw_lookback)

nw3 = f_nw_endpoint(nw_src, 8.0 * bw_scale, nw_lookback)

nw4 = f_nw_endpoint(nw_src, 13.0 * bw_scale, nw_lookback)

nw5 = f_nw_endpoint(nw_src, 21.0 * bw_scale, nw_lookback)

nw6 = f_nw_endpoint(nw_src, 34.0 * bw_scale, nw_lookback)

nw7 = f_nw_endpoint(nw_src, 55.0 * bw_scale, nw_lookback)

nw8 = f_nw_endpoint(nw_src, 89.0 * bw_scale, nw_lookback)

nw_ordered_bull = (nw1>nw2?1:0) + (nw2>nw3?1:0) + (nw3>nw4?1:0) + (nw4>nw5?1:0) + (nw5>nw6?1:0) + (nw6>nw7?1:0) + (nw7>nw8?1:0)

nw_ordered_bear = (nw1<nw2?1:0) + (nw2<nw3?1:0) + (nw3<nw4?1:0) + (nw4<nw5?1:0) + (nw5<nw6?1:0) + (nw6<nw7?1:0) + (nw7<nw8?1:0)

nw_relaxed_bull = nw_ordered_bull >= nw_ribbon_threshold

nw_relaxed_bear = nw_ordered_bear >= nw_ribbon_threshold

ribbon_filter_long = not use_nw_ribbon or nw_relaxed_bull

ribbon_filter_short = not use_nw_ribbon or nw_relaxed_bear

nw1_slope = nw1 - nw1[1]

// ═══════════════════════════════════════════════════════════════════════════

// 8. ELM NEURAL FILTER

// ═══════════════════════════════════════════════════════════════════════════

f_norm(val, lo, hi) => math.max(math.min((val - lo) / (hi - lo), 1.0), 0.0)

ema200_elm = ta.ema(close, 200)

dist_ema200 = (close - ema200_elm) / close * 100

elm_f1 = nz(ta.rsi(close, 14) / 100.0, 0.5)

elm_f2 = f_norm(ta.roc(close, 5), -10, 10)

elm_f3 = f_norm(dist_ema200, -5, 5)

elm_f4 = f_norm(adx, 0, 60)

elm_f5 = f_norm(nw1 != 0 ? nw1_slope / nw1 * 1000 : 0, -5, 5)

elm_f6 = f_norm(nw_ordered_bull - nw_ordered_bear, -7, 7)

elm_f7 = volume_sma > 0 ? f_norm(volume / volume_sma, 0, 3) : 0.5

var float ew1=0.1, var float ew2=0.1, var float ew3=0.1, var float ew4=0.05

var float ew5=0.1, var float ew6=0.1, var float ew7=0.05, var float ew_bias=0.0

elm_target = close > close[elm_target_bars] ? 1.0 : 0.0

elm_prev_out = ew1*nz(elm_f1[elm_target_bars]) + ew2*nz(elm_f2[elm_target_bars]) + ew3*nz(elm_f3[elm_target_bars]) + ew4*nz(elm_f4[elm_target_bars]) + ew5*nz(elm_f5[elm_target_bars]) + ew6*nz(elm_f6[elm_target_bars]) + ew7*nz(elm_f7[elm_target_bars]) + ew_bias

elm_prev_prob = 1.0 / (1.0 + math.exp(-math.max(math.min(elm_prev_out, 10), -10)))

elm_error = elm_target - elm_prev_prob

if barstate.isconfirmed

ew1 := ew1 * elm_weight_decay + elm_lr * elm_error * nz(elm_f1[elm_target_bars])

ew2 := ew2 * elm_weight_decay + elm_lr * elm_error * nz(elm_f2[elm_target_bars])

ew3 := ew3 * elm_weight_decay + elm_lr * elm_error * nz(elm_f3[elm_target_bars])

ew4 := ew4 * elm_weight_decay + elm_lr * elm_error * nz(elm_f4[elm_target_bars])

ew5 := ew5 * elm_weight_decay + elm_lr * elm_error * nz(elm_f5[elm_target_bars])

ew6 := ew6 * elm_weight_decay + elm_lr * elm_error * nz(elm_f6[elm_target_bars])

ew7 := ew7 * elm_weight_decay + elm_lr * elm_error * nz(elm_f7[elm_target_bars])

ew_bias := ew_bias * elm_weight_decay + elm_lr * elm_error

elm_out = ew1*elm_f1 + ew2*elm_f2 + ew3*elm_f3 + ew4*elm_f4 + ew5*elm_f5 + ew6*elm_f6 + ew7*elm_f7 + ew_bias

elm_prob = 1.0 / (1.0 + math.exp(-math.max(math.min(elm_out, 10), -10)))

elm_clean = nz(elm_prob, 0.5)

var int elm_correct = 0, var int elm_total = 0, var float elm_accuracy = 0.5, var float elm_conf_weight = 1.0

