Market Mastery Blueprint Strategy

ลิงก์ TradingView

คำอธิบาย

The Market Mastery Blueprint Strategy is a trend-following and mean-reversion hybrid built on the 3-part framework of State, Position, and Event.

STATE

The strategy classifies market conditions using the percentage spread between the 20MA and 200MA:

- Narrow State: MAs are close together (spread <= 0.5%) — signals compression and potential breakout.

- Wide State: MAs are far apart (spread >= 1.0%) — signals extended trend and potential reversal.

POSITION

Two high-probability trade zones are defined:

- Position 1 (Gold Mine): Price is within 1 ATR of the 200MA — a high-value pullback zone for long entries.

- Position 3 (Pluto Land): Price is extended above both MAs with both gaps (price to 20MA and 20MA to 200MA) exceeding 1.5 ATR — a high-risk overextension zone used for short entries.

EVENT

Two candlestick signals confirm trade entries:

- Elephant Bar (Long): A strong bullish candle whose body is at least 1.5x the 20-bar average body size, confirming institutional buying in Position 1.

- Topping Tail (Short): A candle where the upper wick makes up 60% or more of the total range, confirming rejection in Position 3.

RISK MANAGEMENT

- Dynamic position sizing: risk is calculated as a fixed percentage of equity divided by the stop distance.

- 3R profit target: take profit is set at 3x the initial risk.

- Hard stop: long stop = low of signal bar, short stop = high of signal bar.

IDEAL USE CASE

Best used on SPY or SPX on the 2-minute to daily timeframe. Signals can be used to time entries for options spreads (call spreads, put spreads, bear call spreads) with 0-2 DTE and defined max risk of $300 per trade.

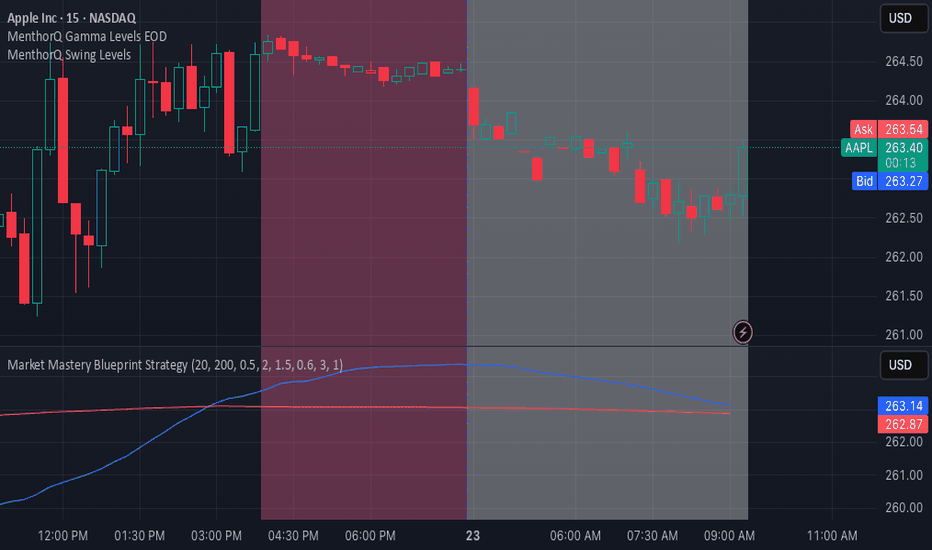

รูป Preview

Pine Script Source

//@version=5

strategy("Market Mastery Blueprint Strategy",

overlay=true,

margin_long=100,

margin_short=100,

initial_capital=10000,

pyramiding=0,

commission_type=strategy.commission.percent,

commission_value=0.01)

// ── Inputs ──

maLenFast = input.int(20, "Fast MA Length")

maLenSlow = input.int(200, "Slow MA Length")

maSpreadThr = input.float(0.5, "Narrow State MA Spread (%)", step=0.1)

wideFactor = input.float(2.0, "Wide State Spread Multiplier", step=0.1)

eleFactor = input.float(1.5, "Elephant Body vs Avg Body", step=0.1)

tailFactor = input.float(0.6, "Tail Wick % of Range", step=0.05)

riskR = input.float(3.0, "R Multiple Target", step=0.5)

riskPct = input.float(1.0, "Risk % of Equity per Trade", step=0.25)

// ── MAs & ATR ──

maFast = ta.sma(close, maLenFast)

maSlow = ta.sma(close, maLenSlow)

atr = ta.atr(14)

plot(maFast, color=color.blue, title="20MA")

plot(maSlow, color=color.red, title="200MA")

// ── State detection ──

spreadPct = math.abs(maFast - maSlow) / maSlow * 100

narrowState = spreadPct <= maSpreadThr

wideState = spreadPct >= maSpreadThr * wideFactor

// ── Position zones ──

pos1 = math.abs(close - maSlow) <= 1.0 * atr

aboveBoth = close > maFast and close > maSlow

threeFinger = (close - maFast) > 1.5 * atr and (maFast - maSlow) > 1.5 * atr

pos3 = aboveBoth and threeFinger

// ── Events ──

bodySize = math.abs(close - open)

avgBody = ta.sma(bodySize, 20)

elephant = close > open and bodySize >= eleFactor * avgBody

longSignal = narrowState and pos1 and elephant

candleRange = high - low

upperWick = high - math.max(open, close)

toppingTail = upperWick >= tailFactor * candleRange

shortSignal = wideState and pos3 and toppingTail

// ── Position sizing ──

var float entryPrice = na

var float stopPrice = na

var float tpPrice = na

// Long setup

if longSignal and strategy.position_size <= 0

entryPrice := close

stopPrice := low

float riskPerShare = entryPrice - stopPrice

if riskPerShare > 0

float capitalRisk = strategy.equity * (riskPct / 100.0)

float qty = capitalRisk / riskPerShare

tpPrice := entryPrice + riskR * riskPerShare

strategy.entry("Long", strategy.long, qty=qty)

strategy.exit("Long TP/SL", "Long", stop=stopPrice, limit=tpPrice)

// Short setup

if shortSignal and strategy.position_size >= 0

entryPrice := close

stopPrice := high

float riskPerShare = stopPrice - entryPrice

if riskPerShare > 0

float capitalRisk = strategy.equity * (riskPct / 100.0)

float qty = capitalRisk / riskPerShare

tpPrice := entryPrice - riskR * riskPerShare

strategy.entry("Short", strategy.short, qty=qty)

strategy.exit("Short TP/SL", "Short", stop=stopPrice, limit=tpPrice)