Mean Reversion V-F V.1

ลิงก์ TradingView

คำอธิบาย

I received lot of request to publish better version of Mean Reversion V-F so here you go

In V.1 WE going in Long trade after MA falling # of bars

The # of bars can be adjust from the settings

New calculation for deviations - after the first trade calculation start from close of the bar and so on

The first trade is market trade the rest are limit trades so can get to it in any time if the price

drop to that deviations level

Can be use for crypto and stocks

For stocks just enable Use for Stocks and input # of stocks

The strategy gave my lot better results and less drown down

If any question let my know

Happy trading

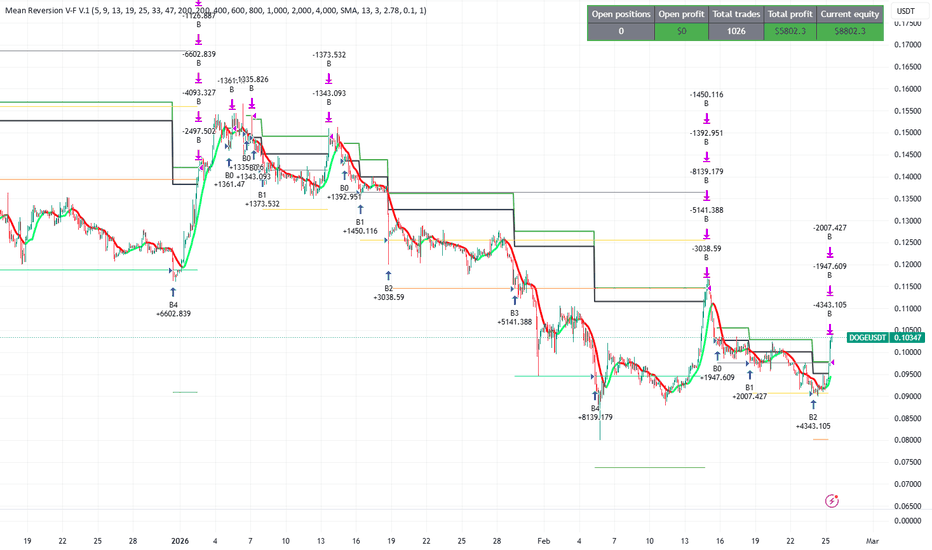

รูป Preview

Pine Script Source

// This Pine Script® code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fullmax

//@version=6

strategy('Mean Reversion V-F V.1', overlay = true)

//input variables

STK = input.bool(defval = false, title = 'Use for Stocks- how many Stocks in units level')

//// settings

deviation = input.float(title = 'Deviation Increment (%)', defval = 3, minval = 0.01, maxval = 100,step=0.1) / 100

deviation1 = input.float(title = 'Deviation Increment1 (%)', defval = 5, minval = 0.01, maxval = 100,step = 0.1) / 100

deviation2 = input.float(title = 'Deviation Increment2 (%)', defval = 7, minval = 0.01, maxval = 100,step = 0.1) / 100

deviation3 = input.float(title = 'Deviation Increment3 (%)', defval = 9, minval = 0.01, maxval = 100,step = 0.1) / 100

deviation4 = input.float(title = 'Deviation Increment4 (%)', defval = 13, minval = 0.01, maxval = 100,step=0.1) / 100

deviation5 = input.float(title = 'Deviation Increment5 (%)', defval = 17, minval = 0.01, maxval = 100,step=0.1) / 100

deviation6 = input.float(title = 'Deviation Increment6 (%)', defval = 25, minval = 0.01, maxval = 100,step=0.1) / 100

deviation7 = input.float(title = 'Deviation Increment7 (%)', defval = 31, minval = 0.01, maxval = 100,step=0.1) / 100

unitsLevel = input.float(title = 'First trade (units in cash)', defval = 50, maxval = 10000)

unitsLevel1 = input.float(title = 'Level 1 (units in cash)', defval = 100, maxval = 10000)

unitsLevel2 = input.float(title = 'Level 2 (units in cash)', defval = 200, maxval = 10000)

unitsLevel3 = input.float(title = 'Level 3 (units in cash)', defval = 400, maxval = 10000)

unitsLevel4 = input.float(title = 'Level 4 (units in cash)', defval = 600, maxval = 10000)

unitsLevel5 = input.float(title = 'Level 5 (units in cash)', defval = 800, maxval = 10000)

unitsLevel6 = input.float(title = 'Level 6 (units in cash)', defval = 1000, maxval = 10000)

unitsLevel7 = input.float(title = 'Level 7 (units in cash)', defval = 1000, maxval = 10000)

//moving average

string maType = input.string("WMA", "MA type", options = ["WMA", "SMA", "RMA", "EMA" , "HMA"])

int maLength = input.int(20, "MA length", minval = 2)

float ma = switch maType

"EMA" => ta.ema(close, maLength)

"SMA" => ta.sma(close, maLength)

"RMA" => ta.rma(close, maLength)

"WMA" => ta.wma(close, maLength)

"HMA" => ta.hma(close, maLength)

=>

runtime.error("No matching MA type found.")

float(na)

//falling ma for the first trade

fm= input(5,"# of bars MA to fall to fet in the first trade")

/// buy signal

rdma = ta.falling(ma,fm)