if barstate.isconfirmed and bar_index > elm_target_bars + 10

float p = nz(elm_prob[elm_target_bars], 0.5)

bool ok = (p > 0.5) == (close > close[elm_target_bars])

elm_total += 1

if ok

elm_correct += 1

if elm_total > elm_calibration_window

elm_accuracy := elm_accuracy * 0.99 + (ok ? 0.01 : 0.0)

else

elm_accuracy := elm_total > 0 ? float(elm_correct) / float(elm_total) : 0.5

elm_conf_weight := elm_use_calibration ? math.max(0.0, math.min(1.5, (elm_accuracy - 0.48) / 0.08)) : 1.0

elm_vote_long = use_elm and elm_clean > elm_conf_soft

elm_vote_short = use_elm and elm_clean < (1.0 - elm_conf_soft)

elm_block_long = use_elm and elm_use_block and elm_clean < (1.0 - elm_conf_hard)

elm_block_short = use_elm and elm_use_block and elm_clean > elm_conf_hard

// ═══════════════════════════════════════════════════════════════════════════

// 9. MTF FILTER

// ═══════════════════════════════════════════════════════════════════════════

mtf_ema_f = request.security(syminfo.tickerid, mtf_timeframe, ta.ema(close, mtf_ema_fast_len), lookahead=barmerge.lookahead_off)

mtf_ema_s = request.security(syminfo.tickerid, mtf_timeframe, ta.ema(close, mtf_ema_slow_len), lookahead=barmerge.lookahead_off)

mtf_cl = request.security(syminfo.tickerid, mtf_timeframe, close, lookahead=barmerge.lookahead_off)

mtf_bull = mtf_ema_f > mtf_ema_s and mtf_cl > mtf_ema_f

mtf_bear = mtf_ema_f < mtf_ema_s and mtf_cl < mtf_ema_f

mtf_filter_long = not use_mtf_filter or mtf_bull

mtf_filter_short = not use_mtf_filter or mtf_bear

// ═══════════════════════════════════════════════════════════════════════════

// 10. VWAP & ORDER FLOW

// ═══════════════════════════════════════════════════════════════════════════

var float vwap_sum = 0.0, var float vol_sum = 0.0, var float vwap = 0.0

if barstate.isfirst or ta.change(time('D')) != 0

vwap_sum := 0.0

vol_sum := 0.0

vwap_sum += volume * hlc3

vol_sum += volume

vwap := vol_sum > 0 ? vwap_sum / vol_sum : close

buy_vol = close > open ? volume : 0.0

sell_vol = close < open ? volume : 0.0

delta = buy_vol - sell_vol

cvd = ta.cum(delta)

cvd_sma = ta.sma(cvd, cvd_length)

vol_ratio = buy_vol / math.max(sell_vol, 1)

of_bullish = use_order_flow and ((cvd > cvd_sma and cvd > cvd[1]) or vol_ratio > (1 + cvd_threshold)) and close > vwap

of_bearish = use_order_flow and ((cvd < cvd_sma and cvd < cvd[1]) or vol_ratio < (1 - cvd_threshold)) and close < vwap

of_filter_long = not use_order_flow or of_bullish or close > vwap

of_filter_short = not use_order_flow or of_bearish or close < vwap

// ═══════════════════════════════════════════════════════════════════════════

// 11. SMART MONEY CONCEPTS

// ═══════════════════════════════════════════════════════════════════════════

bullish_ob = close > open and close[1] < open[1] and high - close < (high - low) * 0.3

bearish_ob = close < open and close[1] > open[1] and close - low < (high - low) * 0.3

bullish_fvg = low > high[2] and (low - high[2]) > atr * fvg_min_size

bearish_fvg = high < low[2] and (low[2] - high) > atr * fvg_min_size

recent_high = ta.highest(high, liquidity_lookback)

recent_low = ta.lowest(low, liquidity_lookback)

liq_grab_high = high > recent_high[1] and close < open and close < recent_high[1]

liq_grab_low = low < recent_low[1] and close > open and close > recent_low[1]

swing_high = ta.pivothigh(high, bos_pivot_length, bos_pivot_length)

swing_low = ta.pivotlow(low, bos_pivot_length, bos_pivot_length)

var float last_sh = na, var float last_sl = na

if not na(swing_high)

last_sh := swing_high

if not na(swing_low)

last_sl := swing_low

bullish_bos = not na(last_sh) and close > last_sh and close[1] <= last_sh

bearish_bos = not na(last_sl) and close < last_sl and close[1] >= last_sl

smc_bullish = use_smc and (bullish_ob or bullish_fvg or liq_grab_low or bullish_bos)

smc_bearish = use_smc and (bearish_ob or bearish_fvg or liq_grab_high or bearish_bos)

smc_filter_long = not use_smc or smc_bullish or bullish_ob or bullish_fvg

smc_filter_short = not use_smc or smc_bearish or bearish_ob or bearish_fvg

// OB visualization

var box[] bull_ob_boxes = array.new_box()

var box[] bear_ob_boxes = array.new_box()

if barstate.isconfirmed and use_smc and show_order_blocks

if bullish_ob

array.push(bull_ob_boxes, box.new(bar_index-1, high[1], bar_index+15, low[1], border_color=color.new(color.green,100), bgcolor=color.new(color.green,90)))

if array.size(bull_ob_boxes) > 6

box.delete(array.shift(bull_ob_boxes))

if bearish_ob

array.push(bear_ob_boxes, box.new(bar_index-1, high[1], bar_index+15, low[1], border_color=color.new(color.red,100), bgcolor=color.new(color.red,90)))

if array.size(bear_ob_boxes) > 6

box.delete(array.shift(bear_ob_boxes))

var box[] fvg_bull = array.new_box()

var box[] fvg_bear = array.new_box()

if barstate.isconfirmed and use_smc and show_fvg

if bullish_fvg

array.push(fvg_bull, box.new(bar_index-2, low, bar_index+10, high[2], border_color=color.new(color.teal,100), bgcolor=color.new(color.teal,90)))

if array.size(fvg_bull) > 5

box.delete(array.shift(fvg_bull))

if bearish_fvg

array.push(fvg_bear, box.new(bar_index-2, low[2], bar_index+10, high, border_color=color.new(color.maroon,100), bgcolor=color.new(color.maroon,90)))

if array.size(fvg_bear) > 5

box.delete(array.shift(fvg_bear))

// ═══════════════════════════════════════════════════════════════════════════

// 12. VOLATILITY REGIME

// ═══════════════════════════════════════════════════════════════════════════

atr_pctrank = ta.percentrank(atr, atr_percentile_length)

high_vol = atr_pctrank > 70

low_vol = atr_pctrank < 30

is_trending = adx > adx_threshold

is_ranging = not is_trending

bullish_trend = ema_fast > ema_slow and close > ema_filter

bearish_trend = ema_fast < ema_slow and close < ema_filter

regime_state = high_vol and is_trending ? 1 : high_vol ? 2 : low_vol and is_trending ? 3 : is_trending ? 1 : 4

regime_sl = use_vol_regime ? (regime_state==1 ? 1.5 : regime_state==2 ? 1.2 : regime_state==3 ? 1.5 : 1.0) : base_sl_atr

regime_tp = use_vol_regime ? (regime_state==1 ? 2.5 : regime_state==2 ? 1.8 : regime_state==3 ? 2.5 : 1.5) : partial_tp_atr * 2.0

regime_label = regime_state==1 ? "HV-TR" : regime_state==2 ? "HV-RNG" : regime_state==3 ? "LV-TR" : "LV-RNG"

// ═══════════════════════════════════════════════════════════════════════════

// 13. EQUITY GUARD

// ═══════════════════════════════════════════════════════════════════════════

var int total_trades = 0, var int wins = 0

var float total_profit = 0.0, var float total_loss_val = 0.0

var int consec_losses = 0

var float peak_eq = strategy.initial_capital

var bool guard_active = false

var int guard_cd = 0

if strategy.closedtrades > total_trades

lp = strategy.closedtrades.profit(strategy.closedtrades - 1)

total_trades := strategy.closedtrades

if lp > 0

wins += 1

total_profit += lp

consec_losses := 0

else

total_loss_val += math.abs(lp)

consec_losses += 1

peak_eq := math.max(peak_eq, strategy.equity)

dd_pct = peak_eq > 0 ? (peak_eq - strategy.equity) / peak_eq * 100 : 0

if use_equity_guard

if consec_losses >= max_consec_losses or dd_pct >= max_drawdown_pct

if not guard_active

guard_cd := guard_cooldown_length

guard_active := true

if guard_active

guard_cd -= 1

if guard_cd <= 0

guard_active := false

if consec_losses < max_consec_losses and dd_pct < max_drawdown_pct

guard_active := false

// ═══════════════════════════════════════════════════════════════════════════

// 14. WEIGHTED CONFLUENCE (v8.2: +VIX weight)

// ═══════════════════════════════════════════════════════════════════════════

max_confl = w_mtf + w_ribbon + w_of + w_smc + w_adx + w_slope + w_elm + w_donchian + w_breadth + w_vix

elm_w_eff = w_elm * elm_conf_weight

ss_long = (mtf_filter_long ? w_mtf : 0) + (ribbon_filter_long ? w_ribbon : 0) + (of_filter_long ? w_of : 0) + (smc_filter_long ? w_smc : 0) + (is_trending ? w_adx : 0) + (elm_vote_long ? elm_w_eff : 0) + (nw1_slope > 0 ? w_slope : 0) + (dc_filter_long ? w_donchian : 0) + (mb_filter_long ? w_breadth : 0) + (vix_favors_long ? w_vix : 0)