/////////// set static levels

float s1 = 0.00

s1 := na(s1[1]) ? na : s1[1]

s2 = 0.00

s2 := na(s2[1]) ? na : s2[1]

s3 = 0.00

s3 := na(s3[1]) ? na : s3[1]

s4 = 0.00

s4 := na(s4[1]) ? na : s4[1]

s5 = 0.00

s5 := na(s5[1]) ? na : s5[1]

s6 = 0.00

s6 := na(s6[1]) ? na : s6[1]

s7 = 0.00

s7 := na(s6[1]) ? na : s7[1]

////

//// take Profit

take_profit1 = input.float(1.67, title = 'Target Take Profit (%)', step = 0.01, minval = 0.0) / 100

take_profit_level1 = strategy.position_avg_price * (1 + take_profit1)

plot(take_profit_level1, style = plot.style_linebr, linewidth = 2, color = color.green)

plot(strategy.position_avg_price, style = plot.style_linebr, linewidth = 2, color = color.black)

/////brake even plot

fee = input.float(0.1,step= 0.1,title = 'exchange fee')/100

long_order_fee = strategy.position_avg_price * (1 + fee)

plot(long_order_fee, style = plot.style_linebr, linewidth = 2, color = strategy.position_size > 0 ? color.rgb(63, 69, 54, 84) : na)

/// trailing take profit % or hull

takeProfitTrailingEnabled = input.bool(defval = false, title = 'Enable Trailing', tooltip = 'Enable or disable the trailing for take profit. WARNING! This feature will repaint. Make sure you use it with "Bar Magnifier" and "Deep Backtesting" for realistic backtest results')

trailingTakeProfitDistancePerc = input.float(defval = 1.0, title = ' Trailing Distance %', minval = 0.01, maxval = 100, step = 0.01, tooltip = 'The distance as a percentage of the take profit price to keep from the high price after the target is reached when trailing.') / 100

// LOGIC

longTrailingTakeProfitStepTicks = take_profit_level1 * trailingTakeProfitDistancePerc / syminfo.mintick

////// # of trades and take profit

nt = str.tostring(strategy.opentrades)

if strategy.position_size > 0

strategy.exit('B', limit = takeProfitTrailingEnabled ? na : take_profit_level1, trail_price = takeProfitTrailingEnabled ? take_profit_level1 : na, trail_offset = takeProfitTrailingEnabled ? longTrailingTakeProfitStepTicks : na)

//mode

if rdma and strategy.opentrades == 0

strategy.entry('B' + nt, strategy.long, STK ? unitsLevel : unitsLevel/close)

s1 := close*(1 - deviation1)

if strategy.opentrades == 1

strategy.entry('B'+ nt, strategy.long, STK ? unitsLevel1 : unitsLevel1/close,limit = s1)

s2 := close*(1 - deviation2)

if strategy.opentrades == 2 and strategy.opentrades > 1

strategy.entry('B'+ nt, strategy.long, STK ? unitsLevel2 : unitsLevel2/close,limit = s2)

s3 := close*(1 - deviation3)

if strategy.opentrades == 3 and strategy.opentrades > 2

strategy.entry('B'+ nt, strategy.long, STK ? unitsLevel3 : unitsLevel3/close,limit = s3 )

s4 := close*(1 - deviation4)

if strategy.opentrades == 4 and strategy.opentrades > 3

strategy.entry('B'+ nt, strategy.long, STK ? unitsLevel4 : unitsLevel4/close,limit = s4)

s5 := close*(1 - deviation5)

if strategy.opentrades == 5 and strategy.opentrades > 4

strategy.entry('B'+ nt, strategy.long, STK ? unitsLevel5 : unitsLevel5/close,limit = s5)

s6 :=close*(1 - deviation6)

if strategy.opentrades == 6 and strategy.opentrades > 5

strategy.entry('B'+ nt, strategy.long, STK ? unitsLevel6 : unitsLevel6/close,limit = s6)

s7 := close*(1 - deviation7)

if strategy.opentrades == 7 and strategy.opentrades > 6

strategy.entry('B'+ nt, strategy.long, STK ? unitsLevel7 : unitsLevel7/close,limit = s7)

//plot

maupdn = ma > ma[1] ? #0aff68 : ma < ma[1] ? #ff0a0a : na

plot(ma, color = maupdn, linewidth = 3)

// plot statics level's

st1 = plot(strategy.opentrades > 0 ? s1 : na, title = 'Long 2 SLayer', style = plot.style_linebr,color = color.gray)

st2 = plot(strategy.opentrades > 1 ? s2 : na, title = 'Long 3 SLayer', style = plot.style_linebr, color = color.yellow)

st3 = plot(strategy.opentrades > 2 ? s3 : na, title = 'Long 4 SLayer', style = plot.style_linebr,color = color.orange)

st4 = plot(strategy.opentrades > 3 ? s4 : na, title = 'Long 5 SLayer', style = plot.style_linebr, color = color.lime)

st5 = plot(strategy.opentrades > 4 ? s5 : na, title = 'Long 6 SLayer', style = plot.style_linebr, color = color.green)

st6 = plot(strategy.opentrades > 5 ? s6 : na, title = 'Long 7 SLayer', style = plot.style_linebr, color = color.blue)

st7 = plot(strategy.opentrades > 6 ? s7 : na, title = 'Long 7 SLayer', style = plot.style_linebr, color = color.red)

//////////