ss_short = (mtf_filter_short ? w_mtf : 0) + (ribbon_filter_short ? w_ribbon : 0) + (of_filter_short ? w_of : 0) + (smc_filter_short ? w_smc : 0) + (is_trending ? w_adx : 0) + (elm_vote_short ? elm_w_eff : 0) + (nw1_slope < 0 ? w_slope : 0) + (dc_filter_short ? w_donchian : 0) + (mb_filter_short ? w_breadth : 0) + (vix_favors_short ? w_vix : 0)

conf_score = math.max(ss_long, ss_short)

conf_pct = max_confl > 0 ? conf_score / max_confl * 100 : 0

direction = ss_long > ss_short ? "LONG" : ss_short > ss_long ? "SHORT" : "WAIT"

alert_worthy = conf_pct >= alert_confidence_pct

// SL/TP

sl_long = dc_use_for_sl and use_donchian ? dc_lower : close - atr * regime_sl

tp_long = close + atr * regime_tp

sl_short = dc_use_for_sl and use_donchian ? dc_upper : close + atr * regime_sl

tp_short = close - atr * regime_tp

f_qmult(float q, float mx) =>

p = mx > 0 ? q / mx : 0.5

p >= 0.75 ? 1.0 : p >= 0.5 ? 0.8 : 0.6

// ═══════════════════════════════════════════════════════════════════════════

// 15. EXECUTION (v8.2: +VIX filter + VIX size adjust)

// ═══════════════════════════════════════════════════════════════════════════

in_session = not use_time_filter or not na(time(timeframe.period, trading_session))

ema_cross_up = ta.crossover(ema_fast, ema_slow)

ema_cross_down = ta.crossunder(ema_fast, ema_slow)

rsi_cross_up = ta.crossover(rsi, 30)

rsi_cross_down = ta.crossunder(rsi, 70)

trend_long = is_trending and bullish_trend and ema_cross_up and volume_spike and volume_floor_ok

trend_short = is_trending and bearish_trend and ema_cross_down and volume_spike and volume_floor_ok

breakout_long = close > highest_high[1] and volume_spike and volume_floor_ok and close > ema_filter

breakout_short = close < lowest_low[1] and volume_spike and volume_floor_ok and close < ema_filter

mean_rev_long = is_ranging and close < bb_lower and rsi < 30 and rsi_cross_up and volume_floor_ok

mean_rev_short = is_ranging and close > bb_upper and rsi > 70 and rsi_cross_down and volume_floor_ok

dc_long = use_donchian and dc_use_breakout and dc_breakout_long and volume_spike and volume_floor_ok and close > ema_filter

dc_short = use_donchian and dc_use_breakout and dc_breakout_short and volume_spike and volume_floor_ok and close < ema_filter

long_cond = (trend_long or breakout_long or mean_rev_long or dc_long) and mtf_filter_long and ribbon_filter_long and of_filter_long and smc_filter_long and dc_filter_long and not elm_block_long and not vix_block_long and in_session and ss_long >= min_confluence and not guard_active

short_cond = (trend_short or breakout_short or mean_rev_short or dc_short) and mtf_filter_short and ribbon_filter_short and of_filter_short and smc_filter_short and dc_filter_short and not elm_block_short and in_session and ss_short >= min_confluence and not guard_active

// Entry type for alerts

entry_type_long = trend_long ? "TREND" : breakout_long ? "BRKOUT" : mean_rev_long ? "MREV" : dc_long ? "DC" : "MIXED"

entry_type_short = trend_short ? "TREND" : breakout_short ? "BRKOUT" : mean_rev_short ? "MREV" : dc_short ? "DC" : "MIXED"

if long_cond and strategy.position_size == 0

qm = elm_size_impact ? f_qmult(ss_long, max_confl) : 1.0

final_size = strategy.equity * 0.10 * qm * vix_size_mult / close

strategy.entry("Long", strategy.long, qty=final_size)

strategy.exit("PartialL", "Long", qty_percent=partial_tp_pct, limit=close + atr * partial_tp_atr, stop=sl_long)

if use_trailing

tp_dist = atr * regime_tp

act_ticks = math.round(tp_dist * trail_activation_pct / syminfo.mintick)

off_ticks = math.round(atr * trail_offset_atr / syminfo.mintick)

strategy.exit("TrailL", "Long", stop=sl_long, trail_points=act_ticks, trail_offset=off_ticks)

else

strategy.exit("ExitL", "Long", stop=sl_long, limit=tp_long)

if alert_worthy

alert("BUY " + syminfo.ticker + " | " + entry_type_long + " | " + current_asset_type + " | Conf:" + str.tostring(conf_pct, "#") + "% | AI:" + str.tostring(elm_clean, "#.2") + " | VIX:" + vix_label + " | " + market_outlook + " | DC:" + dc_zone + " | " + regime_label, alert.freq_once_per_bar_close)

if short_cond and strategy.position_size == 0

qm = elm_size_impact ? f_qmult(ss_short, max_confl) : 1.0

final_size = strategy.equity * 0.10 * qm * vix_size_mult / close

strategy.entry("Short", strategy.short, qty=final_size)

strategy.exit("PartialS", "Short", qty_percent=partial_tp_pct, limit=close - atr * partial_tp_atr, stop=sl_short)

if use_trailing

tp_dist = atr * regime_tp

act_ticks = math.round(tp_dist * trail_activation_pct / syminfo.mintick)

off_ticks = math.round(atr * trail_offset_atr / syminfo.mintick)

strategy.exit("TrailS", "Short", stop=sl_short, trail_points=act_ticks, trail_offset=off_ticks)

else

strategy.exit("ExitS", "Short", stop=sl_short, limit=tp_short)

if alert_worthy

alert("SELL " + syminfo.ticker + " | " + entry_type_short + " | " + current_asset_type + " | Conf:" + str.tostring(conf_pct, "#") + "% | AI:" + str.tostring(elm_clean, "#.2") + " | VIX:" + vix_label + " | " + market_outlook + " | DC:" + dc_zone + " | " + regime_label, alert.freq_once_per_bar_close)

// ═══════════════════════════════════════════════════════════════════════════

// 16. VISUALIZATION

// ═══════════════════════════════════════════════════════════════════════════

// EMAs

plot(ema_fast, "EMA 21", color=#42A5F5, linewidth=1)

plot(ema_slow, "EMA 50", color=#FFA726, linewidth=1)

plot(ema_filter, "EMA 200", color=color.new(#EF5350, 50), linewidth=1)

// Donchian Channel (enhanced with fill)

p_dc_up = plot(dc_show and use_donchian ? dc_upper : na, "DC Upper", color=color.new(#26A69A, 40), linewidth=2)

p_dc_lo = plot(dc_show and use_donchian ? dc_lower : na, "DC Lower", color=color.new(#EF5350, 40), linewidth=2)

plot(dc_show and use_donchian ? dc_mid : na, "DC Mid", color=color.new(#FF9800, 50), linewidth=1, style=plot.style_cross)

dc_fill_color = dc_squeeze ? color.new(#FF9800, 85) : dc_trend_long ? color.new(#26A69A, 92) : color.new(#EF5350, 92)

fill(p_dc_up, p_dc_lo, color=dc_show and use_donchian ? dc_fill_color : na, title="DC Fill")

// NW Ribbon

nw_c = nw_relaxed_bull ? color.new(#00C853, 70) : nw_relaxed_bear ? color.new(#FF1744, 70) : color.new(color.gray, 85)

p1 = plot(show_nw_ribbon ? nw1 : na, "NW1", color=color.new(#00E676, 40), linewidth=2)

p8 = plot(show_nw_ribbon ? nw8 : na, "NW8", color=color.new(#E53935, 40), linewidth=2)

fill(p1, p8, color=show_nw_ribbon ? nw_c : na)

// VWAP

plot(show_vwap ? vwap : na, "VWAP", color=#AB47BC, linewidth=2)

// VIX background tint

vix_bg = vix_sentiment == 1 ? color.new(#B71C1C, 95) : vix_sentiment == 2 ? color.new(#E53935, 96) : vix_sentiment == 4 ? color.new(#43A047, 96) : vix_sentiment == 5 ? color.new(#1B5E20, 95) : na

bgcolor(show_vix_bg and use_vix_sentiment ? vix_bg : na, title="VIX Sentiment BG")

// Squeeze highlight

bgcolor(dc_squeeze and use_donchian ? color.new(#FF9800, 94) : na, title="DC Squeeze BG")

// Entry signals

plotshape(long_cond and barstate.isconfirmed, "BUY", shape.triangleup, location.belowbar, #00E676, size=size.small)

plotshape(short_cond and barstate.isconfirmed, "SELL", shape.triangledown, location.abovebar, #FF1744, size=size.small)

// Entry labels

if long_cond and barstate.isconfirmed

label.new(bar_index, low - atr*0.5, "BUY " + str.tostring(conf_pct,"#") + "%\n" + entry_type_long + " " + current_asset_type + "\nVIX:" + vix_label, color=color.new(#00C853,50), textcolor=color.white, style=label.style_label_up, size=size.small)

if short_cond and barstate.isconfirmed

label.new(bar_index, high + atr*0.5, "SELL " + str.tostring(conf_pct,"#") + "%\n" + entry_type_short + " " + current_asset_type + "\nVIX:" + vix_label, color=color.new(#FF1744,50), textcolor=color.white, style=label.style_label_down, size=size.small)

// SMC labels

if show_liquidity and use_smc and barstate.isconfirmed

if liq_grab_high

label.new(bar_index, high + atr*0.3, "LIQ", color=color.new(#FF9800,70), textcolor=#FF9800, style=label.style_label_down, size=size.tiny)

if liq_grab_low

label.new(bar_index, low - atr*0.3, "LIQ", color=color.new(#FF9800,70), textcolor=#FF9800, style=label.style_label_up, size=size.tiny)

if show_bos and use_smc and barstate.isconfirmed

if bullish_bos

label.new(bar_index, low - atr*0.15, "BOS", color=color.new(#00C853,85), textcolor=#00C853, style=label.style_label_up, size=size.tiny)

if bearish_bos

label.new(bar_index, high + atr*0.15, "BOS", color=color.new(#FF1744,85), textcolor=#FF1744, style=label.style_label_down, size=size.tiny)

// SL/TP lines

var line sl_line = na, var line tp_line = na, var line partial_line = na

var label sl_lbl = na, var label tp_lbl = na, var label partial_lbl = na

if barstate.islast and strategy.position_size != 0 and show_sl_tp_lines

line.delete(sl_line)

line.delete(tp_line)

line.delete(partial_line)

label.delete(sl_lbl)

label.delete(tp_lbl)

label.delete(partial_lbl)

float d_sl = strategy.position_size > 0 ? sl_long : sl_short

float d_tp = strategy.position_size > 0 ? tp_long : tp_short

float d_partial = strategy.position_size > 0 ? close + atr * partial_tp_atr : close - atr * partial_tp_atr

sl_line := line.new(bar_index-20, d_sl, bar_index+10, d_sl, color=#EF5350, width=2, style=line.style_dashed)

tp_line := line.new(bar_index-20, d_tp, bar_index+10, d_tp, color=#00C853, width=2, style=line.style_dashed)

partial_line := line.new(bar_index-20, d_partial, bar_index+10, d_partial, color=color.new(#FF9800,30), width=1, style=line.style_dotted)

sl_lbl := label.new(bar_index+11, d_sl, "SL " + str.tostring(d_sl, format.mintick), color=color.new(#EF5350,80), textcolor=#EF5350, style=label.style_label_left, size=size.tiny)

tp_lbl := label.new(bar_index+11, d_tp, "TP " + str.tostring(d_tp, format.mintick), color=color.new(#00C853,80), textcolor=#00C853, style=label.style_label_left, size=size.tiny)

partial_lbl := label.new(bar_index+11, d_partial, str.tostring(partial_tp_pct,"#") + "% TP", color=color.new(#FF9800,80), textcolor=#FF9800, style=label.style_label_left, size=size.tiny)

// ═══════════════════════════════════════════════════════════════════════════

// 17. DASHBOARD (v8.2: redesigned, cleaner, with VIX + Donchian + prediction)

// ═══════════════════════════════════════════════════════════════════════════

mtf_15m_up = request.security(syminfo.tickerid, "15", ta.ema(close,21) > ta.ema(close,50), lookahead=barmerge.lookahead_off)

mtf_1h_up = request.security(syminfo.tickerid, "60", ta.ema(close,21) > ta.ema(close,50), lookahead=barmerge.lookahead_off)

mtf_4h_up = request.security(syminfo.tickerid, "240", ta.ema(close,21) > ta.ema(close,50), lookahead=barmerge.lookahead_off)

trend_align = (mtf_15m_up ? 1 : 0) + (mtf_1h_up ? 1 : 0) + (mtf_4h_up ? 1 : 0)

if showDashboard

int rows = dash_style == "Full" ? 20 : 12

var table db = table.new(position.bottom_right, 2, rows, border_width=1, border_color=color.new(#37474F, 60))

if barstate.islast

sz = size.small

bg_h = color.new(#0D1B2A, 10)

bg_r = color.new(#1B2838, 85)

int r = 0

// ── HEADER ──

table.cell(db, 0, r, "MASU+ v8.2", text_color=#E0E0E0, bgcolor=bg_h, text_size=sz, text_halign=text.align_left)

table.cell(db, 1, r, current_asset_type + " " + syminfo.ticker, text_color=#90CAF9, bgcolor=bg_h, text_size=sz, text_halign=text.align_right)

r += 1

// ── DIRECTION + CONFIDENCE ──

dir_bg = direction == "LONG" ? #00C853 : direction == "SHORT" ? #FF1744 : #546E7A

table.cell(db, 0, r, "Signal", text_color=#B0BEC5, bgcolor=bg_r, text_size=sz, text_halign=text.align_left)

table.cell(db, 1, r, direction + " " + str.tostring(conf_pct, "#") + "%", text_color=color.white, bgcolor=dir_bg, text_size=size.normal, text_halign=text.align_right)

r += 1

// ── VIX SENTIMENT (NEW) ──

vix_bg_d = vix_sentiment == 1 ? #B71C1C : vix_sentiment == 2 ? #D32F2F : vix_sentiment == 3 ? #546E7A : vix_sentiment == 4 ? #2E7D32 : #1B5E20

table.cell(db, 0, r, "VIX " + str.tostring(vix_val, "#.1"), text_color=#B0BEC5, bgcolor=bg_r, text_size=sz, text_halign=text.align_left)

table.cell(db, 1, r, vix_label + (vix_rising ? " ^" : vix_falling ? " v" : ""), text_color=color.white, bgcolor=vix_bg_d, text_size=sz, text_halign=text.align_right)

r += 1

// ── MARKET PREDICTION (NEW) ──

pred_bg = vix_prediction >= 1.0 ? #00C853 : vix_prediction >= 0.3 ? #66BB6A : vix_prediction <= -1.0 ? #FF1744 : vix_prediction <= -0.3 ? #EF5350 : #546E7A

table.cell(db, 0, r, "Outlook", text_color=#B0BEC5, bgcolor=bg_r, text_size=sz, text_halign=text.align_left)

table.cell(db, 1, r, market_outlook + " (" + str.tostring(vix_prediction, "#.1") + ")", text_color=color.white, bgcolor=pred_bg, text_size=sz, text_halign=text.align_right)

r += 1

// ── DONCHIAN (enhanced) ──

dc_bg_d = dc_squeeze ? #FF9800 : dc_zone == "TOP" ? #00C853 : dc_zone == "BOT" ? #FF1744 : dc_zone == "UPPER" ? color.new(#00C853, 40) : dc_zone == "LOWER" ? color.new(#FF1744, 40) : #546E7A

dc_text = dc_zone + " " + str.tostring(dc_position_pct, "#") + "%" + (dc_squeeze ? " SQZ" : dc_expanding ? " EXP" : "")

table.cell(db, 0, r, "Donchian", text_color=#B0BEC5, bgcolor=bg_r, text_size=sz, text_halign=text.align_left)

table.cell(db, 1, r, dc_text, text_color=color.white, bgcolor=dc_bg_d, text_size=sz, text_halign=text.align_right)

r += 1

// ── TRENDS ──

t_text = (mtf_15m_up ? "15m+" : "15m-") + " " + (mtf_1h_up ? "1H+" : "1H-") + " " + (mtf_4h_up ? "4H+" : "4H-")

t_bg = trend_align == 3 ? #00C853 : trend_align == 0 ? #FF1744 : #FF9800

table.cell(db, 0, r, "Trends", text_color=#B0BEC5, bgcolor=bg_r, text_size=sz, text_halign=text.align_left)

table.cell(db, 1, r, t_text + " (" + str.tostring(trend_align) + "/3)", text_color=color.white, bgcolor=t_bg, text_size=sz, text_halign=text.align_right)

r += 1

// ── ADX ──

table.cell(db, 0, r, "ADX", text_color=#B0BEC5, bgcolor=bg_r, text_size=sz, text_halign=text.align_left)

table.cell(db, 1, r, str.tostring(adx, "#.0") + "/" + str.tostring(adx_threshold) + (is_trending ? " TREND" : " RANGE"), text_color=color.white, bgcolor=is_trending ? #00C853 : #78909C, text_size=sz, text_halign=text.align_right)

r += 1

// ── ELM AI ──

table.cell(db, 0, r, "ELM AI", text_color=#B0BEC5, bgcolor=bg_r, text_size=sz, text_halign=text.align_left)

elm_dir = elm_vote_long ? "BULL" : elm_vote_short ? "BEAR" : "FLAT"

elm_bg = elm_vote_long ? #00C853 : elm_vote_short ? #FF1744 : #546E7A

table.cell(db, 1, r, elm_dir + " " + str.tostring(elm_clean*100, "#") + "% (acc:" + str.tostring(elm_accuracy*100, "#") + "%)", text_color=color.white, bgcolor=elm_bg, text_size=sz, text_halign=text.align_right)

r += 1

// ── MARKET BREADTH ──

table.cell(db, 0, r, "SPX Breadth", text_color=#B0BEC5, bgcolor=bg_r, text_size=sz, text_halign=text.align_left)

table.cell(db, 1, r, mb_status, text_color=color.white, bgcolor=market_risk_on ? #00C853 : #FF1744, text_size=sz, text_halign=text.align_right)

r += 1

// ── VOLUME ──

vol_pct_d = volume_sma > 0 ? volume / volume_sma * 100 : 100

vol_bg = volume_spike ? #00C853 : volume_floor_ok ? #78909C : #FF1744

table.cell(db, 0, r, "Volume", text_color=#B0BEC5, bgcolor=bg_r, text_size=sz, text_halign=text.align_left)

table.cell(db, 1, r, str.tostring(vol_pct_d, "#") + "% avg" + (volume_spike ? " SPIKE" : volume_floor_ok ? "" : " LOW"), text_color=color.white, bgcolor=vol_bg, text_size=sz, text_halign=text.align_right)

r += 1

// ── REGIME ──

reg_bg = regime_state==1 ? #00C853 : regime_state==2 ? #FF9800 : regime_state==3 ? #42A5F5 : #78909C

table.cell(db, 0, r, "Regime", text_color=#B0BEC5, bgcolor=bg_r, text_size=sz, text_halign=text.align_left)

table.cell(db, 1, r, regime_label + " SL:" + str.tostring(regime_sl,"#.1") + " TP:" + str.tostring(regime_tp,"#.1"), text_color=color.white, bgcolor=reg_bg, text_size=sz, text_halign=text.align_right)

r += 1

if dash_style == "Full"

// ── NW RIBBON ──

nw_text = nw_relaxed_bull ? "BULL " + str.tostring(nw_ordered_bull) + "/7" : nw_relaxed_bear ? "BEAR " + str.tostring(nw_ordered_bear) + "/7" : "FLAT"

nw_bg = nw_relaxed_bull ? #00C853 : nw_relaxed_bear ? #FF1744 : #546E7A

table.cell(db, 0, r, "NW Ribbon", text_color=#B0BEC5, bgcolor=bg_r, text_size=sz, text_halign=text.align_left)

table.cell(db, 1, r, nw_text, text_color=color.white, bgcolor=nw_bg, text_size=sz, text_halign=text.align_right)

r += 1

// ── ORDER FLOW ──

of_text = of_bullish ? "BUY FLOW" : of_bearish ? "SELL FLOW" : close > vwap ? "> VWAP" : "< VWAP"

of_bg = of_bullish ? #00C853 : of_bearish ? #FF1744 : close > vwap ? color.new(#00C853, 40) : color.new(#FF1744, 40)

table.cell(db, 0, r, "Order Flow", text_color=#B0BEC5, bgcolor=bg_r, text_size=sz, text_halign=text.align_left)

table.cell(db, 1, r, of_text, text_color=color.white, bgcolor=of_bg, text_size=sz, text_halign=text.align_right)

r += 1

// ── SMC ──

smc_text = smc_bullish ? "BULL" : smc_bearish ? "BEAR" : "WAIT"

smc_bg = smc_bullish ? #00C853 : smc_bearish ? #FF1744 : #546E7A

table.cell(db, 0, r, "Smart Money", text_color=#B0BEC5, bgcolor=bg_r, text_size=sz, text_halign=text.align_left)

table.cell(db, 1, r, smc_text + (bullish_bos ? " BOS+" : bearish_bos ? " BOS-" : ""), text_color=color.white, bgcolor=smc_bg, text_size=sz, text_halign=text.align_right)

r += 1

// ── VIX MOMENTUM ──

vm_bg = vix_rising ? #FF1744 : vix_falling ? #00C853 : #546E7A

table.cell(db, 0, r, "VIX ROC", text_color=#B0BEC5, bgcolor=bg_r, text_size=sz, text_halign=text.align_left)

table.cell(db, 1, r, vix_momentum + " " + str.tostring(vix_roc_val, "#.1") + "%", text_color=color.white, bgcolor=vm_bg, text_size=sz, text_halign=text.align_right)

r += 1

// ── VIX SIZE MULT ──

vs_bg = vix_size_mult >= 1.1 ? #00C853 : vix_size_mult <= 0.7 ? #FF1744 : #546E7A

table.cell(db, 0, r, "VIX Size", text_color=#B0BEC5, bgcolor=bg_r, text_size=sz, text_halign=text.align_left)

table.cell(db, 1, r, str.tostring(vix_size_mult, "#.2") + "x", text_color=color.white, bgcolor=vs_bg, text_size=sz, text_halign=text.align_right)

r += 1

// ── DC WIDTH ──

dcw_bg = dc_squeeze ? #FF9800 : #546E7A

table.cell(db, 0, r, "DC Width", text_color=#B0BEC5, bgcolor=bg_r, text_size=sz, text_halign=text.align_left)

table.cell(db, 1, r, str.tostring(dc_width_pct, "#.2") + "%" + (dc_squeeze ? " SQUEEZE" : dc_expanding ? " EXPANDING" : ""), text_color=color.white, bgcolor=dcw_bg, text_size=sz, text_halign=text.align_right)

r += 1

// ── GUARD ──

table.cell(db, 0, r, "Guard", text_color=#B0BEC5, bgcolor=bg_r, text_size=sz, text_halign=text.align_left)

table.cell(db, 1, r, guard_active ? "PAUSED" : "OK L:" + str.tostring(consec_losses) + " DD:" + str.tostring(dd_pct,"#.1") + "%", text_color=color.white, bgcolor=guard_active ? #FF1744 : #00C853, text_size=sz, text_halign=text.align_right)

r += 1

// ── STATS ──

wr = total_trades > 0 ? float(wins) / float(total_trades) * 100 : 0

table.cell(db, 0, r, "Stats", text_color=#B0BEC5, bgcolor=bg_r, text_size=sz, text_halign=text.align_left)

table.cell(db, 1, r, str.tostring(total_trades) + " trades WR:" + str.tostring(wr, "#.0") + "%", text_color=color.white, bgcolor=wr >= 55 ? #00C853 : wr >= 45 ? #FF9800 : #FF1744, text_size=sz, text_halign=text.align_right)